From the HRA Journal: Issue 216

Gold made the move I hoped for and predicted in the last issue. It's consolidating well above May price levels now. Traders will want to see a couple of more steps up in price to really get on board but the tone of the market has definitely improved again since early June.

Significantly, base metals have also shown a lot of relative strength in the past few sessions. It's been a long time since we have seen the whole metals complex on the move. That, even more than a lift in gold prices, signals changing perception by traders outside the resource space. To get the sort of rally we really want after three years of pain it's those outside traders we need. I think the leading edge is starting to arrive.

Reporting is still light but the number of companies that are opening trenches and drilling holes increased again so news is on the way. Most people still expect a weak summer market and I suspect there are many management groups trying to time events so they start reporting after Labour Day. That is standard operating procedure but if I'm right about how this year unfolds it won't be a standard year. New 52 week highs for the Venture are now only a couple of percent above current levels. Companies with material enough drill results will have to report them and it will only take one or two wins to move the Venture to new highs for the year.

Eric Coffin

Excuse the theft of the famous Buffalo Springfield song title but it came to mind as I reviewed recent market trends. In the last issue I postulated the resource market was due for a change, notwithstanding the recent drop in gold prices and widespread negativity about metals prices.

In the weeks since then we have indeed seem more life in the gold and silver markets. I expected that and, as I noted then, that wasn't based on a doom and gloom scenario. This move felt different since it tracked a surge in equities and better economic readings.

The chart below gives another side to this story. There has been a clear move upwards in the industrial metals index. It's still early but the break in the downtrend is dramatic. There is something happening here that isn't following the playbook of the majority that expect weak commodity prices for a long time to come.

In part, we can thank (or blame) Indonesia for the move in the index. Indonesia's concentrate tax has generated force majeure announcements by both Newmont and Freeport-McMoRan on their copper-gold mining operations in Indonesia. Both miners are running out of space to store concentrate as they negotiate to end the crippling tax. Newmont recently walked away from the bargaining table. These two mines (Batu Hijau and Grasberg) are big enough that the production halts would wipe out the projected copper oversupply this year if they don't come back online.

There will probably be a deal at some point. One worrisome aspect of this issue is that political rhetoric has gotten much tougher in Jakarta. There is a national election in a week and the two main presidential contenders are outdoing each other on anti-foreign investment comments. Hopefully that is just electioneering. If not this dispute could take a long time to fix.

I haven't included a nickel chart below but nickel has been the biggest winner in H1 2014 precisely because of Indonesia. That's ironic since almost all nickel produced in Indonesia comes from small local miners working laterite.

It's a huge job creator locally and none of those small firms can afford to build a smelter complex. I've been leery of the move on nickel because warehouse inventories of the metal are not dropping and it could be ahead of itself.

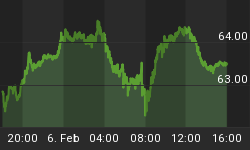

One chart I did include is zinc. I noted early this year that zinc could be one of the best performers this year and next. It's not impacted by Indonesia and, like copper, has broad uses across a number of economic sectors.

Zinc prices recently hit new highs, printing prices above $1.00/lb for the first time in three years. Inventories are still not low by historic standards but they have been dropping since early 2013 and that fall should continue. At the current pace warehouse inventories could be down to levels that could trigger larger price gains before year end.

I point out zinc in particular since it seems to be subject to less "extraneous" noise--like Chinese commodity financing or doom and gloom western traders. It's unsexy enough to be a useful guide to base metal complex demand and it ain't following the script either. A zinc supply deficit is projected but it looks like things are moving quicker than expected. I don't think its traders playing games--just good old fashioned demand.

Copper has been a head scratcher for me for months but there is no denying the strength of the chart right now. The fall in official warehouse inventories has been impressive and - unlike most other base metals - copper inventories are low by historic standards.

I've said before and I say again that I'm bothered by how low those inventories are. China is starting to come out of its funk and the US economy is starting to accelerate but both of those things are slow motion affairs. The drop in inventories looks suspiciously fast.

I still think a lot of the copper drawdown might just be sitting in un-bonded warehouses. If so, it's potentially available for sale and could still provide a nasty shock. Even so, the chart is the chart and there is clearly no shortage of copper traders expecting higher prices.

That brings me to the chart below and a theme I have touched on already this year. The five year US CPI chart below shows a distinct upturn in both core and headline inflation over the past few months. Significantly perhaps it also shows the "core" reading is beginning to converge with the headline "median" reading. That will make it tougher to dismiss higher median readings as being less meaningful (since none of us eat or drive).

Core CPI is now matching the US Fed's 2% target and personally I don't think it's going to stop there. There are reasons to expect some of the larger categories like Owner Equivalent Rent to keep rising and we're just starting to see the prices of goods rise--it's been mostly services up to now.

This isn't a "Weimar II" story. While money supply growth increases the odds of an inflation spike I don't think that is likely. This is a more mundane move based on a stronger economy, improved lending and higher demand. That's a good thing. Most of the move in base metals is basic demand but some is starting to come from traders expecting a lift in inflation. Copper has historically been a pretty good inflation hedge.

The June US payroll report came in way over consensus. This led to gains in equities and bond yields but also seemed to feed directly into the commodity complex. All the base metals had a very strong move the day the job report was released. Base metals don't drive money into the exploration sector as much as gold does but this adds to upward pressure I think is still building.

That brings us, finally, to gold and the juniors. Gold had the move I was hoping to see in the last issue. The main driver was comments by Yellen that convinced traders the Fed was happy to stay behind the curve.

The strong employment report may put a damper on things near term but I was encouraged by the relatively small drop in gold prices after the report. There was knee jerk selling after the strong job number but a drop of $8 is pretty minor by recent standards. The last Fed meeting has traders more inclined to believe the Fed will stick to its taper but is still in no hurry to raise rates.

Could higher inflation prints later in the year upset that? Yes, but even then I think the Fed will stay behind the curve. The odds are good we will see slightly higher inflation. Nothing scary--say 3% or a bit more. Real (inflation adjusted) interest rates should get more negative if anything, a positive for commodities.

We're into the doldrums but, even so, the Venture has managed to climb past its May high and the March high is in sight. I consider that the last hurdle on the way to a rally that will generate the 30% gain I expect from the TSXV. We are about to enter the period of strong positive seasonality for gold prices and traders are warming to base metals again. Add that all together and you have the makings of a rally, even during the dog days of summer.

Some minor good news has generated good reactions for explorers lately. A decent discovery or two and there is potential for my 30% target to be exceeded. Looks like game on to me.