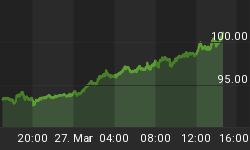

These days, the glimmerings of crisis are never far away, are they? Today, the sign was a very weak government bond auction in Spain, which caused 10-year Spanish yields (Portuguese and Italian as well) to rise about 25bps. Ten-year Spanish bonds now yield 5.69%, near the calendar year's highs although still considerably lower than the spike highs of last July and last November (see Chart).

However, during those prior episodes Spain was not merely reflecting its own fundamentals but those of its sick brethren. Compared to the German 10-year, the current spread around 400bps is just as high as it was in July of last year and only about 65-70s shy of the peak in November.

Meanwhile, in the last few days the German central bank and now the Austrian central bank have each declared that they will not accept Greek, Portuguese, or Irish bonds as collateral. Greece, remember, has been "saved" and the new bonds are supposed to be money-good; however, the yields on those bonds has risen since the exchange was made. The Feb-2023 maturity initially traded around 19% but has risen to 21.5%. If this is what healing feels like I'm sure glad we're no longer hurting!

In the U.S., General Electric was downgraded by Moody's to Aa3 from Aa2, and GE Capital downgraded to A1. Investors shrugged off this news, which GE claimed was due to a change in Moody's methodology rather than a change in GE's credit rating. That seems a risky claim, because the counterargument would be (assuming that Moody's isn't making their methodology worse) that GE (and more especially GECC) has been rated too highly in the past. GE stock declined in line with the broader market, although credit default swaps moved wider.

Equities dropped around 1%, largely from the news delineated above but also partially in follow-through to the "disappointment" that the Fed said exactly what they had been saying previously. However, bonds also rallied, and this wouldn't make much sense if the main impetus for today's movements was disappointment over the Fed's failure to provide support for the bond market. This is why I attribute most of today's movement to a renewed rise in the temperature of the European crisis.

Precious metals were killed, losing 4.2%, and commodities in general declined. For a change the move in commodities makes some sense, if you believe the tiny alteration of the Fed's direction in the minutes was significant, if you think the Fed is serious, and will pull back on liquidity rather than just fail to add more, if commodities weren't already very cheap, and if the easing of other global central banks was irrelevant. But if the decline was related to the Fed's tilt, then at least the commodity decline is the right direction, because the adjustment in the Fed-speak (if there was an adjustment) concerned cooling the degree of monetary support; prior recent declines in commodities have come due to growth fears that I don't think are particularly relevant right now to the outlook for commodities in the medium term.

.

I routinely deride economists who rely on the discredited notion that growth in excess of a nation's productive capacity is what causes inflation - and, conversely, a surplus of productive capacity is what causes deflation. See, for example, here, here, and here. And that is just in the last month!

I want to point out that it isn't that I don't believe in microeconomics (where an increase in supply causes prices to fall and a decrease in supply causes prices to rise). I believe deeply in the supply-demand construct.

But the problem with applying these ideas to the macroeconomy is that people get confused with real and nominal quantities, and they think of the "productive frontier" of an economy as being one thing rather than a multi-dimensional construct.

When an economy reaches "productive capacity," it isn't because it has used up all of its resources. It is because it has used up the scarcest resource. Theory says that what should happen isn't that all prices should rise, but that the price of the scarce resource should rise relative to the prices of other resources. For example, when labor is plentiful relative to capital, then what should happen is that real wages should stagnate while real margins increase - that is, because productivity is constrained by the scarce resource of capital, more of the economy's gains should accrue to capital. And so Marx was right, in this sort of circumstance: the "industrial reserve army of the unemployed" should indeed increase the share of the economic spoils that go to the kapitalists.

And that is exactly what is happening now. In the banking crisis, the nation's productive capacity declined because of a paucity of available capital, in particular because banks were forced to de-lever. Output declined, and after the shock adjustments the margins of corporate America rose sharply (which I recently illustrated here), near record levels from earlier in the decade of the 00s. And real wages stagnated. Be very clear on this point: it is real wages which are supposed to stagnate when labor is plentiful, not nominal wages.

Now, what should happen next in a free market system is that the real cost of capital should decline, or real wages should increase, or both, as labor is substituted for capital because of the shortage of capital. We indeed see that the real cost of capital is declining, because real rates are sharply negative out to 10 years and equities are trading at lusty multiples. But real wages are stagnating, going exactly nowhere over the last 36 months. Why is the adjustment only occurring on the capital side, with bull markets in bonds and stocks?

We can thank central bankers, and especially Dr. Bernanke and the Federal Reserve, for working assiduously to lower the cost of capital - also known as supporting the markets for capital. This has the effect, hopefully unintended, of lowering the level at which the convergence between real wages and the real cost of capital happens; and of course, it obviously also favors the existing owners of capital. By defending the owners of capital (and, among other things, refusing to let any of them go out of business), the Fed is actually helping to hold down real wages since there is no reason to substitute away from capital to labor!

But all of this happens in real space. One way that the real cost of capital and the real wage can stay low is to increase the price level, which is exactly what is happening. We call this inflation.

.

On the last full trading day of the week, Initial Claims (Consensus: 355k versus 359k last) represents our final chance to try and trade the Employment number before the actual number is released. ADP was right on target today, giving no clues about which way traders should lean going into Friday. I expect this means that traders will spend the afternoon trimming positions that they would be ill able to cover on Friday if there was a surprise on the Employment number. That probably means more weakness on stocks and possibly some further strength in bonds.