Rotten economic data caused equities and energy to penetrate key levels this morning. In an utterly shocking news flash, Housing Starts were miserable at only 523k, although last month was revised higher by 36k. We should try to be even-handed here. Just as the jumps in Housing Starts in 2010 and early this year were nothing to get terribly excited about when put into the proper context (see Chart below), so too we ought to avoid growing too morose about the 10.6% fall in starts this month.

The "lazy L" recovery in Housing Starts.

Any way you slice it, the housing market is in hibernation and this surely isn't a big surprise. Somewhat more surprising was the fact that Industrial Production was unchanged and Capacity Utilization declined a tick from last month's downwardly-revised 77.0% (was 77.4%). The surprise was blamed on downstream effects from the interruption of Japanese production (especially in autos) following the tsunami/nuclear crisis. See the Chart below.

A pretty sharp recovery in Cap U, but there's more "output gap" left - if that matters.

It is easy to see why many policymakers roll their eyes at people who warn of inflationary consequences to too much money. If you believe the output gap matters, then here is another soothing metric! Underutilization of labor is represented by the high unemployment rate. Underutilization of physical plant is represented by the low Capacity Use figures. If the output gap matters, then we ought to have been in deflation and we ought to probably still be there. As I am fond of pointing out, this just doesn't square with historical experience - big output gaps do occasionally exist contemporaneously with inflation.

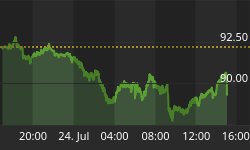

The initial reaction of markets was as you would expect, but the more dangerous because of the proximity of several markets to important support. For example, no matter how you draw the lines the S&P today broke through what is ordinarily solid support at the apex of a triangle (see Chart).

Doesn't really matter how you draw the lines, this is pretty ugly.

Wherever you went to techie-school, that's a bearish chart that shows an upside breakout from a rising triangle, a re-test, and a then a fail through the apex. NYMEX Crude held the important level at $94.50 and rebounded, but the risk remains (on the other hand, grains did well again as drought conditions - ironically - have caused the winter wheat crop condition to be rated the worst since 1996). The 10y Treasury rallied to 3.11% and is at the highs (low yields) of the year...just as the Fed is preparing to end QE2, by the way.

While a downward adjustment in equities makes sense, a severe move in other markets (bonds, dollar, commodities) really doesn't in the absence of crisis. Bonds, arguably, are already at crisis levels (although in the Lost Couple of Decades in Japan, obviously rates got substantially lower than they are now, here). So we remain on crisis watch. Never has the most-likely source of the next crisis been so clear, but it is the timing no one is sure about.The headline on Bloomberg was "EU Sees Possible Greek Debt 'Soft Restructuring' in Aid Bid," but linguistic gymnastics aside (if I were to extend maturities to, say, 100 years and declare a 10 year interest holiday, is that a 'soft restructuring,' a 'reprofiling,' or a default?) the first paragraph ought to be chilling.

"European finance ministers for the first time floated the idea of talks with bondholders over extending Greece's debt-repayment schedule, saying that last year's 110B-euro ($156 billion) rescue has failed to restore the country to financial health."

When is a rescue not a rescue? The EU undertook to save a lady on the 10th floor of a burning building with an 8-floor ladder. Actually, the analogy needs a further detail, because the woman is in the process of climbing higher in the building and all the fire department has is an 8-floor ladder. Anyway, isn't it just a little frightening that $156bln kept the wolf from the door for only a year? Do you think any of the European legislatures who need to vote on the $116bln Portugal bailout are looking at that vote a little differently right now?

It seems scarcely believable that the EU finance ministers actually expect to convince anyone that there is an end game here that represents a win for the strategy of 'keep bailing them out to keep the Euro whole.' But for markets, the question continues to be the timing. In my view, I would rather be short equities and that rotten chart, protecting my backside with cheap options (or a set-it-and-forget-it stop), than long the bond market where the biggest buyer is about to exit the stage and a lot of bad news seems to be priced in.

On Wednesday, the only scheduled event of note is the release of the minutes of the most-recent FOMC meeting, at 2:00ET.