Gold lost more than $50 an ounce this month, in large part due to worries that China will cool off its current torrid pace. Investors are concerned that the People's Republic of China's seemingly out of control growth will slowdown, raising fears of a hard landing reminiscent of the early nineties. Having visited China twice in the last six months and as recently as three weeks ago, such meltdown fears are overblown. Ten years ago much of China's east coast was still a backwater. However since 1976, China's real GDP growth has averaged 9 percent per year, or three times the average of major industrialized countries. So far this year, China's booming GDP grew by 9.7 percent in the first quarter, acting as a powerful stimulus to the world as both producer and consumer.

China's astonishing economic growth in the past has provoked dire warnings of the unsustainability of its economic boom. Yet year after year, the Middle Kingdom has disproved these naysayers.

China's booming economy is heavily dependant on natural resources

China is now the number one consumer in the world of copper, platinum, steel, zinc and iron. They produce more steel than the United States and Japan combined. And there are more cell phone users and beer drinkers than in the United States. The Ministry of Commerce reported that China's foreign trade this year will top $1 trillion this year, up 17 percent. While exports will be up 15 percent to $505 billion, imports will grow even faster to $495 billion, up 20 percent. In the fourth quarter of last year, China's imports reached $124.1 billion, up 42.3 percent. China is the fastest growing economy the world, and its voracious demand for everything from oil to copper is causing a spike in prices.

In 1997, Beijing's attempt to engineer a gradual slowdown caused a hard landing. Unlike then, the boom today is much more broadly based, particularly with a newly created middle-class exceeding that of the American population. The Chinese for example have introduced two "Golden Week" holidays a year, where the nation literally shuts down, allowing throngs of people to travel and spend. Beijing alone received 3.6 million tourists during the seven-day holiday. Chinese consumer demand, which is currently among the lowest in the Far East, is expected to grow significantly.

In 1997, Beijing's attempt to engineer a gradual slowdown caused a hard landing. Unlike then, the boom today is much more broadly based, particularly with a newly created middle-class exceeding that of the American population. The Chinese for example have introduced two "Golden Week" holidays a year, where the nation literally shuts down, allowing throngs of people to travel and spend. Beijing alone received 3.6 million tourists during the seven-day holiday. Chinese consumer demand, which is currently among the lowest in the Far East, is expected to grow significantly.

Indeed, it is China's push to boost its infrastructure, which is fueling a large part of its growth. Moreover the needed "slower" growth still means powerful economic growth (by western standards) and a continuation of the Chinese economy's insatiable demand for resources. China has boosted spending for steel, cement, roads and power facilities. To rein in this growth, capital requirements for new steel projects were raised to 45 percent from 25 percent and real estate projects were raised to 35 percent. The People's Bank of China raised its reserve ratio to 7.5 percent from 7.0 percent. These tightening measures are more of a signal than actual depressants to growth. Beijing has a major pipeline of investment and the Olympics are an excuse for this infrastructure spending. China's real problem is allocating its resources to where it needs it the most.

Over-investment in infrastructure

China is also in the midst of a massive investment spending cycle. The last bubble was in 1993-94, when year-to-year growth in fixed investment hit 60 percent. The fixed investment share of GDP was 43 percent in 2003. While fixed investment is growing due to infrastructure spending as a proportion of GDP, it was much higher in the past. Unlike the United States, which went through an over-investment boom in technology, China's overinvestment in infrastructure is to accommodate the demands of a growing population. The situation is different from that of the early 1990s with free market reforms the key driver in the Chinese economy.

Demographics: Key Driver

Demographics are a big factor when talking about the China syndrome. China has the largest population in the world, with 1.3 billion people representing 25% of the world's population. China has over 30 cities with populations over 5 million, with Shanghai topping 20 million people, and Beijing with 15 million people. In its zeal for restraining its population growth, Beijing introduced a "one child" policy. There appears to be a skewing towards more boys and thus China's sex ratios are out of whack. This policy is apparently ending and there is believed to about 300 million non-reported children that may be added to the rosters. China has a young population and the addition of 300 million more, mostly girls, would correct an already skewed gender imbalance.

