After a shocking upset in Greece's parliamentary elections, the US dollar surged dramatically. Soaring 5.4% in May alone, the world's reserve currency won legions of fans among traders. "King Dollar" was universally lauded, with everyone jumping on the strong-dollar bandwagon. But this dazzling strength was merely a short-term phenomenon. Zoom out a little, and today's "strong dollar" is a fallacy.

Perspective is everything in the markets. Attaining it is challenging and takes a lot of effort, but the fruits are well worth the toil. We humans naturally tend to extrapolate the present and very recent past out into infinity, expecting short-term situations to continue indefinitely. So when prices surge rapidly like the US dollar has, traders get greedy and assume the move will persist for a long time to come.

But greed, and its antithesis fear after prices have fallen sharply, are the mortal enemies of successful investment and speculation. Having perspective, keeping recent price moves firmly rooted in longer-term context, combats these dangerous emotions. While the dollar's advance over the past month alone was amazing, how does it look in the context of recent years' action? Truly not very impressive at all.

As always, the benchmark of choice for tracking the dollar's fortunes is the venerable US Dollar Index (USDX). Born many decades ago in 1973, it measures the progress of the dollar against a basket of a half-dozen major foreign currencies. Dominating these is the euro, at 57.6% of this index's weight. Next are the Japanese yen, British pound, and Canadian dollar at 13.6%, 11.9%, and 9.1% respectively.

It is this heavy euro weighting that has helped fuel the strong-dollar fallacy. Before the euro was launched in 1999, the USDX had ten components with no one commanding a dominant weighting. But when the euro replaced the German mark, French franc, Italian lira, Dutch guilder, and Belgian franc, there was no choice but to change each of these USDX components to the euro.

So the past decade's euro-centric USDX is an accident of fate. In the early 1970s Europe was the US's major trading partner, today's massive Asian economies had barely even started rising to prominence. Thus the most popular metric traders use to measure the dollar is effectively largely its exchange rate versus the euro. And man, fears of the 17-nation eurozone fracturing have been ubiquitous recently.

Every time something bad happens in Europe, which is pretty much every few days lately, the euro takes a hit as scared traders exit the world's second-most-important currency. And when the euro falls, naturally the euro-dominated USDX has to rise. May's incredible spike in the dollar was actually a precipitous plunge in the euro. The dollar wasn't loved, it was merely the lesser of two fiat-paper evils.

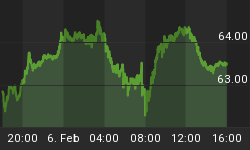

If you look at the past month's USDX chart, the dollar certainly looks like a rock star. But zoom out to gain that critical perspective, and things aren't so rosy. This first chart extends back to 2008, before that year's epic stock panic. And by these recent years' standards, the dollar not only isn't particularly high but its May rally wasn't particularly impressive. The so-called strong dollar really isn't so strong after all.

While traders have largely forgotten now, the USDX was suffering in a massive secular bear between mid-2001 and early 2008. I'll discuss that secular perspective a little later. But the net result of years' worth of dollar supply growth (inflation) outpacing world demand growth had forced the USDX to all-time lows by April 2008. The thriving young euro was the market darling while the dollar was a laughingstock!

But soon after, that year's once-in-a-century stock panic came along and changed everything. With the flagship S&P 500 stock index plummeting a nauseating 30.0% in a single month, everyone panicked and rushed for the exits. But traders around the world had to park this flight capital somewhere, so they collectively chose the US dollar and US Treasuries. This epic demand for cash was unprecedented.

It catapulted the USDX from just above its all-time lows to 22.6% higher in just 4.2 months, its biggest and fastest rally ever over such a short span! But it's critical to remember that this dollar buying wasn't because traders were excited about the dollar's fundamentals. They simply had nowhere else to hide. The very day the stock markets finally bottomed, the USDX peaked before reversing sharply.

To understand the dollar action today, you really need to see how the stock markets and US dollar interacted during and immediately after that panic. They moved in lockstep opposition, nearly a perfect negative correlation. This inverse link burrowed itself so deeply in traders' minds that ever since they have equated a rising dollar with falling stock markets and vice versa.

May 2012's sharp dollar surge was mostly driven by the old Europe fears of Greece leaving the euro. After a radical-left anti-bailout party nearly won Greece's early-May parliamentary elections, this suddenly became a very real possibility. But we can't discount the fact that the US stock markets were also exceptionally weak in May, weathering a sharp pullback. This also contributed to the dollar's spike.

