Investors on Friday felt a bit betrayed, while the man on the street said "See? I told you so!" as the Bureau of Economic Analysis (BEA) reported revised figures for the last several years of GDP growth. The BEA revised the last three years (plus 2011Q1) in the regular series of revisions, and also made some lesser revisions back to 2003. These revisions show the 2008/09 recession to be deeper and the recovery less strong, and help explain the strange phenomenon of an economy growing without adding new jobs. It isn't that productivity was jumping; actually, the economy just wasn't growing as fast as we thought. In other words, the job growth makes more sense now.

The economy is smaller than we thought it was - and Q2 was weaker-than-expected as well. Headline GDP was +1.3% versus expectations for +1.8%, and Personal Consumption was only +0.1% (economists expected +0.8%).

Incidentally, the revisions have generally been to lower figures from the original releases to the final releases, as well. Counting from the original GDP release in each quarter, the new revised quarter-on-quarter growth rate ended up lower in 22 of the last 29 quarters, and higher in only 6. In other words, don't be too confident in the +1.3% that was announced for Q2!

Revising level of GDP lower, of course, raises the market-to-GDP ratio, and the ratio of profits to GDP, which is now at the highest level (biggest margins) in 60 years. The market, in other words, is even more over valued than it was on dependable long-term metrics like the Q ratio. (This doesn't mean that the next 100 Dow points is lower. The question I am more concerned with is what the next 5-10 years looks like. If I can be consistently right on that, I'll be consistently overweight when stocks are generally cheap and underweight when they are generally rich, and that ought to be good enough to do quite well over time. I feel the need to mention this because I think some people read this commentary as if I am writing about day trades. In general, I focus more on strategic positioning than tactical trading, although I try for a few good hit-and-run tactical trades per year).

Less-noticed was the Employment Cost Index, which rose +0.7% after +0.6% last quarter. This performance will worry some people who fret about wage-push inflation, even though the evidence that there is such an animal is sparse (wages typically follow inflation, rather than lead it). The ECI broke down as +0.4% on the wages portion (right on the trend of the last couple of years), but the +1.3% rise in benefits was the largest quarterly increase since 2005.

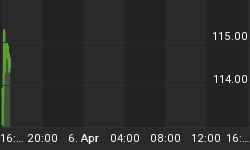

Noticed even less than ECI was the rise in M2 that printed on Thursday evening and put the 52-week rise in M2 at +7.9%. I had expected this rise to pause, flatten out a little bit, as the sudden acceleration is very unusual. But at least so far, there are few signs that this surge is a temporary phenomenon (see Chart). It also bears observing that since real GDP was revised lower, it implies that velocity slowed more than we thought as well (since MV=PQ, where M is the money stock, V is velocity, P is the price level, and Q is real output).

The multi-week acceleration in M2 is now noticeable even on a chart of the level of M2.

All of this news led stocks to open up weak, and bonds to continue their recent rally with 10-year yields falling to 2.80%. Equities rallied mid-morning when President Obama went on TV again to waggle his finger menacingly at the Congress. Soon, stock prices fell back and the S&P index ended the day -0.7%. As I said, bonds had a big rally, with yields falling 15bps on the 10y note. Real yields accounted for almost all of that, as the 10y TIPS yield fell 13bps to 0.36% - tying all-time lows from last October (see Chart). The reaction of real bonds implies that the bond rally is not due to a decline in inflation expectations, but rather to a decline in investors' expectations of the long-run growth rate of the economy. At least, that's philosophically the case; right now there are obviously a lot of other crosscurrents with the potential for the government to briefly stop spending money if a debt ceiling deal is not reached. Disappointment on Friday that a deal had notbeen reached also led the VIX index to reach its highest level since the Japanese tsunami.

10-year TIPS yields tie all-time lows.

Because the nominal bond rally occurred through the medium of real rates rather than inflation expectations, it seems that the rally was less due to flight-to-quality than it was a reaction to the GDP report and the revisions, which suggest that the resurgent economy was less resurgent than had been thought (and the return to monetary and fiscal policy even less than had been thought).

The reason that may matter is that, as I am writing this on Sunday night, there is talk that there may be an agreement to raise the debt ceiling that has been approved by Republican and Democratic leaders and by the White House. So far, it appears to be just the leadership that has agreed to the deal, but since both sides of the aisle have already had their cover vote (that is, they have each voted on the plan they wanted but that was doomed in the other chamber, so they can say to their constituents "I really tried") there is a decent chance that this gets approved and we can again spend like drunken sailors. Yayyy!

The deal only cuts spending by $1 trillion over the planning horizon from the previous baseline, which means a drop in the bucket compared not only to spending (which would be something like $40-50 trillion over the next 10 years, so this is a 2.0%-2.5% cut) but to the deficit itself. It would be a down-payment on another $1.5 trillion cut that Congress would need to decide on by year-end, or that would in the alternative happen through automatic cuts to all government areas.

