Tuesday was another day of ho-hum trading following yee-haw news.

Anyone expecting a bloodbath following the ratings downgrades clearly has not been paying attention as the market sleepwalks through 2012. Stocks gained 0.4%, 10-year note yields ended virtually unchanged at 1.86%, and TIPS yields fell 2.5bps despite the proximity of a $15bln 10-year auction, now only 2 days away with 10-year TIPS yields at -0.22%.

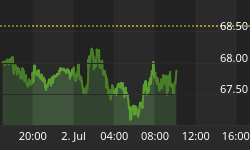

The dollar slid somewhat, and commodities rallied. Indeed, the only market with a reasonable level of excitement was the Nat Gas market, where prices fell to levels not seen since 2002 (see Chart, Source Bloomberg). It is useful to remember that a significant part of commodities futures returns comes not from movements in the spot price, but from collateral return, normal backwardation, expectational variance, and a couple of other sources.

Natural Gas front contract.

Spot gas has gone basically nowhere in a decade as supply responded to price.

Of course, Nat Gas also had the worst fundamentals of any commodity. Coming into the month, the mild winter and the added supply from frackers had combined to make NG the fourth-most-contango commodity (a commodity in contango is one which has deferred contracts at higher prices than nearby contracts, implying a negative roll return), with the worst momentum, among the universe of normal commodities. That combination means that it was not selected this month to be one of the commodities in the USCI basket. And that, in turn, means that USCI has appreciated by 3.79% this month while DJP, an ETN that tracks the DJ-UBS Commodity Index, is up only 0.02%.

European bonds closed mixed, with small gains in Greece, Portugal, Ireland, and Italy on the back of successful sales of short bills in Spain, Hungary, Belgium, and by the EFSF. But it isn't very surprising that these sales of 3-month to 18-month bills were well-received, considering that the ECB has made hundreds of billions of Euros available virtually free to banks, which can earn an easy spread in this way. Let me know when Spain sells a 5-year note. Portugal also bounced a little today because the huge move yesterday was caused by Citi removing the country from its European Bond Index after its downgrade. Some investors who systematically wait for these "forced" moves to take the opposite side of figured to be getting a mild bargain. For a little while, anyway!

Fitch tried to grab the headlines back from S&P by saying that Greece is insolvent and will default. Really, though, at this point it's about the over/under on when, not if, Greece defaults. Markets did not react to this news, nor to S&P's statement that it will take ratings actions on European banks and insurers within the next month, some as early as the next week. This is potentially a bigger deal than the original downgrade itself. While a sovereign rating is a strange beast - since many investors will treat the sovereign as the closest thing there is to a risk-free investment in a particular country, no matter what its rating - ratings of financial companies affect actual contracts, collateral covenants under a CSA (collateral support annex to an ISDA), and credit lines. It was a downgrade to AIG that triggered one of the big failures in 2008, when the additional margin demanded by CSA agreements could not be met by the firm. And the problem for investors is that unless you're the guy holding the CSA that has the rating trigger in it, you won't know about the problem until it's too late. Not that investors need any more reason to avoid financials than that their business model is irremediably destroyed and ROE will be permanently lower in the future, but the silent-but-violent nature of the blowup events means the only person holding the credit that is about to go under will be the person who is the last to hear about margin calls.

.

By now, I suppose we all recognize that one of the precipitating factors for this crisis, if not the precipitating factor, was the rise in leverage and in particular private leverage. There has been a lot of ink spent about the 'deleveraging' that is going on; as I have written several times before (most recently in "Scrooge Businesses") the data say this is largely a myth. Domestic financials are deleveraging; Households are deleveraging slightly; Businesses are now re-leveraging. And of course, this is all occurring with the backdrop of the great increase of leverage that the federal government is generously taking on our behalf. I think that many of us feel that society must be deleveraged broadly in order to build the foundation for robust future growth. I want to take a quick moment here to talk about the difficulty of actually reducing overall leverage.

John Mauldin recently wrote (and he has written many times before on this topic, as have others):

"...a country cannot reduce private-sector leverage, reduce public-sector leverage and deficits (balance its budget), and run a trade deficit all at the same time...ultimately, there must be a trade surplus if leverage and debt are to be reduced."

The statement is true from any given country's perspective; Mauldin's argument is that we can't all run trade surpluses. That's not quite true: emerging market countries are in general drastically less-leveraged than are the developed countries, so if we could just persuade them all to run large trade deficits to the developed world, we could shift our indebtedness to them. Let's assume for the sake of argument that isn't a serious alternative. What, if anything, do we need to do to reduce ALL debt and leverage?

It may seem easy. Each of us needs to save, pay down credit cards, and so on. We all know people who are doing this. And yet, the numbers say that in aggregate, it's not happening. That's because when Person A sells his house to person B, one is delevering but the other one is levering. When Person A defaults, he delevers but the bank who lent him the money increases its leverage. If Person A defaults and the government injects capital into the bank, then the government is taking on Person A's leverage.

What the numbers tell us (see the charts in 'Scrooge Businesses' referred to above) is that the government's increase in leverage is simply balancing out the decrease in the banks' leverage, and households and businesses are just trading around leverage and not doing much. Is there anything we can do, absent borrowing lots of money from EM?

It turns out that there is one thing we can do, and you may be able to guess what it is by the fact that it has been the last refuge of heavily-indebted governments for many generations. Leverage is, notionally, the dollar value of debt divided by the dollar value of assets. Back in the 1970s and 1980s, one reason that overall leverage wasn't growing too fast is that the real value of debt evaporated pretty quickly. That is, you paid off your mortgage with dollars that were worth a lot less than when you took out the mortgage, and the house was worth a lot more. This happened because the value of a mortgage is a fixed number of dollars. Inflation helped keep leverage in check by eroding those claims. As a society, we became used to this effect, and when inflation went away in the 1990s and 2000s, we continued to draw as much debt as we had been (and more) but when we went to pay it back, it was still a lot of money! Much more debt got rolled and refinanced, and the debt numbers climbed.

The solution to the debt/assets ratio is inflation, unfortunately. While many assets will not keep pace with inflation, some will. Below is a chart (Source: Enduring Investments) that I use in presentations in a different context - illustrating how a corporation's capital structure drifts (to non-optimal levels) over time if debt is nominal. But the chart has meaning in the context of this discussion. The curves show how rapidly your leverage decreases under different inflation assumptions, assuming that you start at 100% leveraged, your assets keep pace with inflation and your debt is nominal. So for example, if inflation is 1%, after 10 years your leverage is down to 78% or so; if inflation is 7%, then your leverage is down to 45%.

Inflation isn't all bad. If you're a debtor. And aren't we all?

Note that this has nothing to do with amortizing the loan. We are assuming no amortization here. So all you do is pay the interest, and in 10 years your leverage drops 150% more (55% instead of 22%, roughly) with 7% inflation.

So, do you still think the Fed is neutral on inflation? Do you still think the Committee really wants inflation pegged at 2%? At the very least, the FOMC wants inflation to be at the upper end of the band that allows it to retain its credibility. And, if push came to shove, I suspect they might allow an "oops" to happen if they thought a little more inflation might help delever society.

And it might. It just might.