What a shock! The Federal Reserve as currently constituted is dovish!

It has really amazed me in recent months to see the great confidence exuded by Wall Street economists who were predicting the Fed will begin tightening by mid-year. While a tightening of policy is desperately needed - and indeed, an actual tightening of policy rather than a rate-hike, which would do many bad things but not much good - I was surprised to see economists buying the line being put out by Fed speakers on this (and I took issue with it, just last week).

Yes, the Fed would like us to believe that they stand sentinel over the possibility of overstaying their welcome. Their speeches endeavor to give this impression. But it is easy to say such a thing, and to believe that it should be said, and a different thing altogether to actually do it. Given that the Fed's "preferred" inflation measure is foundering; market-based measures of inflation expectations were in steady decline until mid-January; the dollar is very strong and global economic growth quite weak; and other central banks uniformly loose, in my view it seemed that it would have required a historically hawkish Federal Reserve to stay the course on a mid-year hiking of rates. Something on the order of a Volcker Fed.

Which this ain't.

Today the minutes from the end-of-January FOMC meeting were released and they were decidedly unconvincing when it comes to steaming full-ahead towards tightening policy. There was a fairly lengthy discussion of the "sizable decline in market-based measures of inflation compensation that had been observed over the past year and continued over the intermeeting period." The minutes noted that "Participants generally agreed that the behavior of market-based measures of inflation compensation needed to be monitored closely."

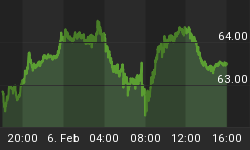

This is a short-term issue. 10-year breakevens bottomed in mid-January, and are nearly 25bps off the lows (see chart, source Bloomberg).

To be sure, much of this reflects the rebound in energy quotes; 5-year implied core inflation is still only 1.54%, which is far too low. But we are unlikely to see those lows in breakevens again. Within a couple of months, 10-year breakevens will be back above 2% (versus 1.72% now). But this isn't really the point at the moment; the point is that we shouldn't be surprised that a dovish FOMC takes note of sharp declines in inflation expectations and uses it as an excuse to walk back the tightening chatter.

The minutes also focused on core inflation:

"Several participants saw the continuing weakness of core inflation measures as a concern. In addition, a few participants suggested that the weakness of nominal wage growth indicated that core and headline inflation could take longer to return to 2 percent than the Committee anticipated."

As I have pointed out on numerous occasions, core inflation is simply the wrong way to measure the central tendency of inflation right now. It isn't that median inflation is just higher, it's that it is better in that it marginalizes the outliers. As I pointed out in the article last Thursday, Dallas Fed President Fisher seemed to be humming this tune as well, by focusing on "trimmed-mean." In short, ex-energy inflation hasn't been experiencing "continuing weakness." Median inflation is near the highs. Core has been dragged down by Apparel, Education and Communication, and New and used motor vehicles, and these (specifically the information processing part of Education and Communication, not the College Tuition part!) are among the categories most impacted by dollar strength. Unless you expect dramatic further dollar strengthening - and remember, one year ago there were still many people who were bracing for a dollar plunge - you can't count on these categories continuing to drag down core CPI.

Again, this isn't the current point. Whether or not core inflation heads higher from here to converge with median inflation (which I expect to head higher as well), and whether or not inflation expectations rise as I am fairly confident they will do over the next few months, the question was whether a Fed looking at this data was likely to be gung-ho to tighten policy in the near-term. The answer was no. The answer is no. And until that data changes in the direction I expect it to, the answer will be no.

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"