The following is part of Pivotal Events that was published for our subscribers May 1, 2008.

SIGNS OF THE TIMES:

Last Year:

"Investors Rein In Market That Funds Leveraged Buyouts"

"Up until April, the market for risky loans was so lenient borrowers could cut their interest rates simply by asking - rather than providing anything to - investors."

- Wall Street Journal, April 27, 2007

* * * * *

This Year:

"Prices are soaring [food] and stand every chance of staying high because this crisis is different." [emphasis added]

- Globe and Mail, April 12, 2008

"It's a panic [on rice]. My customers are demanding double their usual volume."

"In an effort to maintain social peace through low local prices, governments have stepped up their purchases."

- Financial Times, April 17, 2008

"Weakness in the dollar has not been exhausted."

- Letter-writer Jim Willie, April 24, 2008

It is worth adding that Ross Clark's impartial model in the April 2, 2008 ChartWorks registered a "Downside Capitulation" on the Dollar Index and an "Upside Exhaustion" on the Euro.

Needless to say, but the DX, which had established the "Sequential Buy" pattern as well, has established an uptrend.

* * * * *

Stock Markets: Last week we reviewed the dominant pattern in the stock market which was set by the plunge into the January low, from which a rebound out to March-April would be likely. The Bear Stearns panic was news related, and should not be considered as the worst event. Going along with this, one should not conclude that the heroic efforts of policymakers have got the markets back on the road to prosperity. The consensus opinion, which did not anticipate the severity of the contraction, should not be relied upon for advice in a financial storm. Using history as a guide, this credit contraction has much further to go.

However, the relief likely to come into the markets and run into around now is being fully expressed - perhaps culminating with the "genius" behind yesterday's Fed cut and wise comment. We expected that the recovery would be sufficient to make policymakers look good again. The way we look at it is that throughout market history, short-dated market rates of interest increase during a bull market and then decline virtually until the subsequent bear market is over.

Typically, administered rates at the senior central bank follow market rates, so yesterday's main event is of little consequence.

The key question now - Is the market up when it should be? - Yes.

Is it showing signs of excess? - The S&P and Naz are getting close to our target of a 50% retracement, and the Dow has made it. This is good, but it has been achieved with weak technicals - such as shown in the attached chart on divergences. This is not-so-good.

How valid is the confidence that boom-prosperity has been restored? As stated above, the consensus has done little original research into great credit expansions and consequent contractions.

Another consideration is the action that was likely to run with the stock market, which has been the commodity rally. Now that rice has followed the earlier huge blowout and collapse in wheat it is reasonable to conclude that the cyclical bull market in grains is over.

More discussion on commodities can be read below. But the point is that the best possible on reflating asset prices has been accomplished and all sectors are vulnerable to seasonal decline as well as to the news of financial disaster already accomplished as well as to those yet to be discovered.

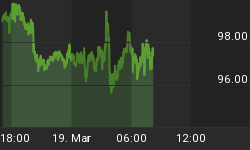

Sector Comment: At the low for banks in January we were looking for a 50% retracement rally out to March-April. Instead, there was an instantaneous rebound to 96 (98 was the target), which we noted at the time. Since the end of January the action has been choppy with two lows testing the January washout.

The BKX could get a little higher, which would get the weekly RSI up to the level that ends bear market rallies.

A week ago Wednesday, the ChartWorks noted the "Upside Exhaustion" readings on some of the hot energy stocks, as well as on Potash as representing the Ag sector. The swoon since is becoming impressive.

INTEREST RATES

The Long Bond found stability at 115.25 and it looks like it will have to do some work at this level. Momentum is not yet low enough to end the decline, and breaking below 115 would be poor chart action that would likely indicate that liquidity concerns are working their inevitable way towards long-dated treasuries.

Credit Spreads were also likely to be benign to favourable through the rebound until around now. As yesterday's WSJ reported "The junk-bond market is closing out its best month in years." This was referring to traditional corporates and the price rally also showed up in the higher-ranked sub-prime bonds.

However, as we have been noting the spread market can have a seasonal reversal in May. One of the things that helps is to have some good action going into May - and this we have.

But, over in sub-prime land, the BBB and BBB-minus have already declined to new lows and the only somewhat better stuff will soon follow. The BBB, which traded at 100 in August, 2006 is now quoted at 8.05 (no typo).

The way that this is likely to work out is that the slide in commodities will be associated, as usual, with declining earnings. This will diminish the ability to service debt, etcetera. Declining tax revenues will do the same for many sovereign issues.