6/29/2014 6:29:28 PM

Market Summary

According to the Stock Trader's Almanac, QE taper may not be on a set course, but it sure does appear that way as the Fed once again did exactly what was expected at their most recent meeting. They cut monthly bond purchases by another $10 billion. They are still injecting $35 billion of new money monthly and are continuing to reinvest interest and principle from their existing holdings. This is still plenty of monetary support. Recent spikes in inflation were largely dismissed by the Fed with a single word, "noisy." Only time will tell if the Fed is correct with this assessment of if they are merely burying their heads in the sand. Previous Weekly Setup articles mentioned "No knowledgeable market watcher can seriously deny that the Federal Reserve's various iterations of Quantitative Easing (QE) is the steroid that has juiced the stock market to stratospheric levels.The reason all the 'expert' financial prognosticators keep getting it wrong about a market correction, crash, etc. is because they ignore that fact the Federal Reserve is supplying unlimited demand 'QE' to keep stock prices afloat. Company earnings, U.S. political system dysfunction, global political and economic unrest, chronically poor labor markets, etc., none of it have really mattered. Ben Bernanke started the free money train and Janet Yellen is committed to keeping it rolling, and until it comes to a complete stop, betting against this market is a very risky bet indeed."

The major indexes basically ended the week flat on a surge in trading volume to 8.9 billion shares on U.S. exchanges. The spike in volume at Friday's close was the result of Russell Investments' final reconstitution of its indexes, which affected more than $5 trillion in assets. The average volume for the month to date is about 5.6 billion. With only three trading days remaining in the first half of 2014, the Dow Jones Industrial Average and S&P 500 continue to track their respective Midterm Year and Sixth Year of Presidential terms seasonal patterns quite closely. On average, at the half-way point DJIA has been down 0.27% at the end of June. As of today's close DJIA was up approx.1.75%, not that far off the mid-point average. S&P 500 is typically off 1.05% at the end of June in midterm years since 1950. This year S&P is up 6.01%. Its superior performance is predominately due to its higher exposure to technology shares that have surged since mid-April. Even if the market closed the year at its current level it mark best three-year run for stock since 1997-1999 period.

The updated graph records quarter-to-date sector performance. We talked about how energy and utility stocks have outperformed the market recently, but you can see these sectors have been on a tear for most of the past three months.

Market Outlook

Since money managers have completed their 2nd quarter portfolio rebalancing and June quadruple witching week has ended, expect slow trading next week. Also, keep in mind the market is closed for the 4th of July holiday with some exchanges actually closing early on Thursday. Senior traders usually take most of the week off for vacation and will work remotely to deal with any major financial news. Otherwise, expect continued range-bound trading on light volume. As we said recently "According to the Stock Traders' Almanac, in the mid-1980s the market began to evolve into a tech-driven market and control in summer shifted to the outlook for second quarter earnings of technology companies. NASDAQ's mid-year rally from the end of June through mid-July is strongest. July is best month of the third quarter for the Dow and S&P. Since the bursting of the tech bubble in 2000, NASDAQ's mid-year rally has a spotty track record with seven appearances in the past twelve years. However, it has been solid for four years straight including a whopping 7.5% advance last year." In the updated performance graph below you can see that commodities such as energy and gold are the best performers for the month of June. And as mentioned above, Russell Investments reconstituted its indexes, plus investors' willingness to accept risk contributed to the Russell 2000 outperformance compared to the other equity indexes.

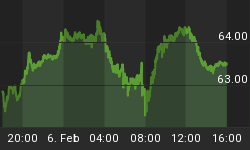

The updated Momentum Factor ETF MTUM Heikin-Ashi chart confirms last week's analysis "The market set up a 'bear trap' to squeeze short sellers, especially after investors responded favorably to this week's Fed announcement the bears had to chase prices to record highs." The chart shows the 'bear trap' was confirmed as the price remained near the highs and forced the bears to cover short positions.

Recent Weekly Setup analysis is still valid "CBOE Volatility index (VIX) closed at its lowest in more than seven years. To some, this suggests investors have become "complacent," that is, ignoring potential problems that could derail a rally, but a number of strategists suggested that just because investors aren't paying for protection does not mean they don't have worries."

Investors Intelligence Advisors Sentiment survey has reported over 60% bulls for four straight weeks after reaching a multi-year high two weeks ago. Similar lofty readings were recorded in August 1987, December 2004, October 2007 and at the end of 2013. Further excessive bullishness is seen in Weekly CBOE Put/Call Ratio declining to 0.47 last week, the lowest since January 2011. Traders and investors are most likely fully invested leaving little cash on the sidelines that actually wants to own stocks. The updated American Association of Individual Investor (AAII) survey below shows bullish sentiment close to the historical average. Neutral sentiment is a lot higher than normal and the bearish reading is well below average, from a contrarian perspective this suggest any surprise will be to the downside.

Previous analysis of National Association of Active Investment Managers (NAAIM) exposure index said "Professional money managers have gotten on board with the current bullish trend as their latest index is higher than last quarter's NAAIM 84.40% average reading. Another factor contributing to money managers' putting more funds to work is the need to rebalance their portfolios for the second quarter window dressing due at the end of the month..." The result end-of-quarter rebalancing act is money managers' 88.15% equity exposure.

Trading Strategy

We recently opined "The current gold rush has probably made most of its move and now is the time to takes some profits and/or tightens stops to lock in gains. If the price stalls out at resistance, a price neutral gold trade is probably a low-risk opportunity." The updated chart confirms gold has reached an inflection point where the price has to absorb overbought conditions to break through firm resistance and move higher.

Last week we said "Gold and treasury bonds continue to maintain an inversely correlated relationship. Depending on how your investment portfolio is set up, gold and treasury bonds can be used to hedge against each other and the equity market.Long bullish gold trades are now more risky since the price has surged and shorting gold is also a risky move at this point. But a long bullish Treasury bond trade is inexpensive and low-risk right now, and if/when gold drops you can expect bond prices to then move higher." The updated chart below demonstrates how as gold's upward momentum petered out, Treasury bond prices moved higher.

Last week the Weekly Setup offered this suggestion "Long bullish Treasury bond trade is inexpensive and low-risk right now." Treasury note yields fell to multi-week lows catapulting bond prices higher. The weaker than expected first quarter economic reports add conviction to the argument that the Federal Reserve will continue to accommodate even after its quantitative easing programs expire at the end of the year. "We're going to linger near current rate levels until we get a better bead on Q3 growth in the U.S. This is when we should get a better sense of the true run rate of the U.S. economy with numbers that will be presumably free of the weather distortions that made for such a bumpy ride in the first half of this year," William O'Donnell and Gabriel Mann of RBS said in a note.

Regards,