The Olympics are over, so the political games begin in earnest. Over the weekend, presumptive Republican Presidential nominee Mitt Romney made his first revealing executive decision when he tapped Wisconsin Congressman Paul Ryan to be his running mate.

The selection changes the contours of the U.S. political race, as veep selections often do. It probably does not create any near-term consequences for the markets, but as and if the Romney/Ryan ticket gains in the polling (as they surely will; for starters, announcing a VP pick almost always produces a bounce but also this tends to energize the base that Romney absolutely needs good turnout from to win) it is likely to be beneficial to equity markets at the margin. The improvement, if it happens, will not be uniform. Some industries, such as autos, which benefit from direct government largesse will probably do worse; but the notion that smaller government may be in train with somewhat greater probability is likely to have positive impact on perceived long-term values. And any possibility that a fiscal conservative (that is, Ryan, not Romney) might be a senior member of the executive branch is likely to have salutatory effects, all else equal, on U.S. Treasury credit as well.

More than likely, these effects will be mere ripples in a much more turbulent pond. In an ordinary Presidential election cycle, markets and market sectors can ebb and flow with the fortunes of the incumbent and challenger; this cycle though is anything but ordinary. European events can, and most likely will, dominate the macroeconomic picture as well as global risk appetites and foreign exchange swings. Which is to say: you can cheer for whoever you want in this election, without worrying whether it will help your investments!

While most of Europe remains on holiday (and more and more Americans seem to want to emulate that behavior), market action remains excruciatingly slow. At 3:15 ET today, New York exchange volume was only 275 million shares and even the usual surge into the close only brought the total to 450 million. In a year of slow days, this was slower than slow. In fact, I was only able to find one session (other than half-sessions around Christmas or Thanksgiving) in the last ten years or so that had a lower volume number: the Monday after Christmas in 2010!

This lack of liquidity, with the stock market so near to setting new (nominal) highs for the year, creates instability even as it appears to suggest stability. As I argued last week, when liquidity is low there is a larger cost to initiating any move - but any move that happens is likely to be bigger.

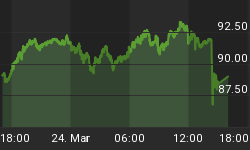

Add to that the fact that many investors have turned to covered-call writing to earn "extra income." Admittedly, I only have this anecdotally, as I was approached at a backyard party recently by someone who was writing naked puts (actually, they were writing covered calls, but because of put-call parity we know that that is exactly the same as writing naked puts with the same strike) and seemed to not understand my question about whether implied volatility was high enough to make that worth the risk.¹ Which, since the VIX is at its lowest level since early 2007, it's probably not (see Chart, source Bloomberg).

If this anecdote generalizes, and there is widespread selling of options, then it takes a dangerously-illiquid situation and makes it even less stable. With lots of gamma outstanding, what tends to happen is that small moves become microscopic moves since long-gamma hedgers try to recapture their time decay (selling rallies and buying selloffs), but large moves become really large moves because short-gamma investors try to save themselves from blowing up (buying into a market rally that they're missing, or selling stocks that are abruptly plunging, overwhelming their small 'income' advantage). I would be a much better buyer of options here, even in the middle of boring August.

Now, although markets are currently quiet, and government committees and the like are less-active as well (and in the U.S., elected officials are heading out to politick for the next few months), it doesn't mean that there's a complete lack of action. Indeed, with Dodd-Frank now steamrolling towards implementation, there are pockets of frenzied activity! One story that I saw today (which has nothing to do with Dodd-Frank) is interesting to investors since it lowers the hurdle for eliminating the payment of Interest of Excess Reserves (IOER). The title of the P&I Online story was "Money fund firms prepping in case SEC breaks the buck," and it described how the SEC plans to vote on August 29th on whether to issue a formal proposal requiring the sponsors of money market funds to either create a 'capital buffer' (perhaps similar to what the NY Fed recently proposed, and I mentioned here) or adopt a floating NAV policy rather than guaranteeing a $1 price.

We've discussed both of these proposals before in this space, but for today the significance is that if the floating NAV policy is generally adopted by money funds, the argument that a zero IOER could destroy money funds goes away. Since this is very likely to happen soon, either alone or as part of a parcel of monetary policy maneuvers, it is not insignificant that the SEC is pressing this issue.

.

Tomorrow the scheduled economic data includes Retail Sales (Consensus: +0.3%/+0.4% ex-auto). Core retail sales have been negative for the past three months in succession, something we hadn't seen since mid-2010. Four in a row would make the streak the longest since 2008, and I think it would be taken quite negatively by the markets. A positive print by Retail Sales isn't terribly significant by itself, since the series is quite volatile, but may be enough - even though expected - to continue to push the bond market lower.

¹ Note: if you do not understand and/or are not intimately comfortable with the definitional equivalence between a covered call and a naked put, then I will put my "friendly advice" hat on and beseech you, for your own good, not to sell options until you do!