From the February 21, 2011 Hard Rock Analyst Dispatch

With Libyans having joined the movement to overturn aging autocracies the Arab street action has moved into a geopolitically more difficult territory. Concern over Libya's oil exports are showing up as higher crude pricing. Libya's 1.6 M barrels/day of crude output may well undergo disruptions, but the Saudis could replace that if prices move high enough to cause concern. As troubling is the unpredictability of Muammar Gaddafi and those around him. They seem more likely to go down fighting than the western leaning autocrats have been, and that is more likely to cause splintering of the country and concern similar shifts elsewhere in the region. Markets are reflecting this heightened uncertainty with continued gains for precious metals and US$ as well as oil. We expect the US$ and oil to peak before gold and its cousins do.

Base metals have been trending lower as would be expected during Dollar strength, but broader considerations are also part of this. Traders managed to push copper through $10,000/t ($4.56/pound), but that 5-figure copper pricing has acted as a ceiling. More analysis is now focused on the growth of on-market stockpiles and the unknown size of off-market stocks, plus increased efforts to cool emerging market growth. Traders have begun listening to those concerns as much as to Arab street rallies. The share prices of First Quantum (FM-T, FQM-L), Capstone (CS-T), Lundin (LUN-T, LNUMF-Q) and most other copper miners began declining ahead of the metal's peak. Since Dr Market tends to trump Dr Copper, this more cautious mood around the red metal is likely to last. Waiting for weakness in the subsector should pay off.

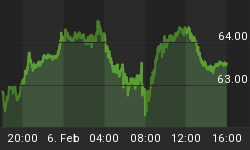

Gold's early year price decline reversed during Egypt's street action. The new uptrend continues and has steepened as the movement spreads over North Africa and southwest Asia (see chart next page). This comes as gold's 60% price gains of the past two years finally shows up in the bottom lines of yellow metal producers. For some miners the earnings gain has been in the 100s of percent over last year. These include number one producer Barrick Gold (ABX-T, N) and intermediate producer Agnico-Eagle (AEM-T, N). Like most miners the gold producers pulled back in early year profits taking after strong run ups at the end of 2010. This combination may have set up the answer to a valuation question of ours.

Gold producers have long garnered high P/E ratios, unlike base metal miners that traditionally sported fairly low ratios. High gold company ratios have been justified on the basis in-ground gold reserves, which must have left base metal players felling like chopped liver. We have said before that this secular bull market for metals, or super cycle if you prefer, could close that gap. For the past few years gold producer prices have not kept up with the metal's gain. This has partly been an issue of miners paying down past expenditure while dealing with rising costs such as for steel and energy. A number of gold miners seem to have put those issues behind them for now.

When Barrick's 2010 results came out they showed a trailing P/E at half the +30 multiple it had seen in some past years despite a strong share price recovery through last year. The Agnico-Eagle P/E was similarly priced at half the extraordinary +60 P/E of some past years when its stellar 2010 results came out. In the several days since Barrick gained nearly 4%, helped by gold's own price gain, to sit at a trailing ratio of 15.7. Agnico however has slipped almost 8% over those several days to sit at a still impressive trailing P/E of 35.7. While Barrick is obviously likely to continue its gains in this market, reaction to 2010 results for these and other established gold miners will stabilize a sector gaining a broader, balanced audience as an insurance holding. As the market settles on what it will pay for producers they will be more likely to seek new resources amongst junior players.

Silver is making this year's second set of new 30 year highs, and we expect that to continue. The moon metal is always more volatile than its yellow cousin. In the current environment its smaller market could get pushed that much more than usual. We would also point out that a gauge of P/E standards for silver is even tougher than for gold. Even after silver tripled and quadrupled many small producers struggled to generate any E but still managed share price gains along with the metal. The silver sector could undergo a re-ranking similar to that gold seems to be in, but not while the current run continues.

Thoughts on the base metals side of the earnings equation can await more numbers from them, but the buying up of copper juniors speaks to a group that is happier with its market. Though share prices would slide in the space along with metal prices, it would take a much larger dips than we expect to put any actual deal making off side. For the time being patience on the buy side is most likely to be rewarded longer term.

It's a secular bull market for metals and resources. We've been saying that for ten years. And we've been right. HRA initiated coverage on 19 companies since early 2009 - the average gain to January 12, 2011 is 309%! We're constantly reviewing companies for potential addition to the HRA list so there are sure to be more winners going forward. Of course, you won't know about them unless you're a subscriber!

Another thing we've been right about is the growing importance of the Yukon as an exploration destination and, more recently, Area Play. HRA was there early and continues to follow several of the biggest winners in the play. To watch Eric Coffin's latest Yukon Area Play Crescendo video (Feb 2011), please click here now to access it for free for a limited time!