Demographics are a big factor when talking about the China syndrome. China has the largest population in the world, with 1.3 billion people representing 25% of the world's population. China has over 30 cities with populations over 5 million, with Shanghai topping 20 million people, and Beijing with 15 million people. In its zeal for restraining its population growth, Beijing introduced a "one child" policy. There appears to be a skewing towards more boys and thus China's sex ratios are out of whack. This policy is apparently ending and there is believed to about 300 million non-reported children that may be added to the rosters. China has a young population and the addition of 300 million more, mostly girls, would correct an already skewed gender imbalance.

Simply, while China has grown over the past decade, there is room for more growth. Sure there will be short-term shortages but everywhere we went there was the recognition for more growth. This growth is needed to provide the millions of jobs that are required. Over 60 percent of China's labour force remains in the countryside but there is a steady migration with some 30 percent of the population now living in the cities. China must accommodate this growth with respect to housing, jobs, etc.

When they build, they do come

China's policymakers have embarked on meaningful economic reforms and in this case when they build, people do come. For example, in 1989, the total number of expressways (the size of the 401) in China was only 271 kilometers. Ten years later, China had over 1,000 kilometers of expressways and at yearend there was 30,000 kilometers of expressways. On this recent trip to China's coast, everywhere expressways were being built to link up the major cities. Beijing needs these highways since all were choked with speeding trucks and kamikazi drivers who do not respect lanes or other drivers. China hopes to have 82,000 kilometers of expressways, which will link most of its major centers. The problem however is once arriving in these cities, there still exists no easy way to move through the cities. Congestion is a problem, day and night.

The Power Crisis

China is also suffering a chronic shortage of electricity and plans to install 42 gigawatts of generating plant capacity this year alone, equivalent to the UK's entire installed capacity. Having flown, traveled by rail and car, we noted the need for more rail capacity since China's roads are already choked with trucks. The list goes on, including the need for additional port and shipping facilities, water treatments facilities and environmental infrastructure requirements.

Americans forewarned

Of more concern, as goes the Chinese economy, so goes America's financial markets. By becoming the world's largest debtor nation, America has unknowingly allowed itself to be governed by the newest superpower, China. China has immense reserves now, second only to Japan. With $400 billion of foreign exchange reserves invested largely in United States Treasuries, the Chinese have financed a large part of the American deficits. Should China slowdown or alternatively decide to dump its bonds in favour of gold or euros, it would throw American financial markets into a tailspin, causing US interest rates to skyrocket - and that is the Achilles' heel of the American dream.

Of more concern, as goes the Chinese economy, so goes America's financial markets. By becoming the world's largest debtor nation, America has unknowingly allowed itself to be governed by the newest superpower, China. China has immense reserves now, second only to Japan. With $400 billion of foreign exchange reserves invested largely in United States Treasuries, the Chinese have financed a large part of the American deficits. Should China slowdown or alternatively decide to dump its bonds in favour of gold or euros, it would throw American financial markets into a tailspin, causing US interest rates to skyrocket - and that is the Achilles' heel of the American dream.

America's budget deficit has been piling up, in part due to the war in Iraq. The war is harming the US economy, costing to date $200 billion and now Bush is seeking another $25 billion. Notwithstanding a stronger economy, the United State's current account deficit will exceed a record $500 billion this year. This means that every single day, the US must borrow around $1.5 billion from abroad to finance the huge gap between its imports and exports.

Be careful what you wish for

To date foreign investors, in particular the Chinese and Japanese, have financed America's twin deficits. However, having spent $137 billion on intervention this year, the Japanese did not acquire any US dollars in April for the first time in seven years, reflecting in part their own strengthening economy and stabilized currency. Moreover, the collapse in the bond markets prompted foreign investors to curtail their purchases of US debt with the realization that the Americans are pursuing a policy of currency debasement to pay off their debts.

Yet this oversupply of US dollars is seeding a huge monetary expansion in China with the Chinese surplus piling up at more than a $100 billion a year as the dollar gets weaker, the Chinese economy gets stronger. Of concern is that by pressuring the Chinese for everything from the "peg" to trade irritants, the Americans risk the Chinese might follow the Japanese and other investors and begin to dump their dollars in favour of other instruments such as euros and gold - and that is the last thing that Bush needs now.

