The following article does not constitute a solicitation to invest in the program described in this article. An investment may only be made at the time a qualified investor receives the commodity trading advisor's disclosure document. Futures and options trading is not suitable for all investors. Past performance is not necessarily indicative of future results.

"Behold, the fool saith, 'Put not all thine eggs in the one basket' which is but a manner of saying, 'Scatter your money and your attention,' but the wise man saith, 'Put all your eggs in the one basket and... watch that basket.'"

Such is the wit, humor and wisdom of Mark Twain that he succinctly encapsulated in the quote above the conundrum that investors face both then and now. The problem is the tradeoff between lower volatility and muted returns resulting from diversification, versus increased volatility but potentially higher returns which comes from selective investment choices.

Take for example an investment portfolio made up of mining shares only. If you were to invest in all of the mining stocks available in the US markets, then your returns would reflect the general direction of all such mining stocks. This mean return is often referred to as "beta". However, if you were to invest selectively in only a few of these mining stocks, or time when you bought and sold them, then your skill would have a greater influence on your overall returns. Such skill-based investment decisions is called "alpha" by portfolio managers.

This issue becomes acute when investing in commodity assets such as gold or silver. Unless you are engaged in the timing of when to buy and sell, you are basically beholden to the ups and downs of the market over which you have no control. So what is an investor to do?

Until the millennium there were only a few ways to invest in gold and silver. One could purchase the physical asset in the form of bullion, coins or jewelry; or you could invest indirectly vis-à-vis mining stocks or related companies; or you could trade precious metals futures contracts.

There is, however, another way of investing in metals called managed futures. Sophisticated investors have long known about managed futures as an arena in which to obtain skilled-based returns from professional money managers. Not only that, unlike the hedge fund universe, this sector of the industry is highly regulated and accessible to small and large investors alike.

As a managed futures specialist it is my job to scour the universe of managers, called commodity trading advisors or CTAs, and help my clients allocate to these specialists. What I want to tell you about today is a managed futures program that trades gold and which really impressed me as unique.

Most CTA programs are active traders -- in fact, one could say that the primary source of returns in managed futures is skill-based. The problem with a pure trading approach, however, is that it doesn't provide an asset-based return (ie, beta) that investors may be seeking to enhance their overall investment portfolio. Not so with the Gold Covered Call Writing program -- like gold ETFs it invests in gold only from the long side.

Unlike other managed futures programs, the Gold Covered Call Writing strategy maintains a perpetual long-only gold futures position which essentially duplicates the exposure to gold prices. But there is another dimension to this strategy which is value-added and comes from using call and put options to both generate income and provide downside risk protection.

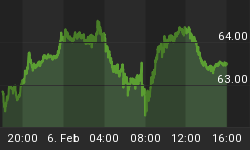

A great way to understand how such an approach can provide risk adjusted performance is to compare the returns of gold ETFs with the returns of the Gold Covered Call Writing program. But first, let's take a look at the chart below which shows how just volatile gold has been in the last few months:

As you can see, gold was trading in a sideways range until September 2009 when the market turned bullish and then frothy during November. In December 2009, however, gold prices dropped dramatically and then entered into a very choppy range which continued until March 2010, at which point it resumed a bullish trend until it dropped dramatically in July 2010. It is important to note that past performance is not necessarily indicative of future results. The question is, where does gold go from here?

Now here is a comparison of the performance returns between the most popular gold ETF, GLD, and the Gold Covered Call Writing program since inception through August 27, 2010:

What is notable is that in four out of ten periods GLD suffered down months, while the Gold Covered Call Writing program only suffered two down months. And in many periods, this strategy outperformed GLD with less volatility overall. How can this be the case?

The answer is in the use of options, specifically the covered call writing strategy. Covered call writing is the name given to the strategy in which one sells a call option while simultaneously owning the underlying asset. This approach works best in a mildly bullish or neutral market conditions, and even incorporates limited insurance to the downside if the asset declines somewhat.

What makes the Gold Covered Call Writing program so interesting is that the income stream generated from selling covered calls is similar in concept to gold loans which evolved in 1980s. This activity came about as a means for central banks to earn a return on their inventories to cover warehousing costs. In other words, if gold trades sideways the program still has the potential to generate positive returns unlike gold ETFs whose NAVs will remain stagnant in range-bound conditions.

Since the program launched it has been capturing between 3% -4% in net premiums per expiration cycle. In the real world, however, gold prices are volatile and go down as well as up which in turn will impact the overall returns of the program. Nevertheless, it is expected that the premiums captured from writing calls will over the long run reduce such volatility, and so far that has been the case.

One thing to note, however, is that the covered call strategy does limit profit potential as the graph above shows. Accordingly, investors may not fully participate in a strong upward move like what happened to gold in November 2009, unless the call is rolled to a higher strike. This is where the skill-based aspect comes into play with the CTA making such trading decisions. Part of this discretion includes the purchase of puts which acts like insurance in order to further protect downside volatility.

There is still another aspect of this program which makes it much different from gold ETFs. Institutional investors like to be efficient with the use of investment capital and thus often use leverage to achieve their goals. Given current prices, in order to have the same exposure as one gold futures contract, you would have to invest around $114,000 in the GLD ETF. The Gold Covered Call Writing program, however, achieves the same exposure with just a $50,000 investment, resulting in approximately 2:1 leverage.

Please note that the use of leverage can work both for you and against you, and investors should first make sure they fully understand this important factor when investing in managed futures. If you want to learn more about the use of margin in managed futures, we would be happy to explain.

So to review... the Gold Covered Call Writing program provides an alternative way to invest in gold that is both transparent and liquid due to its "separately managed accounts" structure. It encompasses leverage which enables a $50,000 investment (or less) to be equal to the face value exposure of one futures contract (price/ounce x 1000). And the program uses options in order to generate an income stream from premium capture, as well as provide limited downside risk protection. Year-to-date, the program is up +7.17% for the first quarter (estimate for April is additional +1.5% as of 4/23/10).

In summary, the performance of the Gold Covered Call Writing program is derived from a combination of the underlying long gold futures contract, the "covered call" strategy (premium capture) net the cost of "put insurance" to limit downside risk, and leverage as a function of the futures contract's face value.

Now, how does one get started in learning more and how to invest in this program? Easy! Start by going to this webpage http://www.capitaltradinggroup.com/promo/gcc.cfm and completing the form. We'll respond by providing you with a brochure on the Gold Covered Call Writing program and start sending you monthly performance updates. Or if you are interested in investing now, you can email me at nsloane@ctgtrading.com or call (800)238-2610.