The tragic comedy continues to disgust and delight, depending on your position and demeanor.

Today S&P revised its long-term sovereign outlook for the U.S. to negative. Stocks didn't like this very much, and promptly sold off 2%; the dollar also dipped and Treasuries went from very positive to somewhat negative on the day. However, the dollar and bond dips didn't last very long. The outlook for the U.S. fiscal situation is long-term negative, no doubt; however, the outlook for the European fiscal situation, and the condition of her banking institutions and member nations, is short-term negative as well and this concern rightly dominated today.

Last week's slaughtering of PIIGS continued today, with Greek 10y yields up 66bps even as the regime crosses its heart and says that no restructuring is planned. Where have we heard such promises before? Oh yes, I remember - when they said they wouldn't need assistance in the first place.

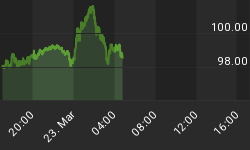

Irish and Portuguese yields were also higher on the day, but of more concern is that Spanish 10y yields rose to the highest levels since 2000 (see Chart below, source Bloomberg).

Spanish yields are at 10-year highs.

This is probably a good time to remember that it was only 11 days ago that the ECB hiked interest rates. Muchas gracias, ECB! And then there was this as well, from an Associated Press story:

"Meanwhile, another European country is weighing on markets too - but this one has no debt problems. News that a euroskeptic party made big gains in Finland's election Sunday has stoked fears that the EU's "comprehensive plan" to deal with the debt crisis may not run as smoothly as hoped."

I have always thought that one of the more amazing aspects of the entire Euro crisis has been that investors seemed to assume that continued unanimity of the Euro members...for unanimity is required before bailout monies can be disbursed...was the more likely case. Anyone who has ever walked into a movie rental shop with a family of four to choose a movie should have been skeptical that the apparent unanimity would hold. To pirate the old line about a fool and his money, the amazing thing is that they ever got together in the first place.

So the Euro has taken a hit, giving the dollar something of a breather even though the long-term outlook for the U.S. sovereign bond rating has worsened. The fact is that the rolling crisis in Europe has practical consequences, while S&P's report on the U.S. fiscal situation does not. It surely can surprise no one that the state of fiscal affairs in the U.S. is in a parlous state. And an actual default remains extremely unlikely (the Fed can always continue to print money to pay for government expenditures), especially while most public debt is held domestically. So the S&P report has no real significance, which is why bonds and the dollar snapped back after the knee-jerk reaction. The fact that equities did not snap back very much, ending the day -1.1%, tells you something about the sponsorship for the market at these levels.

The 10y note ended at 3.37%, and a mere 0.76% on the 10y TIPS bond. That's the lowest real yield since December. Commodities continue to look the least-worst of a number of inflation-related markets. Energy dropped back today but NYMEX Crude is still at $107.30 and continuing to defy many recent predictions of cataclysmic collapse. But grains, livestock, and precious metals all rallied today despite the dollar's strength.

There was no important data today, but Friday's CPI figures were near expectations at +0.549% on the headline number and +0.135% core (I'd suggested there was downside risk to the +0.2% consensus). Housing accelerated further, to 0.780% y/y from 0.657% y/y as of last month, but the pace of acceleration slowed as I'd expected. As the table below shows, most of the major groups are accelerating or going sideways, with the modest and surprising exception of Medical Care. Apparel decelerated this month, but it tends to jump around quite a bit. No group is decelerating markedly.

| Weights | y/y change | prev y/y change | 3m y/y chg | |

| All items | 100.0% | 2.682% | 2.108% | 1.496% |

| Food and beverages | 14.8% | 2.781% | 2.236% | 1.481% |

| Housing | 41.5% | 0.780% | 0.657% | 0.287% |

| Apparel | 3.6% | -0.645% | -0.421% | -1.077% |

| Transportation | 17.3% | 9.829% | 7.100% | 5.290% |

| Medical care | 6.6% | 2.734% | 2.891% | 3.275% |

| Recreation | 6.3% | -0.069% | -0.143% | -0.766% |

| Education and communication | 6.4% | 1.119% | 1.229% | 1.292% |

| Other goods and services | 3.5% | 1.803% | 1.959% | 1.901% |

On Tuesday, Housing Starts (Consensus: 520k from 479k) is expected to rebound from last month's dismal performance. If it does not recover a fair amount, it will be very discouraging to current growth expectations - the current assumption is that the previous dip was weather-related. The European developments will probably still be more important for the markets’ near-term direction, however.