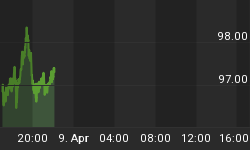

A small aftershock is rippling through EU bond markets these days. Today Moody's downgraded Greece 3 notches to B1, citing lagging tax collections and "implementation risks' that are increasing odds of a default event. In general, I am not a big fan of ratings agencies and I think they tend to be considerably behind the curve when it comes to ratings changes (and sometimes, in the wrong direction), but this serves to highlight the fact that not everyone thinks the European sovereign bond crisis is over. While it is no surprise that Greek 10y bonds did poorly on the news, you may not be aware that Irish and Portuguese 10y government bonds are also both at long-term highs today as well (see Chart).

![]() Larger Image

Larger Image

Greek, Irish, and Portuguese bonds are all near their highs in yield although no where near their highs in angst.

Oil was up again today; although it backed off to end up only 1% or so, WTI is above $105 now. RBOB Gasoline declined 4 cents but is still over $3.

The stock market dashed out of the gate, and then subsequently dashed itself upon the rocks. The S&P ended 0.8% lower but had been toying with last week's lows around mid-day. The VIX moved back above 20. Volume was again right around 1bln shares.

Bonds, despite the decline in stocks, also fell slightly with the 10y yield up to 3.503%.

The movement of stocks and bonds are consistent with markets that are working off over-bought and over-sold conditions and just chopping around in the meantime. That is more than likely what is going on. But the movement of European bonds is less hopeful. The movement to lower volatility but a consistent slip higher in yields could be a sign that pressure is slowly being released, that these markets were being artificially supported by the ECB and are gradually being allowed to slide back to their true equilibrium levels. If this is true, it is just a water torture being visited on the banking institutions that hold so much of this risk, building pressure there.

Alternatively, the steady move to higher yields could be a sign that banks are releasing their bonds steadily into a market that keeps backing up bids. In that case, the pressure is being released from the banks but building on the market itself. At some point, either the banks will finish selling and the bond market will stabilize, or - and this is the bad case - the bids will decide they've had enough, the market will evaporate, and a sharp break will occur. Given the size of the exposures that many European banks have to periphery sovereigns, I'm not super optimistic that homes can be found for all the paper at yields that allow the sovereigns themselves to continue to access the capital markets and thereby service the bonds.

But notice that if either of these are true (and it may be that neither is true, and that these are just markets adrift with no one participating or having much exposure - but I doubt that), the formula is that steady pressure is being applied either to banks' economic capital (although not regulatory capital since sovereigns can be treated as being worth par at maturity) or to the bond markets themselves.

Perhaps I'm just thinking in this way because today I have been musing about nonlinear effects in financial markets as I am working on building a model of inflation expectations in which expectations are anchored within a range defined by the way people think about inflation ("low', "medium', or "high' for example) and remain in a range as pressure builds until abruptly there is a regime shift to another equilibrium. So, for example, perhaps people perceive inflation as "low,' and will persist in that belief for a while even if inflation outturns are "medium' for a while. But eventually, I think, the herd shifts to the new equilibrium in what is probably a non-linear break.

Lots of ink has been spilled on the issue of non-linear dynamics in complex systems. Some of my favorites are Ubiquity: Why Catastrophes Happen by Mark Buchanan, Paul Ormerod's Why Most Things Fail: Evolution, Extinction and Economics

, and Why Stock Markets Crash: Critical Events in Complex Financial Systems, by Didier Sornette. The simple summary is that if you apply a steady force away from equilibrium in a system that wants to return to that equilibrium, something's gotta give. Either the system returns to the equilibrium position, or it moves into a new equilibrium (if this is a piece of steel, the transition is called "breaking'). In principle, the system can stay near a transition point for a long time, but sooner or later it goes one way or the other.

(Don't quibble about the finer points of my definition - it was after all a very brief summary).

Applied to the European periphery, the "transition' could come when suddenly bank credits adjust, or it could come (in the other case) when the bond markets collapse. Of course, neither transition is assured, and the system might return to a stable equilibrium.

Applied to the economy, growth might do just fine with oil at $95, $105, or $115/bbl, but then the economy abruptly rolls over at $118.21.

Applied to inflation, CPI might move gently from 1.0% to 2.0% to 3.0%, and then snap suddenly to 6.0% (this sort of outcome is more likely if expectations serve some sort of anchoring function/feedback mechanism, which I am not confident of).

I am not predicting, mind you, any of these things. My point is only to highlight that markets are generally in equilibrium but it need not be a stable equilibrium. Markets that are at extremes are prime candidates for ones that are nearing transition points, which is why we watch breakouts.