After the stock panic, the dollar topped in March 2009 the very day the stock markets bottomed. Then it sold off sharply as the stock markets surged in a dramatic post-panic recovery. Early in this move, the USDX plummeted 2.9% in its largest down day ever when the Fed announced quantitative easing. This is a happy euphemism for monetizing debt, or creating new dollars out of thin air to buy Treasuries.

By late 2009 this currency was simply oversold, so a normal bear-market rally was due. But just as that healthy countertrend move was getting toppy, the first serious Greece fears emerged. To join the EU, countries had to agree by treaty to keep their budget deficits under 3% of GDP. Greece was reporting 6%, already a big problem. But the Greek politicians had been outright lying, in reality it was nearly 13%!

So traders started to get nervous about the euro, pushing the already-mature bear rally in the dollar higher. Soon after these fears exploded, Europe approved a massive €110b bailout package in May 2010. Couple this with a major stock-market correction, and the USDX rocketed back up to panic highs. But just like during the panic, as soon as the stock markets bottomed flight capital left the dollar so it quickly collapsed.

Interestingly the dollar surged again in late 2010 when the Fed's second round of quantitative easing was announced. This is counterintuitive, as more inflation is very bearish for any currency. But a couple factors came into play. First, QE2 was only about half the size of QE1 ($900b versus $1750b), so traders were relieved the new inflation wasn't worse. Second, the record Democrat losses in the US elections (the day before QE2 was announced) led to hopes Obama's insane overspending would finally be reined in.

But that hope was short-lived, by spring 2011 the USDX was once again nearing all-time lows. This dollar weakness persisted for the better part of two quarters, until last autumn. If the US dollar is such a great currency as its bulls proclaim today, then why couldn't it catch a bid without Europe scares or stock-market selloffs to drive temporary safe-haven demand? Those conditions are the only times the dollar has rallied meaningfully since the stock panic!

Late last summer the Greek fears began to flare again as rumors swirled that its initial bailout wouldn't be enough, that the Greek politicians (like Obama) refused to quit spending vastly more than they were taking in. So the dollar rallied briefly. Then later in November and December it surged again on a European sovereign-debt scare. Yields in troubled European countries far larger and more important than Greece were being driven up towards dangerous 7% levels as investors fled.

But like every other Europe scare in the past few years, that one too soon passed. So the resulting euro selling climaxed in mid-January, leading the USDX to peak at the same time. But that interim high was still pretty low by post-panic standards. This benchmark US dollar index remained way below its panic peak, roughly halfway up into its entire post-panic trading range. The strong dollar was merely a short-term illusion.

And then it started drifting sideways to lower again in 2012, even when the Europeans capitulated and agreed to a second massive Greece bailout of €130b. Still the dollar didn't go anywhere for a couple more months until early May, when recession-weary Greeks voted big for an extreme anti-bailout party. Exacerbating this was the sharp pullback in the stock markets, driving serious safe-haven demand.

While May's spike was certainly impressive in isolation, it was truly no big deal within this longer-term context. Not only was the USDX not very high in its post-panic trading range, its spike was much more anemic than what we've seen since 2008. Between its mid-January and late-May interim highs, the best the USDX could muster was merely a 2.0% gain. This is nothing to write home about over a 4.5-month span.

Think about this a second. While Greece fears festered in the background since early 2010, it wasn't until the past few months the odds of Greece leaving the eurozone mushroomed from remote to possible or even probable. The fears of Europe (and maybe the euro) fracturing have never been more intense than in the last few months, especially in May after that Greek vote. You couldn't ask for a better psychological backdrop for the US dollar, with its only real competition seemingly doomed.

Yet what did it do? Not a whole heck of a lot! It remained far below its panic highs and not much above where the recent European sovereign-debt scare took it. If the strong-dollar crowd was right, if the dollar's fundamentals were really bullish, the USDX should have been trading well into the 90s by now instead of the low 80s. The dollar's recent strength is merely a temporary flight-capital phenomenon, not a bullish breakout.

A couple weeks ago I wrote about the embattled euro, which has been driven to deeply oversold levels by all these Greece fears. It is due to surge, as it is one of the most popular and overcrowded shorts in the world. When the euro inevitably reverses, the USDX is going to get crushed. And if the dollar couldn't forge new post-panic highs with euro-fracturing fears climaxing, when will it ever be able to?

This next chart zooms out one more time, to the US dollar's secular bear. While today's strong-dollar thesis is wrong even from the post-panic perspective, it is a total joke from a secular perspective. Despite huge spikes on periodic flight-capital demand, the world's reserve currency continues to languish way down near the bottom of its secular trading range. Calling this "strength" is absurd, it is a total fallacy.

