The good news is:

• NASDAQ breadth data was stronger than NYSE breadth data last week.

The negatives

As of Thursday most of the major indices were short term oversold having been down for 5 consecutive days. A violent rally on Friday took the NASDAQ composite (OTC) to a new multi year high, but left the breadth indicators and other major indices down for the week.

Today's headline in the WSJ is "Fed Closes In On Bond Exit". That should spook the market next week which seasonally has been weak anyway.

All of the breadth indicators deteriorated last week and the High Low ratio indicators which I consider among the most important are split, the NASDAQ derived indicators are pretty strong while the NYSE derived indicators are pretty weak.

The chart below covers the past 6 months showing the S&P 500 (SPX) in red and a 40% trend (4 day EMA) of NYSE new highs divided by (new highs + new lows), (NY HL Ratio) in magenta. Dashed vertical lines have been drawn on the 1st trading day of each month and dashed horizontal lines have been drawn at 10% levels for the indicator, the line is solid at the neutral 50% level.

NY HL Ratio fell from above 80% a week ago to under 50% Friday.

The positives

NASDAQ breadth data has held up better than NYSE breadth data.

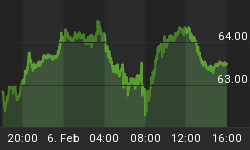

The next chart is similar to the one above except it shows the OTC in blue and OTC HL Ratio, in red, has been calculated from NASDAQ data.

OTC HL Ratio fell last week, but closed at a very strong 81%.

There are trading systems that impose a No Sell Filter when variations of this indicator are above 80%.

Seasonality

Next week includes the 5 trading days prior to the 2nd Friday of December during the 1st year of the Presidential Cycle.

The tables show the daily percentage return for the 5 trading days prior to the 2nd Friday of December during the 1st year of the Presidential Cycle.

OTC data covers the period from 1963 - 2012 while SPX data runs from 1953 - 2012. There are summaries for both the 1st year of the Presidential Cycle and all years combined. Prior to 1953 the market traded 6 days a week so that data has been ignored.

Next week has to be one of the worst weeks of the year during the 1st year of the Presidential Cycle. Since 1965 the OTC had only been up twice (the most recent time in 1985) and the SPX 4 times since 1953.

Report for the week before the 2nd Friday of December.

The number following the year is the position in the Presidential Cycle.

Daily returns from Monday to 2nd Friday.

