On Thursday and Friday I was in Chicago, doing business but also attending the first day of the American Economic Association annual conference. Accordingly, I have a few things I need to catch up on in this article - but first, I want to point out something I observed on the agenda for the AEA. This is a very large conference, with literally thousands of economists (and other hangers on, like me) in attendance. There are roughly 500 sessions of around 2 hours apiece, and most of them consist of four speakers or paper presentations. So, roughly, there are maybe 1700-1800 papers presented at the conference.

Do you know how many I was able to find that involved research relating to inflation? The answer is zero or one, depending on whether you count "Internet Prices in the Great Recession," which was a talk by the guys who developed the "Billion Prices Project" at MIT. What does that mean? I suspect it means that economists think inflation is a dead subject, with not much chance of becoming interesting, and/or they figure we already know everything we need to know about inflation. Neither could be more wrong, in my view.

There were still plenty of interesting sessions. One of the most-interesting and most-timely was a panel discussion by Peter Boone, Ken Singleton, and Carmen Reinhart (co-author of This Time Is Different: Eight Centuries of Financial Folly) that was entitled "Sovereign Default." Simon Johnson, from MIT, moderated this timely panel, and started off by asking the panelists if they thought there would be a sovereign default in Europe within 12-18 months. Reinhart said that Greece and Portugal would go, and with Spain and Italy "it depends on whether they are Too Big To Fail." She said, "it's not even math. It's arithmetic." Peter Boone observed that the real crisis is that bonds which were once treated as sacrosanct (such as Italian govvies, by Italian pension funds) are no longer sacrosanct. If they're not sacrosanct, they need a big risk premium. But if there's a big risk premium in the yield, the sovereign cannot survive.

Boone also predicted that "if the citizens of Europe decide they don't trust the Euro, it will all collapse in inflation" (following the ECB's large-scale purchase of bonds to save the market, which he said is really the only way out). He later pointed to Russia's breakup as a good analogy, because each republic had its own central bank with the ability to print money. When people lost confidence in the ruble, the country ended up in inflation. Indeed, it was striking that all three discussants saw inflation, not deflation, as the likely result of an outcome that involved a Euro breakup and/or default. I will have more to report on this session sometime over the next few days...there is a lot to chew on.

.

So what happened while we were discussing sovereign default? Europe produced its first shudders of the new year. At a 12-month treasury bill auction on Thursday, Hungary failed to raise what it needed, even though it was offering almost 10%. The country was downgraded to junk by Fitch. The EU/IMF pushed back the schedule for Greek disbursements a full three months as they continue to negotiate the second €130 tranche of aid. The €5bln it was supposed to receive in December will instead show up in March, and the €10bln it was supposed to receive in March is now due in June. This is somewhat problematic because Greece has some big redemptions in the first quarter. But the bigger fear is that politicians in Europe are playing a dangerous game in trying to get a leg up on the negotiations.

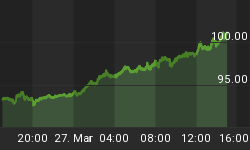

Sovereign debt markets have not responded well to the turning of the calendar. French 10-year yields reached the highest level since the spike in November. Italian yields are back up over 7% (see Chart, source Bloomberg).

Italy isn't getting lots worse, but it is clearly not getting better either.

Meanwhile, Euro deposits at the ECB reached an all-time record of €455bln. In a way, this is good in that it implies the ECB hasn't really been quantitative easing (yet) with its unprecedented provision of "unlimited" 3-year money. If the money is 'stashed' at the central bank, then what is happening in Europe is essentially what we saw in the U.S. with QE2 when the Fed paid banks to keep the extra liquidity in reserves. However, in this case banks explicitly borrowed at a higher rate for 3 years and then lent at a very low overnight rate. Why would a bank do this? Well, they might be just playing the yield curve, betting that rates will rise enough to turn a profit on the 3-year money, but I doubt that. They might be doing the equivalent trade, taking ECB money in lieu of raising overnight money that could be very expensive under conditions of stress; in that case, this exchange of 3-year money to overnight ECB deposits at a lower rate can be thought of as an insurance premium. Either way, the same issues apply to this transaction as applied to QE2: it is unclear how fast, or whether, this money leaks into the real economy; if it does, then the resulting inflation may be controlled or uncontrolled - and the ECB at that point will have nothing to do with it.

The key economic data point was the Employment Report, which was both better-than-expected and disappointing. It was better-than-expected in that the headline number was 200k, about 40k better-than-expected net of revisions, and the Unemployment Rate fell to 8.5% from a revised 8.7% last month. It was disappointing, though, because other jobs market data had given reason for optimism (not least, the 325k ADP number on Thursday, which I'd warned could suffer seasonal-adjustment issues). The participation rate is still at generational lows of 64.0%. And one of my favorite little-watched indicators, the number of people who are not considered in the labor force but nevertheless say they "want a job now," remains at extremely high levels and is showing no signs of improvement (see Chart, source Bureau of Labor Statistics). So, while the jobs market is improving, it is too early I think to proclaimed it healed.

The employment picture is improving, but not enough for these guys.

While equity prices held Tuesday's gains all the way through Friday, the volume story is beginning to get disturbing. Clearly, volumes weren't low because investors were waiting to see Employment. Friday's volume was actually the lowest of the week. It is very odd for an Employment day to be a low-volume day! The last time we saw NYSE composite volume above 1 billion shares, with the exception of triple-witching day on December 16th, was November 30th. Cumulative volume for the first four days of the year was 1 billion shares less than we saw during 2011's first four days, and for comparison it was 4 billion shares less than the first four days of 2006 or 2007. This is not a healthy market, even if it did rise 1.6% in the first week. Maybe this is just part of the wall of worry it will climb, but if the army is storming the enemy position it would be more comforting if it brought a few more soldiers.