The following is part of Pivotal Events that was published for our subscribers July 19, 2012.

SIGNS OF THE TIMES

"China's benchmark price for power-station coal fell for the ninth week, the longest period of losses since 2008."

~ Bloomberg, June 10

"America's Coming Civil War: Makers Vs. Takers"

~ The Washington Times, July 12

We have been writing about America's second civil war for some years, and note that it has been a "cold" war. The main difference is that the original Civil War was fought to extend freedom; the Cold Civil War has been prosecuted to constrain freedom through the urgencies of political correctness. Political correctness has been a remarkably versatile instrument.

"Makers Vs. Takers" is a very good slogan.

"The figures that go into China's gross domestic product are 'man-made' and 'for reference only'."

~ Bloomberg, July 13

The criticism was made by Li Kegiang who was a regional Communist Party head in 2007. It was revealed by WikiLeaks in 2010.

It seems that most countries have a Ministry of Truth.

Perspective

On Friday the Dollar Index stalled out at the overhead resistance level of 83.5, and has slipped to 82.8. This has refreshed stocks, corporate bonds and commodities. Or, perhaps it's the other way around as strength in the orthodox trio has forced the dollar down.

Friday's ChartWorks noted that the DX was poised for a pause in its long-term uptrend.

Positive vibes could run for a few weeks.

Bonds, Bonds, Bonds

Intended consequences often become unintended consequences - particularly when it comes to intrusive policymaking. One might ask if there is any other kind. Fiduciary responsibility hasn't been seen or heard of since the late 1900s, which recorded the height of Nineteenth Century Liberalism. One consequence is a highly speculative bond market.

The purpose of the initial stimulus with the Bear Stearns problem that began in June 2007 was to fix one problem and restore the "prosperity" of the boom. Mind, there was a faction that was working to keep the "sup-prime" problem "contained". Neither worked out because the feature of every great financial mania has been that most banks get reckless and overexposed at the same time. So "fixing" one bank was improbable, as was the notion about "containing" the sub-prime-housing disaster.

But, the combination of naivety and ambition propelled policymakers to ridiculous attempts to make bad things go away by hoping a new wave of speculators would start to bid up house prices. But the stimulus had to go through the banks, which means Wall Street, and savvy traders (the ones left) positioned for a technical rebound. This turned into the first business recovery out of a crash. It was likely to be weak.

But the action became outstanding enough to set up the next wave of losers.

Essentially, this began with commodities when our Momentum Peak Forecaster called for a speculative surge to complete around March 2011. The high for the CRB, which was likely to be a cyclical high, was 370 at the end of that April. Technically, the CRB and within this, base metals are in a bear market. Grains have been outstanding lately due to the worst heat and drought in decades.

The next big play to culminate was the compelling action in US Treasuries. This registered huge Upside Exhaustions in May, as Ross described the chart as an "Eiffel Tower". The peak of intense speculation is being tested and, technically, a significant price-decline is possible.

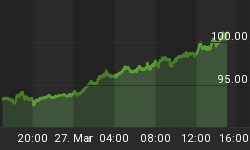

With senior government bonds declining to exceptionally low, or even negative, yields, the action turned to corporates and has become measurably compulsive. The following chart shows a set of daily Upside Exhaustions that usually anticipate an approaching top within a couple of weeks. Also noteworthy is that the index is reaching for the upper channel trend line at 122.

Technically, an impressive price drop is possible.

What would be the fundamentals of such a decline in price and rise in yields?

In as few words as possible the reasoning is Post-Bubble Contraction. During any financial mania the world compulsively takes on more debt than the global economy can service. That's even if the economy remained "normal", but the pattern has been that the worst recession since the last bubble occurs. This has been followed by an unusually weak business cycle.

The only way out of the condition is a lengthy process of liquidation of all debt. "All"?

Yes, because the process can be called a great bond revulsion whereby all classes of bonds are shunned or avoided. Outstanding speculation in long-dated treasuries in May and in investment-grade corporates now suggests the best is virtually in. A turn for the worse could live up to the full meaning of the word.

Much is being written about negative yields. This is an exceptional condition, but negative real rates adjusted for inflation are part of any great bubble. We will review this more thoroughly, but for this week's piece we will note that real long interest rates in the senior currency have increased by some 12 percentage points during the great bond revulsions.

Raptured Corporate Bonds

- Typically, the Upside Exhaustions anticipate the actual top by up to a couple of weeks.

- The action is approaching the top channel line at around 122.

- Note the technical "buys".

Link to July 20, 2012 "Bob and Phil Show"on TalkDigitalNetwork.com: http://talkdigitalnetwork.com/2012/07/corn-pops-markets-slump/