Can one billion Benjamins be wrong? Actually, it's more like 1.57 billion hundred-dollar-bills (aka "Benjamins") that the EU and private bondholders are committing to the defense of Greece - inexplicably, the number in articles today was €109 billion, rather than the €160 billion mentioned in articles last week. Despite that band-aid, today Moody's cut Greece another three notches and declared the bond exchange equivalent to a default. Said the agency: "While the rating agency believes that the overall package carries a number of benefits for Greece - a slightly reduced debt trajectory, lower debt-servicing costs, as well as reduced reliance on financial markets for years to come - the impact on Greece's debt burden is limited." So, kudos to the EU, which managed to spend a deci-trillion (we might as well use the units we're going to be seeing more and more) and still not do muchfor the problem!

Greek 10-year yields rose 25bps today - along with Spanish and Italian and Portuguese yields - reversing only a small part of Friday's plunge but keeping 10-year yields for the saved country still around 14%. Irish 2-year yields rose 77bps, despite the fact that the EU pledge for Greece also promised a break on interest for Ireland.

The S&P index started the day very weak, after trading down as much as 19 points overnight. Bloomberg claimed that U.S. equities were falling because there was no debt ceiling deal over the weekend - I am not sure who was expecting one, but they seemed to think our legislators will try to get things done before the eleventh hour. The explanation seems weak to me, because it doesn't explain why European equity markets were falling (the Euro Stoxx 50 fell 1.1%). The main reason for weak markets is that (as Moody's pointed out) the grand plan out of the EU last week really did very little to (a) ensure Greece won't really default a little down the line, (b) ring-fence the other countries with bad fiscal issues, or (c) give us any confidence that they're capable of handling the next problem.

To be sure, timing is everything. We are all fairly confident that there will eventually be a debt ceiling deal. We all know that stocks will jump on the news of the deal, no matter how much they have rallied in anticipation of the news or on prior rumors of the deal. We all know that bonds will probably rally on the news. And so we're all waiting to sell into that pop, which consequently may not end up being very much of a pop. So volumes continue to slide since no one really wants to sell right now, and buyers also figure that if they wait there may be lower prices after the post-deal correction.

After the weak overnight session, stock prices did drift higher before fading into the close. Bonds didn't do much of anything although yields slipped a couple of basis points higher. Gold set a new all-time high, but grains and softs pulled commodity indices slightly lower on the day.

The only economic data were a couple of lesser manufacturing indices, with Dallas a little stronger than expected (and showing a big bounce from last month) and Chicago a little weaker than expected.

Inflation swaps rallied again. The 10-year inflation swap rate is now at 2.85%, only a whisker away from the year's high around 2.90%. 10-year inflation expectations haven't been higher since before the crisis...and at the time, crude oil prices had just doubled over the prior year so some amount of nervousness was evident and understandable. Over the last 52 weeks, oil has only risen 25%, and core inflation is much lower now than it was in 2008.

You can think of a future inflation measure like this as being something like the median expected inflation plus an option premium to account for the value of the tail, which is much longer to higher inflation rates. In that context, you could say that in 2008, with core inflation at 2.4% and 10-year inflation expectations at 3.0%, you were paying 2-2.5% for the expectation that the average would be slightly above the Fed target over the next decade, plus 0.6% or 0.7% as an option premium. Right now, with core inflation around 1.6% and many people still believing that deflation is a not-unlikely outcome (to be clear, however, I myself view that as a very remote possibility), you could argue that you're paying 1.75% or 2.0% for the expectation of the average and more than 1% as an 'option premium.'

In other words, people aren't paying 2.85% on 10-year inflation swaps because they expect inflation to be so high; they are paying 2.85% because they think there's a good chance they lose 100bps but there's some chance they make 500bps or 1000 bps. Moreover, in the case where the investor loses 100bps on his inflation swap, the rest of his stock and bond investments are likely to do comparatively well, but the "tail" case of higher inflation will splatter both stocks and bonds, so it's the right option to buy.

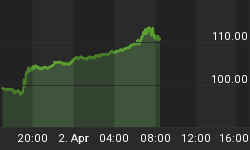

The reason that "option premium" is so well-bid is for the reasons you might naturally think of: a deterioration in the credibility of central banks, the narrowing list of plausible escapes from our current fiscal predicament. More recently, too, there is the observation that money metrics are no longer comatose. The chart below is worth taking administrative note of. It shows commercial bank loan growth over the last 52 weeks.

Bank Credit just went positive on a year-over-year basis!

Simply put, commercial loan growth has finally stopped shrinking. Some people will say that means that loan demand is picking up; I believe this means that loans are now more available than they were - it is a supply-side phenomenon. In either case, it is a sign that more-normal functioning of the banking system is returning. I happen to think the timing of such a phenomenon is exquisitely poor considering what is likely to be happening in Europe, but the numbers are clear. In just the last month, commercial loans have expanded at a 10% annualized pace.

So let the good times roll, except for the nagging issue that if the economy's lending organs are no longer impaired, it increases the risk that the money multiplier might make a comeback sooner rather than later.

Tomorrow, the Consumer Confidence (Consensus: 56.0 from 58.5) figure is due to be released with the consensus expecting a decline to new 2011 lows. As usual, look for the "Jobs Hard To Get" subindex, which last rose to 43.8. New Home Sales (Consensus: 320k from 319k) is a number that is simply not very important as long as it is under 400k or 500k, but be alert to a knee-jerk reaction if there happens to be a significant month-on-month percentage gain. It's meaningless but the market got all hot and bothered about housing starts, after all.

As a final note, be aware that Kansas City Fed President Hoenig is due to testify on monetary policy before Ron Paul's House Financial Services Committee at 2:00ET. Although the Fed Chairman has worked very hard to get Hoenig back on the reservation and reined in with the new communications policy, Congressman Paul is sure to try and elicit some hawkish comments at the hearing entitled "Impact of Monetary Policy on the Economy: a Regional Fed Perspective on Inflation, Unemployment and QE3."