| OTC Presidential Year 1 | ||||||

| Year | Mon | Tue | Wed | Thur | Fri | Totals |

| 1965-1 | -0.30% | 0.14% | 1.31% | 1.02% | 0.80% | 2.97% |

| 1969-1 | -0.66% | -1.02% | -0.32% | 0.28% | 0.60% | -1.13% |

| 1973-1 | 1.32% | -1.43% | -1.51% | -1.86% | 0.57% | -2.91% |

| 1977-1 | 0.05% | -1.13% | -0.12% | 0.20% | 0.49% | -0.50% |

| 1981-1 | -0.58% | -0.79% | 0.08% | 0.32% | -0.14% | -1.12% |

| 1985-1 | 0.09% | 0.13% | 0.49% | 0.54% | 1.06% | 2.32% |

| 1989-1 | 0.26% | 0.06% | -0.41% | -0.08% | -0.02% | -0.19% |

| Avg | 0.23% | -0.63% | -0.29% | -0.18% | 0.39% | -0.48% |

| 1993-1 | -0.15% | -0.23% | -0.19% | -0.83% | -0.10% | -1.49% |

| 1997-1 | 1.08% | -1.87% | -1.48% | -2.39% | -1.41% | -6.07% |

| 2001-1 | -1.44% | 0.49% | 0.47% | -3.23% | 0.34% | -3.36% |

| 2005-1 | -0.69% | 0.14% | -0.39% | -0.25% | 0.46% | -0.73% |

| 2009-1 | -0.22% | -0.76% | 0.49% | 0.33% | -0.03% | -0.18% |

| Avg | -0.28% | -0.45% | -0.22% | -1.27% | -0.15% | -2.37% |

| OTC summary for Presidential Year 1 1965 - 2009 | ||||||

| Avg | -0.10% | -0.52% | -0.13% | -0.50% | 0.22% | -1.03% |

| Win% | 42% | 42% | 42% | 50% | 58% | 17% |

| OTC summary for all years 1963 - 2012 | ||||||

| Avg | 0.17% | 0.05% | 0.02% | -0.39% | 0.26% | 0.10% |

| Win% | 62% | 50% | 53% | 46% | 56% | 52% |

| SPX Presidential Year 1 | ||||||

| Year | Mon | Tue | Wed | Thur | Fri | Totals |

| 1953-1 | -0.12% | -0.32% | -0.12% | -0.24% | -0.08% | -0.88% |

| 1957-1 | -0.94% | -0.88% | -0.12% | 0.10% | 0.44% | -1.40% |

| 1961-1 | 0.32% | -0.11% | 0.08% | -0.40% | 0.47% | 0.36% |

| 1965-1 | -0.75% | 0.88% | -0.12% | 0.31% | 0.26% | 0.59% |

| 1969-1 | -1.20% | -0.09% | -0.08% | 0.04% | 0.32% | -1.00% |

| Avg | -0.54% | -0.10% | -0.07% | -0.04% | 0.28% | -0.47% |

| 1973-1 | 1.49% | -1.95% | -2.57% | -1.27% | 0.99% | -3.32% |

| 1977-1 | -0.42% | -1.53% | -0.05% | 0.19% | 0.74% | -1.07% |

| 1981-1 | -0.85% | -0.30% | 0.53% | 0.18% | -0.62% | -1.05% |

| 1985-1 | 0.62% | 0.07% | 0.94% | 0.20% | 1.55% | 3.38% |

| 1989-1 | 0.22% | -0.52% | -0.29% | -0.28% | 0.32% | -0.55% |

| Avg | 0.21% | -0.85% | -0.29% | -0.19% | 0.60% | -0.52% |

| 1993-1 | 0.33% | 0.07% | -0.10% | -0.45% | -0.05% | -0.21% |

| 1997-1 | -0.14% | -0.67% | -0.61% | -1.53% | -0.16% | -3.12% |

| 2001-1 | -1.59% | -0.28% | 0.03% | -1.56% | 0.33% | -3.06% |

| 2005-1 | -0.24% | 0.13% | -0.50% | -0.12% | 0.28% | -0.45% |

| 2009-1 | -0.25% | -1.03% | 0.37% | 0.58% | 0.37% | 0.05% |

| Avg | -0.38% | -0.35% | -0.16% | -0.62% | 0.15% | -1.36% |

| SPX summary for Presidential Year 1 1953 - 2009 | ||||||

| Avg | -0.23% | -0.43% | -0.18% | -0.28% | 0.34% | -0.78% |

| Win% | 33% | 27% | 33% | 47% | 73% | 27% |

| SPX summary for all years 1953 - 2012 | ||||||

| Avg | 0.19% | 0.01% | 0.04% | -0.31% | 0.22% | 0.15% |

| Win% | 58% | 47% | 54% | 40% | 67% | 55% |

Money Supply (M2)

The money supply chart was provided by Gordon Harms. Money supply growth continued to decline last week.

Conclusion

The threat of tapering along with seasonal weakness is likely to take its toll on the market next week.

Just a wild guess: A little havoc in the financial markets will spook the Fed and they will promise to continue QE for the foreseeable future.

I expect the major averages to be lower on Friday December 13 than they were on Friday December 6.

Last week the OTC was up a little while the other indices were down a little so I am calling last weeks positive forecast a tie.

This report is free to anyone who wants it, so please tell your friends. They can sign up at: http://www.alphaim.net/signup.html. If it is not for you, reply with REMOVE in the subject line.

Gordon Harms produces a Power Point for our local timing group meetings. You can get a copy of that at: http://stockmarket-ta.com/. I have been having some trouble accessing the web site and hope to have that ready later in the day.

Good Luck,

YTD W 22/L 14/T 13