Today's market selloff owes much to the people who put together the ADP figures (that is, Macroeconomic Advisers). Yesterday's cheerful ADP report raised expectations for today's Employment report. Unfortunately, those expectations were dashed. The U.S. economy generated 80,000 new jobs in June, which wasn't far statistically speaking from the Bloomberg consensus of 100,000 but was far from what investors were hoping for. The economy has now expanded payrolls at the blistering pace of 75k per month over the last three months. Wow!

The Unemployment Rate nudged slightly higher to 8.217%, although unchanged on a rounded basis.

It wasn't a horrible report, just horrible compared to what investors were expecting. The stock market judged the labor market progress harshly, with the S&P losing -0.94% although it was down more than that for most of the day. It didn't help that European markets were getting smacked again, with Spanish 10-year yields +53bps and Italian 10-year yields +25bps. It was revealed today that another of the key summit concessions, the fact that the ESM would lend directly to banks rather than to the Spanish government which would then lend on to banks, won't actually happen in practice. First of all, the Troika report which was to precede the signing of the memorandum of understanding wasn't ready on time (because you know, they probably have more-pressing problems than the €100bln hole in Spanish banks). Second of all, the ESM isn't ready yet, so any money going to banks will have to pass through the sovereign and that messes up the whole works. Moreover, a senior EU official reportedly said today that the mechanism of having the ESM lend to the banks was only to "cut out the effect of that loan on the debt-to-GDP ratio of the sovereign...It remains the risk of the sovereign." So, again, financial legerdemain over substance.

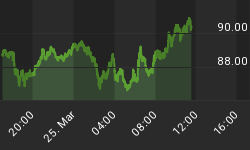

Moreover, if the Spanish banks can't or won't buy Spanish bonds, and the ECB won't buy any more Spanish bonds, who is going to buy the Spanish bonds? Apparently, this is something of a question or 10-year yields wouldn't be back near the crisis highs (see Chart, source Bloomberg).

Commodities finally reacted to the weak turn in the growth story, and the further rise in the dollar, by declining today. The energy sector, let by Nat Gas, fell 3.1% (Natty was -5.4%). The DJ-UBS index was -2.3% (although our preferred commodity index vehicle, USCI was only -1.2%). U.S. bonds rallied, with 10-year real yields -2bps and 10-year nominal yields -5bps. Ten-year inflation expectations as reflected in US CPI swaps fell to 2.39%, the lowest since January although well above the lows of last year.

In the jobs report, Average Hourly Earnings provided an upside surprise, with the year-on-year rate of earnings increase rising to 2.0%. As I've said in the past, though, wages follow inflation so this isn't particularly important to the inflation outlook. Potentially more-significant is the fact that M2 money supply growth on a year-on-year basis fell yesterday (largely from base effects) to +8.0%. While that's still quite high (if we had real growth of 2.5% and velocity was stable, it would imply inflation of 5.5%), it is the lowest it has been in almost one year. Further base effects could bring M2 down to the 6-7% range over the next couple of months, which is still too high for comfort but which will help Chairman Bernanke build the internal coalition for additional easing as some of the traditional monetarists conclude they can stop worrying about the money supply. In the next few weeks, M2 will surpass the $10 trillion mark, but this is likely to go unremarked and unlamented. Today's Payrolls report, along with the ebbing M2 growth and continued malaise in Europe, raises significantly the likelihood of near-term Federal Reserve quantitative easing.