But all are not dependent on the largesse of banks. In Beijing, I met a number of dot com entrepreneurs, with one having recently completed a Nasdaq IPO. Indeed, there is a great desire for companies to tap the international markets for funding with more than 1,000 companies queuing to list on the Hong Kong Stock Exchange. Be ready for an invasion of Chinese companies, many of them with excellent prospects and surprisingly good balance sheets. Price-Waterhouse Coopers estimates that Chinese IPOs could raise $20 billion surpassing the US market this year.

China's golden opportunity

China is vast, not only in size and population, but also in mineral wealth. Mining has an incredible long history in China. Shandong province and Hebei province have been mining for thousands of years. By North American standards China's mines are small. Under the "Mineral Resources Law", all mineral resources of the People's Republic of China are owned by the State. Mining rights are allowed in a specific area for a specific time period and subject to the Ministry of Land and Natural Resources. China has about 1,000 gold mining operations, many of them owned by State agencies or geological groups.

China has become the world's fourth largest gold producer in the world. Shandong province is a major gold province that produced almost 250,000 ounces of gold last year. The largest mine recently went public on the Hong Kong Stock Exchange. Over the past few years the Chinese have deregulated gold exploration and mining activities. A "White Paper" was recently completed although that is not expected to become law until later this decade.

We recently visited a number of these gold mines in Shandong. Of interest is that China would benefit from Western technology and equipment since there has been little drilling. While there is evidence of much gold, little is known of the depth potential. Mechanized mining is unknown here. We believe that China will adopt further changes in order to develop its domestic gold mining industry.

China currently produces about 200 tonnes which matches its current consumption. Albert Cheng of the World Gold Council noted that the Chinese have about $1.2 trillion in savings but the country has one of the lowest gram per capita at 0.16 grams per capita in contrast to 0.73 in India and 1.41 in the United States. In the last couple of years, China has allowed its people to own gold and the Shanghai Gold Exchange is an avenue for its producers to sell production. Shanghai plans to offer gold futures to further stimulate trading. With a deregulated market and improving incomes, Cheng expects this level to rise significantly.

With China becoming such a big factor on a global scale, attention is being paid to its huge foreign exchange position. So far the Chinese have accumulated about 600 tonnes of gold or less then 2% of its foreign exchange reserves in gold. Given the development of China's national economy, we believe that China will moderately increase their gold reserves to 4-5% of reserves. Just to get to that level would require China to accumulate all the gold production for the next two years. In time, China would like to have reserves in line with their European counterparts, who hold 13% of their reserves backed by gold.

Recommendations

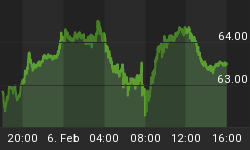

Gold reached a 15-year peak in the last quarter, retesting the early high this year before retreating to a six month low. The collapse has been so severe that many gold stocks broke their 200-day moving averages prompting technicians and pundits to declare gold's bull market over. Wrong.

Not only, has America's debt load crushed the US economy, but the attendant stimulus is finally showing up in higher rates of inflation. The pick up in inflation has been based on too little supply and too much demand exacerbated by geopolitical events. And China's need to build infrastructure has required much more natural resources.

Against this background, gold will rebound underpinned by dehedging, growing concern that inflation will accelerate, higher oil prices and yes, a lower US dollar. The US dollar has enjoyed a "dead cat" bounce within a clearly defined downtrend. Chronic American twin deficits will keep the dollar relatively weak against other currencies (and gold) while fundamentals such as dehedging, investor demand and $40 a barrel oil prices will underpin gold prices. The ramifications of a China-centric world together with the seachange in the low interest landscape will further underpin gold prices.

Gold is an effective hedge and investors would be wise to rebuild positions before the next gold rush to $510 an ounce.

