2013 was a year in which lots of imbalances built up but none blew up. The US and Japan continued to monetize their debt, in the process cheapening the dollar and sending the yen to five-year lows versus the euro. China allowed its debt to soar with only the hint of a (quickly-addressed) credit crunch at year-end. The big banks got even bigger, while reporting record profits and paying record fines for the crimes that produced those profits. And asset markets ranging from equities to high-end real estate to rare art took off into the stratosphere.

Virtually all of this felt great for the participants and led many to conclude that the world's problems were being solved. Instead, 2014 is likely to be a year in which at least some - and maybe all - of the above trends hit a wall. It's hard to know which will hit first, but a pretty good bet is that the strong euro (the flip side of a weakening dollar and yen) sends mismanaged countries like France and Italy back into crisis. So let's start there.

The basic premise of the currency war theme is that when a country takes on too much debt it eventually realizes that the only way out of its dilemma is to cheapen its currency to gain a trade advantage and make its debts less burdensome. This works for a while but since the cheap-currency benefits come at the expense of trading partners, the latter eventually retaliate with inflation of their own, putting the first country back in its original box.

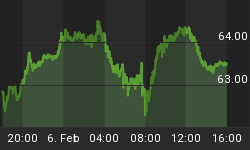

In 2013 the US and especially Japan cheapened their currencies versus the euro, which was supported by the European Central Bank's relative reluctance to monetize the eurozone's debt. The following chart shows the euro over the past six months:

For more details:

Euro rises to more than 2-year high vs. dollar; yen falls

The euro jumped to its strongest level against the dollar in more than two years on Friday as banks adjusted positions for the year end, while the yen hit five-year lows for a second straight session.

The dollar was broadly weaker against European currencies, including sterling and the Swiss franc. Thin liquidity likely helped exaggerate market moves.

The European Central Bank will take a snapshot of the capital positions of the region's banks at the end of 2013 for an asset-quality review (AQR) next year to work out which of them will need fresh funds. The upcoming review has created some demand for euros to help shore up banks' balance sheets, traders said.

"There's a lot of attention on the AQR, and there's some positioning ahead of the end of the calendar year," said John Hardy, FX strategist at Danske Bank in Copenhagen.

Comments from Jens Weidmann, the Bundesbank chief and a member of the European Central Bank Governing Council, also helped the euro. He warned that although the euro zone's current low interest rate is justified, weak inflation does not give a license for "arbitrary monetary easing.

The euro rose as high as $1.3892, according to Reuters data, the highest since October 2011. It was last up 0.3 percent at $1.3738.

The currency has risen more than 10 cents from a low hit in July below $1.28, as the euro zone economy came out of a recession triggered by its debt crisis.

Unlike the U.S. and Japanese central banks, the European Central Bank has not been actively expanding its balance sheet, giving an additional boost to the euro.

Here's what a stronger euro means for France, the second-largest and arguably worst-managed eurozone country:

French Economy Contracts 0.1% In Third Quarter

The final estimate of France's gross domestic product, or GDP, in the third quarter remained unchanged at the previous estimation of a contraction of 0.1 percent, indicating that the euro zone's second-largest economy is struggling to sustain the rebound it witnessed in the second quarter with a growth of 0.6 percent.

The third-quarter GDP growth was in line with analysts' estimates. According to data released on Tuesday by the National Institute of Statistics and Economic Studies, the deficit in foreign-trade balance contributed (-0.6 points) to the contraction in the third quarter, compared to the positive (0.1 percent) contribution made in the preceding quarter.

Some thoughts

At the beginning of 2013, most of the eurozone was either still in recession or just barely climbing out. Then the euro started rising, making European products more expensive and therefore harder to sell, which depressed those countries' export sectors and made debts more burdensome. So now, under the forced austerity of an appreciating currency, countries like France that were barely growing are back in contraction. And countries like Greece that were flat on their back are now flirting with dissolution.

Recessions - especially never-ending recessions - are fatal for incumbent politicians, so pressure is building for a European version of Japan's "Abenomics," in which the European Central Bank is bullied into setting explicit inflation targets and monetizing as much debt as necessary to get there. The question is, will it happen before the downward momentum spawns political chaos that spreads to the rest of the world. See Italian President Warns of Violent Unrest in 2014.