Market Summary

U.S. stocks ended the week with a massive rally, which helped generate the second consecutive week of gains. Oil recovered last week and Federal Reserve comments provided the fuel for a counter-trend bounce. The Bank of Japan also helped rally global stocks after unexpectedly adopting a negative interest rate policy for the first time. Even though the Dow surged 397 points on Friday, it still lost 5.5% of its value in January. That is the deepest monthly decline since the market correct last August. The Nasdaq fared even worse, sinking nearly 8%, its worst month since May 2010 when the infamous flash crash spooked investors. January got off to a terrible start, with panic about the slowdown in China and crashing oil prices sending the Dow to its worst 10-day start to a year on record going back to 1897. For the week, the S&P 500 Index jumped 1.7% while the Blue Chip-heavy Dow Jones Industrial Average's lead the major indices by rising 2.3%. The Nasdaq finished the week flat up a minimal 0.03% while the small cap Russell 2000 rose 1.5% for the week. As seen in the chart below, the major equity indexes finished January in a deep hole as investors sold off equities and deposited the funds into safe-haven assets like Treasuries and Gold.

A standard chart that we use to help confirm the overall market trend is the Momentum Factor ETF (MTUM) chart. Momentum Factor ETF is an investment that seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks exhibiting relatively higher price momentum. This type of momentum fund is considered a reliable proxy for the general stock market trend. We prefer to use the Heikin-Ashi format to display the Momentum Factor ETF. Heikin-Ashi candlestick charts are designed to filter out volatility in an effort to better capture the true trend. Last week's analysis stated "...the stock market is setting up for a "dead cat" bounce... equities are excessively oversold and displayed a bullish reversal sign at weeks end. As noted, downward momentum is dissipating which supports a short-term recovery..." This playing out as predicted with the updated chart below highlighting additional bullish reversal signs from the oversold bounce. More definitive is the momentum change from bearish to bullish.

Last week we said, "...MTUM has converted from a long-term uptrend into trading range established last summer. As long as it remains within the range it is reasonable to expect a near-term recovery bounce..." The updated weekly chart below confirms this analysis.

As evidenced in the chart below, Treasury prices rallied, pushing yields lower last week, after the Bank of Japan in a surprise move adopted a negative interest-rates policy. Yields declined throughout the month, with the two-year note posting its biggest monthly drop since Jan 2010 and snapping a three-month winning streak. Lower yields equate to higher bond prices as they have an inverse relationship. This is one of the unusual sequences when the dollar, treasuries and gold are moving in the same direction. Foreign investors are buying dollars to invest in safe-haven assets like treasury bonds and gold which is why they are all moving higher simultaneously.

Market Outlook

As reported by The Stock Trader Almanac, the January Barometer has only been wrong eight times since 1950 for an 87.9% accuracy ratio. This indicator adheres to propensity that as the S&P 500 goes in January, so goes the year and including the eight flat years yields a .758 batting average. Following the Santa Claus rally's "no-show," January's First Five Days were the worst on record. The Dow Jones Industrial Average violated its December closing low of 17128.55 on the third trading day and today the January Barometer is officially negative. The January indicator trifecta is negative across the board. Since 1950, this is only the eighth time that all three indicators were negative and the DOW's December closing low was violated. Of the previous seven occasions, February was up just twice with an average loss in all seven of 1.9% for S&P 500. However, the next 11 months and full-year S&P 500 was mixed, up four and down three albeit with a negative average performance. The graph below confirms investors trading "risk off" since the start of the year, as the only profitable asset classes are bonds and gold.

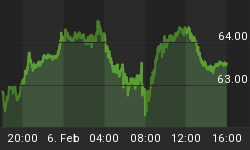

The CBOE Volatility Index (VIX) is known as the market's "fear gauge" because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends VIX higher. If the current counter-trend bounce continues expect the VIX and S&P 500 to converge in the chart below. The VIX is near its recent support level but should sink below it for the first time this year as stocks try to recover.

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 01/27/2016. The most recent AAII survey showed 29.80% are Bullish and 40.00% Bearish, while 30.30% of investors polled have a Neutral outlook for the market for the next six months. Last week's comment is coming to fruition "... The current AAII survey signals a short-term counter trend bounce is overdue based on retail investors' extremely bearish sentiment..." The bearish reading dropped last week and the bullish number rose, but they signal a follow-through on the current counter-trend bounce.

The Nation Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers' responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The current survey result is for the week ending 01/27/2016. Fourth-quarter NAAIM exposure index averaged 44.61%. Last week the NAAIM exposure index was 26.32%, and the current week's exposure is 42.25%. Similar to the end of September when the NAAIM Index fell near the 20% level, professional money managers have started bidding on oversold shares and increased equity their equity exposure during the current counter-trend bounce.

Trading Strategy

Keep in mind that while markets may have stabilized, they remain on edge. The CNNMoney Fear & Greed Index is currently flashing "fear," though that's actually an improvement from the "extreme fear" it displayed before trading started on last Friday. The obvious question is what will happen in the month of February. That probably will be determined by how the U.S. economy responds to global economic concerns, like whether oil prices stabilize and whether U.S stocks can stay decoupled from Asia. Fourth-quarter corporate reporting season is picking up steam, with S&P 500 companies on average expected to post a 4.1% drop in earnings, according to Thomson Reuters I/B/E/S. Excluding energy companies, earnings are seen rising 2.1%. If we get a spate of favorable earnings surprises and positive future guidance, investments in undervalued stocks that have been oversold during the correction could turn out to be a shrewd move. In the graph below the only positive S&P sector so far this year are Utility stocks. The biggest risk to investors is chasing stock prices higher as the market continues a counter-trend bounce, then stocks abruptly sell-off to resume the downtrend catching everyone by surprise - this is known as a "bear trap".

Feel free to contact me with questions,