China's reluctance to provide access

If China is to encourage the development of gold mining, what about some of the Canadian mines that are already in China? Unfortunately there have been few successes in China. Title we believe will a problem for many. Other than in three provinces, China has also been reluctant to provide access to its producers. As such, foreign companies were left with "crumbs" like refractory deposits or had to look for gold in the frontier areas. Moreover, from a geological point of view, much has been made of the similarity with Carlin-type gold deposits, which is misleading since Carlin we believe is unique only to Nevada. We have yet to see a Carlin-type deposit in China. There is no question that China holds exciting mineralogical potential borne out by the copious amount of geological and geo-chem surveys conducted by the various provinces. We believe that China will receive increased investor attention particularly as it allows access to the producers rather than just exploration "moose pasture" and only then will those elusive multimillion-ounce deposits be found.

Southwestern Resources Corp. has been a huge success on hopes that the Boka gold project in beautiful Yunnan province would develop into a big gold mine. Although we do not question the existence of gold, we do not subscribe to the view that this is a viable multimillion-ounce bulk deposit. Not only has Southwestern not established any proven reserves but there has been a lack of sufficient drilling information to support the stock. In our opinion, the omission of sections, sufficient drilling, metallurgy, and even structure make Southwestern a dangerous bet at these levels.

What about Ivanhoe Mines Ltd, with its big Oyu Togoi copper/gold project in southern Mongolia? Unlike Southwestern there has been extensive drilling and a prefeasibilty study has given us much information. However the huge capital costs together with the fact that much of the economic grade lies deeper and will not be sourced until later makes the economics questionable - even for Barrick.

Year of Exploration

Meanwhile, despite the lack of exploration successes elsewhere, we believe that the strong gold prices will spur renewed exploration efforts. We believe that not only will China be a beneficiary, but that on a global scale, we note that there is an increased emphasis on exploration. We believe that this year will prove to be the Year of Exploration.

The exploration and development sector has been badly beaten up, having failed to exceed last November's peaks when gold retested $427 an ounce. Earnings in the latest quarter were somewhat disappointing in that costs remain a problem. The merger of IAMGOLD Corp and Wheaten River Minerals Ltd. reflects the need for mining companies to create synergies since both were saddled with modest growth prospects. The intermediate producers led by Goldcorp have corrected in large part due to the fact that this group was widely held and investors sought easy profits. The dilemma for the industry is how to replace declining reserves. A higher gold price will help boost uneconomic reserves, but the industry needs to find new gold deposits. We continue to recommend an overweighted position in gold equities, particularly during this pullback. Stocks are extremely oversold and poised for rebound. And yes, we still target $510 per ounce this summer.

Our top picks continue to be Kinross, Agnico-Eagle, and Goldcorp. And among the junior developers, we continue to recommend Eldorado, Bema Gold, Campbell Resources, Crystallex International, Miramar Mining, Northgate Exploration.

Barrick Gold Inc. Barrick walked the talk and delivered into its hedge book lowering its exposure to 14.7 million ounces. At its annual meeting, Barrick reiterated its desire to eliminate its hedges, which we applaud since the mark-to-market deficit was $1.8 billion. At $510 per ounce Barrick would be offside by $3.1 billion. Results in the latest quarter were hurt by a loss on silver derivatives of about $15 million so hedging should carry "dangerous for your health" labels. Barrick should produce 5 million ounces this year but it too is caught in a classic dilemma, what to do for growth in the near term. Alto Chicama, Cowal and Veladero are projects planned for 2006.

Crystallex International Corporation

Crystallex released a 40,000 tonne per day flow feasibility study, which increased the price tag by about $116 million with annual production exceeding 500,000 ounces for the first five years of production. The feasibility study by SNC Lavalin allowed for the lowering of cost to US$153 an ounce including royalties. There is no question that the higher production scenario is attractive, however it might be prudent to begin with a 20,000 per day facility since the capital cost would be less. Crystallex successfully raised $115 million in an underwriting (Maison participated) and thus financing the lower 20,000 per day facility may prove easier in today's financing climate. Nonetheless, whether one models 20,000 tonnes per day or 40,000 tonnes per day, Crystallex is especially undervalued here. With new management, an improved balance sheet, and Venezuelan government approval, Crystallex is a buy.

