The market is sapping the strength of investors. Monday's short-lived euphoria following the weekend bailout for Spanish banks will cause many bulls to understandably lose focus. Similarly, the bears were able to breathe a sigh of relief following a Monday morning scare in the futures market.

This is not the time for the bears to become complacent or the bulls to become disinterested. If the S&P 500 revisits the recent low near 1,266, we believe it will possibly spark one of two binary outcomes:

- A sharp, possibly bailout/central bank-induced rally, or

- Entry into a full-blown bear market with significantly lower prices

Numerous factors, including trendlines, Fibonacci retracement levels, and DeMark exhaustion counts, point to the 1,248 to 1,278 range as being very significant relative to investment outcomes over the next three-to-six months. It is prudent to have both "sharp reversal" and "waterfall decline" contingency plans polished and ready to go.

There is no question we are in a deflationary period for asset prices. The ratio of U.S. Treasuries (TLT) to gold (GLD) clearly shows a shift from inflationary expectations to deflationary expectations. The market currently believes the mountains of debt round the globe cannot be overcome by the central bankers' printing presses.

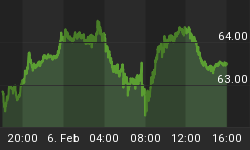

We noted Monday morning that despite the rosy tone in the pre-market S&P 500 futures, bond investors were beginning to grasp you cannot solve a debt crisis by continually issuing more debt and handing out bailout loans. The chart below shows the yield on a Spanish ten-year bond. Yields rise when demand for Spanish bonds falls.

The charts above tell us unless the market sees some type of significant move from European policymakers or another round of money printing from either the European Central Bank (ECB) or Fed, the stock market is going lower. The situation is understood by a handful of policymakers, most notably within the central banks. Thus, we should expect another bailout or form of market intervention with the next two weeks.

The chart below shows simple support and resistance areas that may impact stock prices in the coming weeks. The S&P 500 has pockets of potential support near 1,270 and 1,250. If stocks cannot find support from buyers near 1,250, a relatively rapid move below 1,200 could be in the cards. We plan to show some patience above 1,250; below that level, a more defensive posture will be warranted.

The chart that follows looks complex, but the concepts are simple. The thin horizontal blue lines highlight Fibonacci retracement levels based on the bullish move from the October 2011 low to the April 2012 high. From an investor's perspective, these levels represent areas of possible support. The chart below is based on intraday highs and lows. The levels to watch are 1,289, 1,248, and 1,207. If you use closing prices, the levels are 1,296, 1,259, and 1,221.

Demark indicators are based on market exhaustion, where the last group of sellers finally throws in the towel. You can understand from a psychological standpoint how investors could be ready to give up after European policymakers' latest band-aid "solution" was followed by additional bleeding in the Spanish and Italian bond markets. To hit exhaustion counts in Demark speak, the S&P 500 would have to move back below 1,278. DeMark counts are covered at the 1:02 mark in this June 10 video. DeMark indicators are proprietary tools from Market Studies, LLC.

Bond yields are possibly foreshadowing another round of market intervention from central banks. Support, retracements, and DeMark counts all point to the range between 1,248 and 1,278 as being important for the longer-term bullish case.

While keeping a watchful eye on central banks, we will continue to monitor the markets and developments in Europe. We remain open to "buying low", but also respect the bearish case that could produce significantly lower deflationary lows in stocks.