U.S. stocks ended a holiday-shortened session mostly flat on Friday as a massive decline in the energy sector offset strength in consumer names. For the week, the Dow rose 0.1 percent, the S&P rose 0.2 percent and the Nasdaq rose 1.7 percent. It was the sixth straight weekly gain for all three. For the month of November, the Dow was up 2.5 percent, the S&P was up 2.5 percent and the Nasdaq up 3.5 percent.

In the updated chart below as the dollar got stronger at the end of the week, precious metals prices fell. Treasury prices jumped last week as result of a historical day in the bond market when there were all-time lows in 10-year yields in France, Germany, Italy, Spain, Netherland, Portugal, Switzerland and Japan.

Market Outlook

According to the Stock Trader's Almanac, the first trading days of every month since September 1997 for DJIA have produced nearly twice the gains of all other days combined. Most consistent gains were produced by the first day of February, April and May. However December's first trading day has not been as productive for DJIA or S&P 500. In the following table, the performance of the first trading day of December over the last 21 years is presented. Aside from disastrous 2008, first trading day of December losses have been relatively mild. The second worst loss, slightly more than 1% was in 1994. Gains of 1% or more have been more common with six, seven and nine occurrences for DJIA, S&P 500 and NASDAQ respectively. Since 2006, December's first trading day has been decidedly weaker with DJIA and S&P 500 declining six times in eight years.

December is the number one S&P 500 month and second best for DJIA since 1950, averaging gains of 1.7% on each index. It's also the top Russell 1000 and Russell 2000 (1979) month and second best for NASDAQ (1971). Rarely does the market fall precipitously in December. In midterm years, December's rankings slip modestly, but average gains remain inline. The "January Effect" of small-cap outperformance starts early in mid-December. Wall Street's only "Free Lunch" of distressed small- and micro-cap stocks making new 52-week lows on December Triple-Witching Friday will be served before the opening bell on December 22. Santa's Rally begins on Wednesday December 24 and lasts until the second trading day of the New Year. S&P has averaged gains of 1.5% since 1969. In years when Santa Claus did not come to Wall Street, bear markets or sizable corrections have often materialized in the coming year.

Investors are really gung-ho about the U.S. economy as smaller capitalization indexes like the Russell 2000 and Midcap 400 continue to lead the stock market over their larger cap brethren. Even more telling is that Dow Transport and Real Estate are the hottest asset classes in the fourth-quarter as these sectors are dependent on domestic economy performance.

As highlighted in the updated Momentum Factor ETF (MTUM) chart below the index has reached the extreme overbought level where you can expect the market to retrench. Also noted is the flat momentum which means there is no bullish surge to overcome if stock prices do began to fall.

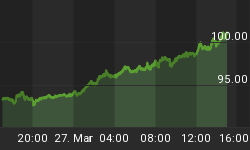

In the updated CBOE Volatility Index (VIX) graph below the index began creeping higher over the past few weeks but crashed this past week as the S&P 500 index once again reached new all-time highs.

Last week we said "...Options Put/Call ratio is another metric that we monitor for warning signs of an overextended market. The box below highlights the total Put/Call ratio number, which is currently extremely low. Normally, the number is close to "1.00" for a balanced market, but a lower number means investors are overinvested in call options. This is an extremely bullish reading and if the market turns lower investors will need to unwind these long calls to avoid loses..." This past week investors reversed the trend and started loading up on put options. The current put buying is not a signal that investors are turning bearish, but they are simply purchasing inexpensive insurance to protect profits as year-end looms.

The current American Association of Individual Investor Survey (AAII) survey bullish percentage is relatively high and contrarians consider this a sign of a looming price pullback. As a contrarian indicator, the AAII survey numbers are generally reliable, but keep in mind that an overly bullish reading can linger indefinitely before the market reacts.

Third-quarter National Association of Active Investment Managers (NAAIM) exposure index averaged 71.09. Last week the NAAIM exposure index was 72.06%, and the current week's exposure is 86.78%. The current exposure is the highest since June and indicates investment managers may be starting to buy high performing shares to put on the books for year-end window dressing.

Trading Strategy

According to Lipper Analytical Service, 2014 has shaped up to be the worst year in modern history for active stockpicking fund managers, with 85% of them failing to beat their benchmarks! It's almost unbelievable. Imagine if only 15% of the autos sold by car companies performed the way there were supposed to or what if airlines only got 15% of their flights to the destination on time. This is disastrous underperformance for the investment management industry. The moral of the story is you probably can do better taking time to do your own research and picking stocks yourself. You should be able to do better than most investment managers did last year by following a strategy of investing in top performing stocks from each of the leading sectors and selling shares in lagging sectors like energy.

Regards,