If the deal is real, and is passed by Congress and signed by the President, then the stock market will breathe a sigh of relief. At this hour, S&P futures are up 15 points in Sunday evening trading. But it certainly isn't nearly enough to avert the downgrade that the ratings agencies have threatened, and fairly soon I imagine we will hear them say so. There was never a chance of default, unless the Administration had chosen petulantly to not pay the interest on the bonds with the trillions in revenue it continues to take in, and the deal doesn't seem to avert the downgrade, which was the real threat all along...so I suspect this is a sucker's rally in stocks.

Now, notwithstanding the foregoing I still don't think a downgrade is a big deal either. Indeed, since I wasn't worried about a default and I don't think a downgrade to the sovereign credit is a big deal, the main reason I have been watching the monkey business on Capitol Hill is because of my love for country and my fear for its future and the future of my children. Nothing I have seen recently makes me feel much better about that, except for the fact that the citizens themselves seem finally to be getting moved to action. And in the U.S., that's a mean feat.

Now, I did think of another negative possibility that could follow a US downgrade. A downgrade would also result in the downgrade of Fannie Mae (FNM) and Freddie Mac (FRE), which are under U.S. conservatorship and which only survive in their forms because of the extraordinary funding that U.S. backing affords. Without a AAA, it is much less clear that these entities will survive (although it has long been unclear whether they should survive). And that raises the specter of volatility in mortgage markets. It also might help explain the bid to Treasuries, because while there are few investors whose mandates will require them to sell sovereign bonds that are downgraded from AAA to AA, there are many more investors who hold agency securities who may have such mandates. Where does an investor who needs to sell Fannie Mae agency bonds turn to invest that money? Well, turning to the sovereign herself makes some sense.

In my current job I don't see those flows, as I might have if I was still on the sell side, but I wouldn't be surprised to hear that Asian accounts have been sellers of agencies for Treasuries.

.

One or two clean-up items from last week: on Thursday, Richmond Fed President Lacker said:

"The additional monetary stimulus initiated last November raised inflation and did little to improve real growth... Given current inflation trends, additional monetary stimulus at this juncture seems likely to raise inflation to undesirably high levels and do little to spur real growth."

I missed this when I wrote Thursday's comment but it is worth noting. So much for the new, tighter communications policy! This is just what I have argued for some time, but it is very surprising to see coming out of the mouth of someone in policy circles.

On Friday, St. Louis Fed President Bullard commented that the Fed's large balance sheet could cause an inflation concern if it isn't shrunk when it is time to shrink it. Hey, news here: see the M2 chart above. It's entirely possible that ship has already sailed! Bullard also said that the Fed is unlikely to add any more stimulus, because inflation is now rising. I've said this in the past as well. Last year, core inflation was declining, so the Fed's two mandates were not in conflict - adding more money helped avoid deflation and helped growth (well, anyway, that was their theory). That is no longer the case; the twin mandates are in opposition now so there is a much bigger hurdle for outright stimulus. Another bank crisis might do it, though.

.

The Wall Street Journal had an interesting story on Friday, entitled "Lending Markets Feeling the Strain." The story details how investors have been pulling lots of money out of money-market funds, supposedly because individuals are afraid of default on the government securities that are held in large quantities by those funds. This is the second explanation I've seen of the money leaving money funds, and this makes more sense than the "elimination of Reg Q" theory. In this case, we'll soon know if it's accurate because once a deal is reached and there is no default coming, the money should flow back in, right? But that isn't the reason I point this out. I want to make a different point.

Money flowing out of money funds affects the funding markets, but most individual investors never really see that dynamic. It isn't very important right now, anyway, since banks are dramatically over-funded thanks to the Fed. But moving money from money market accounts into transactional accounts - checking accounts, cash, brokerage accounts, etc - is a threat to inflation in assets or goods and services.

When transactional money increases, prices of goods tend to increase; asset markets, however, sometimes act as a 'relief valve' for inflationary pressures, which end up spawning bubbles rather than triggering inflation in goods and services. People who have extra cash, courtesy of the extra amount sloshing around in the system, can either spend that cash or invest it. If they invest it at increasing market valuations, it drains some of the inflationary pressure (I need to stipulate "increasing market valuations" in the argument, because obviously every dollar I spend buying equities is just transferred to the person selling me his shares) that would otherwise bid up goods.

But what happens when the markets start looking expensive and/or dangerous for everyone, across a great many asset classes? Then investors hold more cash - and that's exactly what they are doing. And that is fine as long as those cash balances sit there in those checking accounts or in cash. What happens, though, if investors fear those cash balances are going to be taken, either by government fiat or by inflation? Then the money gets spent instead, and moves from asset markets to goods markets.

We don't really know how this dynamic works. We don't know how fast money moves in these circumstances. We have never observed this sort of situation before, and we can't recreate it in the lab. I raise it as a point of curiosity, and a matter for discussion and debate, and as a warning. It is just another risk to watch, as if we didn't already have plenty of them. It is not today's trade.

.

On Monday, we'll react to the weekend edition of Deal-Or-No-Deal. The ISM will be released, and is expected to be approximately unchanged (Consensus: 55.0 from 55.3), but unless there is a real shock that will be largely ignored while investors watch the votes on Capitol Hill. Passage of a deal will mean an equity rally that many of us will look to sell into if we have a chance. Failure...well, let's not even think about that.