I had planned to write yesterday, but I decided to first take a few minutes to watch a little tennis match and then...

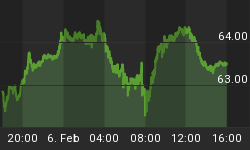

It now appears that the bond market is going to confound most prior forecasts and rally, putting 10y yields back under 3% (and, incidentally, pressuring pension funds once again as their liabilities rise in value even as their investments shrink). Despite heavy Treasury supply, the world economic situation appears again to be deteriorating and the run to quality is underway. (Whether or not Treasuries constitute 'quality' any more is a philosophical diversion we can take up at another time; the point is that - as has been said in a similar sense about democracy itself - Treasuries are worst form of investment except for all the others. There will be a future selloff that may be quite ugly, but for now Treasuries are still enjoying safe-haven status. (To be sure, however, in the context of what is happening globally the rally in U.S. rates is actually pretty tame, and this might be considered worrisome another day). Today, September 10y Note futures actually declined 1/32nd despite the selloff in equities, with 10y yields at 3.12%, but as the chart below shows the rallies on Tuesday and yesterday appears to be enough to push yields through important support (and to the lows of the last year). I expect a grudging rally that could take 10y yields as low as 2.50%.

10 year yields appear to be heading back down.

The underpinnings for the rally go back to the beginnings of the Greek crisis. Despite all that the ECB has thrown at the problem, and the great amount further that it has pretended to throw at the problem, Greek CDS today went to a new record and other sovereigns weakened as well. On Tuesday (after I wrote my commentary), French banking giant BNP was downgraded a notch by Fitch to AA- from AA. These are canaries in the coal mine. And need I note that France and Italy are both out of the World Cup in the Group Stage? Europe is in bad shape economically and morale is low.

But the U.S. is hardly without its problems. Yesterday, New Home Sales shocked most observers by falling to a record low (since 1963) of 300k units. It's a bad sign when New Home Sales is coming in consistently below Initial Claims (Claims fell today, but from a high level last week, so they're still just floating along at a high level). The chart below (Source: Bloomberg), perhaps flippantly, shows the 4-week average of Initial Claims graphed against the seasonally-adjusted annual rate of New Home Sales. Neither is adjusted for population growth since they both ought to respond to population growth. It is interesting, I think, how the recessions of the mid-70s, the early 80s, and even the recession of the early 90s each involved the crossing of these lines. (And perhaps this illustrates how big the housing bubble already was in the early 2000s recession!)

Claims remains above New Home Sales

Now, the fact that the Federal Reserve has finally admitted that conditions are not entirely rosy at the moment is encouraging, although that is of course one reason that yields will likely fall: it is now clear to them what has been clear to most of us for a while, and that is that the European problems are not going to spontaneously heal themselves. I have previously mentioned how surprising I found it that the FOMC statement seemed to ignore the huge jump in stress that accompanied the Greek crisis; this has now been remedied as the statement yesterday mentioned the impact that "developments abroad" have had on "financial conditions" becoming "less supportive of economic growth on balance."

Over the last couple of days, things have been playing out surprisingly like I thought they might, with bonds up and stocks down pretty sharply (-1.7% today). I don't see any reason to think that we have seen the full depth of the equity selloff; volume was heavier today but still quite light overall, and the VIX is merely up to 30. Not that we should be expecting a selling climax with the indices in the middle of their recent ranges, but it is a little surprising how orderly the selloff has been so far.

I doubt we will be so lucky going forward.

Friday's data is second-tier, with the final revision to Q1 GDP and the monthly revision to the Michigan Confidence number. Monday will also be boring data-wise, and we may well need to wait until Chicago PM and Unemployment next week before we get significant economic news. Meanwhile, however, the slow-motion train wreck that is the global economy will be pressing forward, with quarter-end due next week. I don't know what good things might happen or what bad things may happen, but presently it seems there are more alternatives for the latter.