Quite contrary to my expectations, not to mention those of a majority of investors and analysts, I think, Ben Bernanke's Federal Reserve confronted the recent weak economic data and delivered almost exactly nothing.

The Fed didn't even extend the "at least through" language. Changing "at least through late 2014" to "at least through mid-2015" was probably the smallest token gesture the Committee could have made. The language, originally perceived to be a 'promise,' has become a bit of a joke since the projections by members of the FOMC indicate that many of them don't take the promise as representing any kind of commitment, merely a projection that they don't all agree with. As such, it has zero policy value since buying 2-year notes on the basis of what the pointy heads suggest they think will be their policy a year from now would be just plain stupid. And yet, the Fed didn't even incline its head with a small nod in this direction.

Wall Street Journal columnist Jon Hilsenrath must feel used. His column last week suggested strongly that Fed officials "find the current state of the economy unacceptable" and that they "appear increasingly inclined to move unless they see evidence soon that activity is picking up on its own." Wall Street assumed that Hilsenrath wasn't engaging in unsubstantiated guesswork about policy, but that the suggestion was being run up the flagpole.

Guess not.

There is certainly no evidence yet that "activity is picking up on its own." The ISM Manufacturing Index remained just barely on the shady side of 50.0, when a bounce was expected; this included a drop in the "Employment" subindex to the lowest level since the end of 2009 (see Chart below, source Bloomberg). The data will keep on coming, of course, but so far there haven't been any signs of imminent dawn. Indeed, the Fed continues to see "significant downside risks" in the global economy.

I admit that I thought they would do something more than merely change the non-binding promise language, and I was surprised they did not. I thought they would cut the Interest on Excess Reserves (IOER) rate back to zero. That doesn't mean, however, that I thought cutting IOER is the right thing to do. Monetary policy here is impotent with respect to growth, and while they can push inflation higher or lower with policy the move they should make is probably to start pulling back on liquidity once Europe is clear of danger. They should not wait until money velocity begins to rise again.

But that isn't what they will do. The Fed doesn't believe that it is impotent with respect to the Unemployment Rate, so even though they are firing blanks at a charging enemy with no apparent effect, I fully expect them to keep on firing. It's odd, as an analyst, to try and get into the "Fed's brain" and think intentionally wrong, but I suppose it's what actors and actresses do when they're getting into character. It's just that my liberal arts education didn't include a thespian turn.

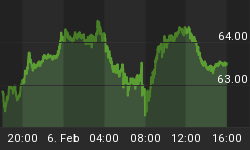

If I am in character as the Fed chairman, I'd be thinking it's awfully dangerous to wait before firing my next blank bullet. Gasoline prices are back on the rise, with retail unleaded back above $3.50 (see Chart, source Bloomberg), joining agricultural produce. This means headline inflation, which currently appears tame, is unlikely to stay that way for very long. If the Fed wants to ease policy in late September, they may have to do it with less-accommodating price data.

It is possible that the Chairman is afraid to do anything unusual, like cutting IOER, unless he has a presser scheduled so that he can explain it to us poor benighted folk? This could be the case, but it doesn't explain why they didn't do anything.

Could it be that, with the ECB meeting tomorrow and that body very likely to ease more aggressively than the Fed anyway, that the Fed chief wanted to let Draghi 'hold serve'? This seems strange, but it's plausible.

In any event, investors seem to believe there is another monetary policy shoe to drop. While yields backed up slightly with 10-year yields +5bps (1.52%) and stocks dropped a trifle (S&P -0.3%), commodities actually rallied after the Fed announcement! Almost certainly, the market will get something from the ECB tomorrow, but I suspect stocks and bonds are clinging too desperately to that eventuality and I expect any rally on the news will be short-lived.