Eldorado Gold Corporation

Eldorado shares have been beaten up partly because of increased taxes in Turkey. We believe that the impact of the increased taxes is modest and detracts from the excellent Kisladag project, which is scheduled to begin production in the second quarter in 2005. Eldorado has an excellent balance sheet and is well positioned to complete the development of Kisladag.

Goldcorp Inc.

Goldcorp results were excellent reflecting the benefits of the rich Red Lake mine, which produced 140,000 ounces in the latest quarter. Goldcorp recently lost two executives, which will not have an impact on operations. We believe that the company is well run and continue to recommend the shares here. Goldcorp held back a portion of its production boosting its inventory to 72,000 ounces. At yearend, the Company was penalized for selling its bullion but in hindsight that was a good move, since the gold price is lower today. Nonetheless, we subscribe to holding back some of the production believing that higher gold prices will benefit Goldcorp shareholders. We continue to recommend the shares for its excellent balance sheet of $365 million in working capital, no debt and for almost 600,000 ounces of annual production.

Kinross Gold Corporation

Kinross Gold shares were beaten up due in part to its leverage to the gold price despite increasing its overall reserve position. The elimination of contractors at Fort Knox will generate efficiencies. At Kubaka, in Russia, the go-ahead from Birkachan will add ounces. Refugio will begin crushing ore in the last quarter and commercial production will begin. Refugio will commence production at 40,000 tonnes per day with annual gold production beginning at 230,000 ounces (50% Kinross/50% Bema). Mine life extensions at Kettle River and Round Mountain improve next year's production profile offsetting the closure of 50% owned New Britannia. We continue to recommend Kinross for its leverage to the gold price and its almost 1,8 million hedge-free ounces make it an ideal takeover candidate. Buy.

Miramar Corporation

Miramar proposes to develop the Doris deposit at Hope Bay, 600 kilometers from Yellowknife, with a mining rate of 800 tonnes of ore per day, beginning next year. Underground access is to be provided from a ramp. The Boston deposit about 50 kilometers from Doris will likely be exploited later on with ore that could be trucked to the Doris mill facility. We believe that the initial output of 24,000 ounces with the project peaking at 130,000 ounces is realistic at this time. The low initial capital cost eliminates a "Cumberland" surprise. To be sure, the mill could be increased to process ore not only from Boston but the higher-grade Madrid deposit. Further, Miramar is conducting an active exploration program at Goose Lake this summer, which should generate some news. We continue to recommend the shares of this developing producer because of the multi-million ounce potential at Hope Bay.

Placer Dome Inc.

Placer Dome reported disappointing results due in part to continuing problems at South Deep in South Africa. So much money has been spent in South Africa for a meager 46,000 ounces produced in the latest quarter at $427 per ounce. Not only does Placer Dome have the bulk of its reserves in South Deep but expansion has been delayed yet again. Near term, Placer has to make a decision for the $1.6 billion Cerro Casale project in Chile, which is a lowgrade copper/gold deposit. The billion-dollar price tag together with the fact that Placer has to carry its partners makes this project dubious at today's prices. Placer's best project for reserve expansion is at Pueblo Viejo in the Dominican Republic. The Pueblo Viejo deposit is one of the largest undeveloped gold deposits in the world, with a geological in-situ resource totaling 34 million ounces of gold and 205 million ounces of silver. The indicated resource is believed to be about 16.8 million ounces of gold and 103 million ounces of silver. The oxide portions of the Pueblo Viejo deposit was mined between 1975 and 1993, producing over 5 million ounces of gold and 22 million ounces of silver. Placer Dome is finalizing a prefeasibilty study and is believed that the company is considering autoclaving the refractory deposit.

Placer is a well-diversified company that has long been rumoured as a takeover candidate. However, we believe that the company's hedge book together with its capital commitments in South Africa make the company an unlikely takeover candidate. The company recently issued a series of convertible debentures in order to finance its long-term obligations, which has put a cap on the stock price. Finally Jay Taylor is retiring in September and Placer's active board of directors must again look for a President, a task that this board has faced too many times (could the problem be the board?).