The early call is for a lower opening on Wall Street this morning, in what appears to be profit-taking or position evening ahead of the start of earnings season next week. Unless the market gets a jolt from a much better than expected Wholesale Trade or Inventories report today, I'm looking for the stock indices to remain range-bound, very similar to Thursday's sluggish intraday action.

Sentiment is shifted overnight toward risk aversion leading to a stronger Dollar this morning. This morning's change in risk sentiment represents just how fragile the investor is at this time. Look for the Dollar to stay in a range with a bias to the downside. Commodity-linked currencies are likely to feel the most heat.

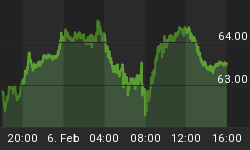

To recap Thursday's trade, the September E-mini S&P 500 hemmed and hawed throughout the middle part of the day but still managed to post a strong gain into the close. Thursday's rally was triggered by a better than expected U.S. Weekly Initial Claims Report and renewed appetite for risk.

Investors have been gobbling up stock for a few days because frankly no one likes the payout being offered by the Treasuries. In addition to speculation that interest rates will remain low for a prolonged period of time because of a weakening economy, investors are also anticipating a robust earnings season.

This week's strength in the stock indices has caught the shorts by surprise, forcing them to cover their positions. On Thursday the September E-mini S&P 500 reached a minor 50% retracement level at 1166.00. Holding above this could trigger an even further rally to 1181.00.

So far the action in my opinion has been short-covering, but there seems to be a lot of power behind this move which could be painful for stubborn short traders. The question is whether there will be one more test of the recent lows in the indices to solidify the bottoming formation.

The better than expected Weekly Claims number helped drive up yields on Thursday, driving September Treasury Bonds and T-Notes lower. Although it is unlikely the trend will turn down in the Treasuries until the economy gets back on track, the charts are indicating that a correction is due.

Look for a pullback in the T-Bonds back to at least 125'15 to 124'24 and in the T-Notes to 121'12 to 121'00. Yesterday's reaction to the upbeat claims number should serve as notice to bullish traders as to how fast the Treasuries can turn south if a series of economic reports begin to show improvement in the economy.

The September Euro rallied early, traded in a range then made a move to the upside in a lifeless trade on Thursday. Volume appeared to drop off throughout the day following the European Central Bank's policy statement announcement shortly before the start of the New York session. For the most part, the Euro seemed to be taking its direction from the U.S. equity markets.

Earlier this morning the European Central Bank said that interest rates would remain at a historically low level. While this was expected, traders turned their focus toward ECB President Trichet's press conference.

Trichet mentioned that the ECB will continue to provide unlimited stimulus and liquidity to the financial system but the news that really helped move the Euro higher was his "lack" of comments on the bank stress tests. The fact that he didn't say anything negative about the tests may have actually instilled confidence in investors.

Investors have been pessimistic about the bank stress tests because they feel that they may not be stringent enough to reveal any serious problems with the bank balance sheets. They had been expected Trichet to reveal a little more about the scope of the tests but had to settle for limited commentary. Since he didn't say much other than investors should wait and see the results before judging, traders decided to take the "no news is good news" approach and rallied the Euro. The only negative that could have been construed by investors was his comment that banks may have to recapitalize after the publication of the stress tests.

Thursday's friendly U.S. Weekly Initial Jobless Claims Report helped bolster stock index futures before the opening, sending the Euro and commodity-linked currencies higher. As stocks began to weaken as the session approached its mid-session, traders began to take profits in the Euro. The strong finish in the stock futures markets helped drive the Euro up into the close.

Technically the Euro main trend is up on the daily chart. This market has entered a key retracement zone at 1.2609 to 1.2782. Holding the latter number is considered a sign of strength.

Based on the current trading action in the market, it looks as if the direction of the Euro will be determined by the movement in the U.S. stock market. As long as demand remains firm for equities, traders should look for continuing strength in the Euro.

Despite the pick-up in demand for higher yielding assets and the generally weak tone in the Dollar, the September British Pound finished lower.

On Thursday the Bank of England left interest rates unchanged as expected. The BoE is most likely going to leave interest rates at these low levels for a prolonged period of time because of the new financial austerity measures proposed by the new government. The BoE is concerned about high inflation but cannot risk a double-dip recession by hiking interest rates prematurely.

Yesterday the U.K. reported an increase in industrial production in June but traders ignored this news saying the increase merely was an offset of the sharp sell-off in industrial production during the height of the recession. Thursday's weakness was attributed to another drop in housing values. This report indicates that the economy is still weak and could trigger a curtailing of spending by the consumer.

The sharp rise in U.S. equity markets helped boost demand for higher yielding currencies. All three commodity-linked markets - Australian Dollar, New Zealand Dollar and Canadian Dollar - experienced substantial gains on Thursday.

Technically, the Aussie and the Kiwi closed near previous main tops which put them in positions to change their main trends to up on the daily chart. Watch for an acceleration to the upside in the September Australian Dollar on a move through .8858 and a similar move in the September New Zealand Dollar on a trade through .7159.

The September Canadian Dollar is still in a downtrend, but upside momentum is building which could help trigger a change in trend to up in the short-run. The bigger picture still indicates that this market is rangebound between 1.0064 and .9208.

Risk appetite could get strong if U.S. equity markets can overcome nearby retracement zones. This increased demand for risk should continue to underpin the Euro and the commodity-linked currencies while putting pressure on the lower yielding U.S. Dollar and Japanese Yen. Clearly, traders don't like the low yields being offered by the Treasuries and are willing to take on more risk to get a better return at this time.