According to Investors Intelligence, cited in Alan Abelson's column in this weekend's Barron's, only 17.4% of advisory services are bearish on the stock market, the lowest reading since 1987. I hope that readers recognize what a rare experience they are being treated to when they read this commentary!

Speaking of a rare experience, a Seattle cartoonist has launched a movement among cartoonists for "Everyone Draw Mohammed Day" on May 20th. Because really, what could go wrong with that idea?

It seems like the populace is too busy making up stupid celebrations to eat their cake. Today marked the celebration of "Boob Quake," which was started by an atheist college student who believes that if women show excessive immodesty today and there is no earthquake, then the mullah in Iran who is the target of her ire will be forced to recant his statement (the thrust of which was that earthquakes are caused by women showing too much skin). Now, like any red-blooded American male I am generally in favor of college co-ed bosoms, but in this case it appears they caused a magnitude 6.5 earthquake. Nice job, ladies. I sense more government safety regulations in the offing.

Should it be disturbing to us that enemies of this country, scattered around the globe, arrange terrorist strikes on our citizens and allies, and our response is to draw cartoons and show our boobs? Well: eat, drink, and be merry, for tomorrow...

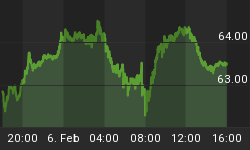

None of that affects the market, of course; but then again, almost nothing seems to affect the market anyway. As I warned on Friday, despite all of the good feelings about "a Greek solution being near" - which seems to happen every Friday - the situation is no more resolved than it was. The German Finance Minister told the Bild am Sonntag newspaper over the weekend (reported here and elsewhere), "The fact that neither the European Union nor the German government has taken a decision means it could be positive or negative." Darn it, there goes the apple cart again. As the chart below shows, 2-year Greek yields are up to over 13%...but the 10y is over 10% too. The market gives Greece about a coin flip to survive without default.

The Greek 2y Is High, But The 10y Is Nearly 10% Too!

In the U.S., however, the failure of a major nation-state and the potential for a run on similar nation-states isn't cause for alarm, apparently. True, equities did surrender 0.4% after trading higher initially, and the 10y Note contract did struggle to a 4/32nds gain (3.81% 10y yield), but this does not look like the stuff of panic.

The irrational exuberance is again winning the tilt against rational lugubriousness. As the latest exhibit in support of that proposition, let me point again to Barron's, this time their survey of money manager views on the economy. The survey question whose response jumped out at me was this: "What are the odds of a 'double dip' or second recession in the U.S. this year?" The responses were:

| • Odds: 100% | Responses: 4% | Makes sense; no such thing as a sure thing. |

| • Odds: 75% | Responses: 19% | A fair number of pretty bearish folks, but they know that 100% is crazy. |

| • Odds: 50% | Responses: 13% | A little less. |

| • Odds: 25% | Responses: 2% | Still less. Looking kinda bearish tilt so far. |

| • Odds: 0% | Responses: 62% |

Wait, what? Fully three-fifths of money managers feel there is no chance at all for a double-dip recession this year. That is crazy. Of course, 2008 taught us that there is no such thing as a certainty, and the bears in the survey seem to understand that, and there is no such thing as an impossibility, which the bulls don't seem to understand. Even if we are generous and recognize that this includes all the 1% and 2% answers, it cannot be very skewed, with 5% and 10% answers, or the "25%" answer bucket would have more in it than a mere 2% of respondents.

That's either irrational exuberance, or the stock market is being driven higher by people who can't do math. Or maybe both.

It is always nice to remember why I am so glad that I am not an equity guy, but in fixed-income. I wonder and worry about the equity folks, but for the most part it's like having an ant farm. It's fun to watch them looking so busy, and yet so single-minded and uncreative, and it's fun to occasionally watch them scurry about when someone taps on the glass. "What the heck was that?!? Let's get out of here! Save the queen! (I told you that you were showing too much thorax!)"

Not that we are always so sober and sedate in the fixed-income world, but since we're worried about a return of principal rather than a return on principal as our primary constraint, we spend much more time thinking about what could go wrong than about what could go right. Which is probably why bond people hang out with other bond people, because no one wants us at parties. And as for the inflation people, forget it. But I digress.

The FOMC, who has a meeting over the next couple of days, keeps talking about unloading its mortgage portfolio to shrink its balance sheet. I mentioned on Friday that I think this is a very bad idea, since the market is not likely to be able to handle another trillion-dollar-seller with aplomb, but there's another issue to be aware of as well. The Fed's purchase of $1.25 trillion of agency MBS not only took a lot of duration out of the market, it also took a lot of negative convexity out of the market. Owners of mortgages get higher coupons than on similar-duration Treasuries because of the embedded optionality in the payout: when rates fall, the security pays back principal; when rates rise, it pays off principal more-slowly than expected. In both cases, you have your money sitting at a lower-than-expected rate if there's a decent move, and this is compensated for through a higher coupon.

Many holders of mortgage securities therefore hedge these prepayments and extensions either by delta-hedging (this is what is meant when we say there was "convexity-related selling" in the market) to add or subtract duration lost or gained by the MBS, or by buying actual options. So when the Fed took all of those MBS out of the market, they greatly decreased the demand for vol, and as a consequence of that vol fell further, and faster, than people expected it to in the wake of 2008-2009.

But when the Fed starts selling those securities, the exact opposite will happen. Not only will it add duration to the market, but it also will increase the demand for volatility (as well as actual volatility, as investors hedge the embedded options or dealers hedge the real options that they sold to investors). This is one reason I like out-of-the-money puts on Treasuries - if the Fed starts selling mortgages, your options may rise in value due to an increase in implied volatility even if rates don't rise.

Tap, tap, tap. Wonder what will happen when rates begin to rise and vols start to creep up too. Tap, tap, tap.

.

The 5y TIPS auction today tailed 2.75bps from the pre-auction mark, which wasn't too bad for a 5-year TIPS auction. Of course, it wasn't great, and a low-ish indirect bid means that the Street owns a lot of the issue. I think it will clean up okay, though.

Tomorrow, Consumer Confidence (Consensus: 53.5 from 52.5) is due out; as usual, I will be looking at the "Jobs Hard To Get" subindex, which remains very high. That index needs to be moving to 40-42 before I get very excited about the employment situation improving. The Case-Shiller index is also out, but that isn't a market-mover; however, Chairman Bernanke is due to speak at 10:00 at the "Obama Debt-Reduction Commission," and will likely tell everyone there that deficits are bad. On the chance that he says something else significant, however, be alert!