Thanks to the Fed's endless creation of new paper dollars at rates far exceeding global demand, the US dollar has been crushed over the past decade or so. Just before the stock panic in early 2008, the USDX had fallen 41.0% lower in just under 7 years! Typically when secular bears end, strong bull markets begin. But for the 4 years since, the dollar has only been able to rally periodically on safe-haven buying.

As soon as whatever happens to be scaring traders into hiding out in cash inevitably passes, so does any dollar buying. The net result is despite some awesome bear-market rallies in recent years, the dollar has simply drifted sideways not far above secular lows. The area of the first chart is shaded in blue here, and seen within secular context this post-panic action looks even poorer since the USDX remains so low.

After having to deal with all the market fallout in recent years from Europe refusing to live within its means, like the majority of traders I am tired of Europe. Some days I curse the whole idea of a united Europe and its single currency. But despite this universal Europe fear, Europe fatigue, Europe contempt, the best the USDX could manage was a meager 13.9% rally over 13.1 months. This isn't particularly large even by its own secular-bear standards.

If the dollar can't catch a meaningful bid on a secular scale even with this dire euro backdrop, it is probably going to get slaughtered when this latest round of Europe fears passes and the euro reverses. It is really amazing, and ominous, to see the dollar still drifting low in its secular range with countless traders extremely worried about the end of the euro as we know it. The strong dollar is a fallacy.

Why is the dollar so weak despite having everything going for it psychologically? Probably because of the Fed's endless monetary inflation, which has accelerated to double-digit rates in recent years. The price of the dollar in world markets, like everything else, is determined by supply and demand. The Fed is ramping dollar supplies like crazy, like there is no tomorrow. Yet at the same time global demand is slowing.

Investors around the world, including central banks, are increasingly disgusted with Washington's gross mismanagement of its currency, government spending, and debt levels. This whole Greece mess started because its politicians ran 13%-of-GDP deficits to finance extravagant social programs to bribe voters. In recent years Obama has been recklessly running US deficits in the 8% to 10% range! The US is a mess.

In addition, central banks around the world are still radically overinvested in US dollars even after the ravages of its long secular bear. They need diversification, and buying the euro is the way to get it. There is also a revolt among countries, companies, and investors over the increasingly draconian and heavy-handed controls and regulations on currency movements and banking coming from Washington.

As long as the dollar's supply growth exceeds its demand growth, it is going to remain mired deep in its long secular bear. And as sad as it makes me as an American, I can't see this changing anytime soon. Washington will keep spending like the Greeks, far beyond its means. The Fed will keep printing new money to buy up the resulting debt. And the world's respect for the US dollar will continue to wane.

The strong-dollar fallacy has hit one asset class particularly hard, commodities. Futures traders are quick to sell on any dollar strength, so commodities have just been trashed. They even decoupled from the stock markets' latest upleg, which is unprecedented. They and the stocks of their producers are trading at incredibly oversold levels, so they will be the primary beneficiaries of the US dollar's next slide lower.

And of course no commodity is more responsive to the US dollar's fortunes than gold. The sharp dollar surge in May drove a full-blown capitulation in gold stocks and to a lesser extent in the metal itself. Capital is already returning after that rare selling-exhaustion event, laying the groundwork for a major new upleg. So when the euro starts recovering from irrational fears and weighs on the dollar, gold and its miners ought to soar.

At Zeal we've been watching the dollar to help time our commodities-stock trading for over a decade now. I called this dollar secular bear way back in August 2001, when it was a hardcore contrarian position. Over the years since we've bought commodities stocks cheap when the dollar was higher, watched them rally as the dollar slid, and then sold them high when the dollar was lower. It has been very profitable.

Recently we've been buying back into cheap gold stocks, because their potential is so great. You can see our trades, analysis, and outlook in our famed weekly and monthly newsletters. In them I draw on our vast experience, knowledge, wisdom, and ongoing research to explain what the markets are doing, why, where they are likely heading, and how to trade them with specific stock trades as opportunities arise. Subscribe today and prepare to ride the coming dollar reversal!

The bottom line is contrary to popular belief the US dollar really isn't strong today. Despite a perfect backdrop of extreme Europe pessimism, the USDX remains low in post-panic terms and very low from a secular perspective. May was a great month, no doubt. But within the context of longer-term trends crucial for short-circuiting dangerous greed and fear, the US dollar's recent strength is minor at best.

Couple this with an oversold euro battered down to its major post-panic support, and a sharp dollar reversal lower is likely imminent. Given the endless bearish newsflow out of Europe, sooner or later something positive will happen. Like Greeks voting to stay in the euro next week. Whatever the euro-buying catalyst is, it will crush all the new dollar longs and light a fire under oversold commodities.