The Faces of Dissipating Appetite

The 4 charts below display the emerging challenges for risk overall risk appetite as manifested through EURUSD, GBPUSD, S&P500 and US crude oil. The latter is increasingly considered as the lifeblood of overall risk appetite, showing recurring failure to break above the $73 level and the negative momentum divergence, as seen by falling stochastics and a flattening price. A similar negative divergence is seen in the S&P500 (as is the case in most equity indices), facing key resistance at 1,015-- the 38% retracement of the decline from all time high of October 2007 to the low of March 2009.

And as appetite diminishes, currencies such as EUR and GBP tend to lose ground vs. USD and JPY. The 2 top charts (EURUSD and GBPUSD) show increasing difficulty in regaining recent upside and are gradually vulnerable to prolonged losses. Despite regaining $1.43, EURUSD is unlikely to hold above this figure in light of the unsustainable risk picture. $1.4090 remains a near-term target, before a retest of $1.3750 emerges.

We've shown last week how struggling oil prices, a bottoming VIX index and a protracted sell-off in the Shanghai Composite illustrated nascent signs of a turnaround in the appetite for risk. The VIX remains well above its 50-week average and multi-month trend line support of 21 while the Shanghai Composite has lost 10% in less than 2 weeks.

Sterling Nears Key Juncture

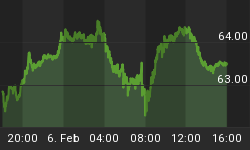

We reiterate our bearishness against GBP (from last week's missive) as the Fed appears less generous in its quantitative easing plans relative to the Bank of England after saying it will slow the pace of purchasing the remaining $50 billion in US Treasuries. Although GBPUSD held up above the key technical level of $1.64 (50-day moving average), the chart shows the pair at risk of falling below the 50-day MA, a medium term trend line which effectively denoted the breakdown point between rising and falling trend.

Note how GBPUSD first fell below its 50-day MA in Q3 2009 at the height of the BoE's 180-degree turn in monetary policy in autumn 2008 and remained below the average ever since UNTIL March 2009 when the FOMC announced treasury purchases.

And with the Fed hinting it will slow the pace of Treasury purchases (good for USD) at same time as BoE to raise its guilt purchases (bad for GBP), the net effect leaves GBP exposed to potentially deeper losses as the BoE remains the more generous provider of QE.

Wake-up Call to FIFO Believers The unexpected 0.3% q/q increase in Germany's Q2 GDP comprises a technical end to the recession and a wake-up call to the widely misguided forecasts suggesting the US recovery would precede that of Europe. Those FIFO claims (First-in-First-out) stating the US would be first to exit recession simply because it was first to fall into one where largely based on the magnitude of the fiscal and monetary policy stimulus by the US authorities. But one-time quarterly rebounds in the aftermath of 2-3 consecutive quarterly contractions are not unusual. Government stimuli, auto incentive schemes and inventory restocking remain no substitutes to a secular rebound in consumer power, especially when unemployment rates have yet to stabilize.

In the case of the US, despite the positive growth impact from lower trade gap and inventory restocking, the severity of the US housing downturn and the persistent (not yet stabilized) corrosive impact on US consumers (from escalating foreclosures and rising unemployment) will keep growth in contraction territory until Q4.