Market Summary

U.S. stocks posted their best weekly gain since November. The Dow gained a whopping 794 points in just the last three days. The Dow's surge has cut losses for this year by almost half. "There's a good chance we've put in the lows for the quarter," says trader Tim Anderson, managing director of MND Partners. A mere five days ago, the Dow was down more than 10% for 2016. For the week, the S&P 500 Index jumped 2.8% while the Blue Chip-heavy Dow Jones Industrial Average rose 2.6%. The Nasdaq rose 3.6% while the small cap Russell 2000 led the major indices up almost 4% for the week. The Benchmark S&P 500 Index (SPX) is now out of correction territory but markets are sure to continue their wild swings in the near-term. You can see in the chart below that even after a big week the equity indexes are still deep underwater for the year. Treasury securities remain elevated and gold stocks are surging at a record pace.

A standard chart that we use to help confirm the overall market trend is the Momentum Factor ETF (MTUM) chart. Momentum Factor ETF is an investment that seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks exhibiting relatively higher price momentum. This type of momentum fund is considered a reliable proxy for the general stock market trend. We prefer to use the Heikin-Ashi format to display the Momentum Factor ETF. Heikin-Ashi candlestick charts are designed to filter out volatility in an effort to better capture the true trend. The orange box below denotes the Momentum Factor ETF trading range established last fall. A few weeks ago the MTUM dipped below the bottom of the trading range to threaten a downtrend. However there was no follow through on the breakdown and the ETF popped back up into the trading range. Until there is a confirmed break out of the trading range the best bet is to expect daily up and down stock price fluctuations.

A tool to help confirm the overall market trend is the Bullish Percent Index (BPI). The Bullish Index is a popular market "breadth" indicator used to gauge the internal strength/weakness of the market. It is the number of stocks in an index (or sector) that have point & figure buy signals relative to the total number of stocks that comprise the index (or sector). So essentially it is the percentage of stocks that have buy signals. Like many of the market internal indicators, it is used both to confirm a move in the market and as a non-confirmation and therefore divergence indication. If the market is strong and moving up, the BPI should also be moving higher as more and more stocks are purchased. The Nasdaq Composite Bullish Percentage Index (BPCOMPQ) chart below highlights a price uptrend line. Nasdaq stocks tend to lead the market and if recent behavior is a guide, investors bidding up Nasdaq stocks usually lead to higher near-term stock prices.

The dollar extended its decline last week, logging its worst three-week stretch since June 2013. Nervous investors seeking shelter in the world's third-largest economy have pushed the dollar down 7.1% vs. the yen since the beginning of the month, as concerns about global growth and market volatility linger. Treasury prices finished a volatile week that was dominated by swings in oil and equity markets marginally lower, snapping a three-week string of advances. Inflation data for January came in higher than expected while tumbling oil prices continued to drive investors to shun assets perceived as risky. As seen in the chart below, despite the major rise in equities this week, demand for the safety of Treasuries was consistent. Gold prices remain elevated at the highest level since February 2015.

Market Outlook

An analysis by Bespoke Investment Group found that the stocks that have gained the most in this rally were the ones that had the most investors betting against them only a few days ago. Many hedge funds are pulling back from those gloomy bets. While there's a lot of momentum in the market, the global economy remains weak. The other damper on this rally is it's hard to sort out how many "real buyers" have been jumping back in versus hedge funds simply comvering their short postions. "So far the market's bouncing almost perfectly to work off the oversold conditions we saw last week. There's still a whole lot of overhead resistance," said Adam Sarhan, CEO of Sarhan Capital. "I think people feel the market's stabilizing to a certain extent," Peter Coleman, head trader at Convergex, noting the S&P 500 rallied more than 6 percent from its low last week to its recent high this week. After three solid days of gains, Thursday's sell-off was "very mild. "I'm getting more constructive," he said. In the graph below you can see how the outlook for low interest rates has enhanced gold's appeal because it doesn't pay interest and investors are piling into gold funds at the fastest pace in seven years.

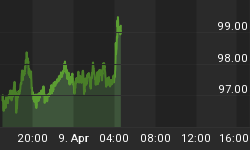

The CBOE Volatility Index (VIX) is known as the market's "fear gauge" because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends the VIX higher. The hourly Volatility Index chart below indicates that over the past week or so traders are becoming less apprehensive about the stock market. You can see that after reaching its highest level in the middle of the month the VIX is in a downtrend which coincides with the surge in "risk-on" trading last week.

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 02/17/2016. The most recent AAII survey showed 27.60% are Bullish and 37.80% Bearish, while 34.60% of investors polled have a Neutral outlook for the market for the next six months. The stock market is showing signs of bottom and retail investors are getting more optimistic as the bullish percentage jumped last week. As a reliable contra-indicator the current AAII survey signals continued follow through on a countertrend bounce.

The Nation Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers' responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The current survey result is for the week ending 02/17/2016. Fourth-quarter NAAIM exposure index averaged 44.61%. Last week the NAAIM exposure index was 32.87%, and the current week's exposure is 41.05%. The current NAAIM exposure index suggests that professional investors are slowly getting back into the game as they have gradually increased their equity exposure the past few weeks.

Trading Strategy

As reported by the Stock Traders Almanac, over the last 21 years, the market's performance in February has improved when compared to the longer-term record since 1950. DJIA has advanced in 14 of the last 21 February's with an average gain of 0.4%. S&P 500 has a similar record, up 13 of 21 with a slightly weaker average gain of 0.1%. NASDAQ is slightly weaker, up 11 times over the same period with just a 0.01% gain. The real star in February has been the Russell 2000 small-cap index, up 12 of 21 with a 0.8% average advance. This outperformance is mostly due to the lingering January Effect. The bulk of February's strength is usually located around mid-month, followed by a bout of weakness, another modest bounce and finally weakness the last two days of the month. Recent strength was a few days late this year and of greater magnitude. Should this February track the pattern from the past 21 years, some strength is likely early next week before the market begins to fade later next week. The updated graph below indicates investors converted to "risk-on" trading over the past month. Defensive Utility stocks had been the only positive group, but Industrial, Materials and Energy S&P Sectors led the market the past month. Now might be a good to "nibble" at some of the shares on your stock watch list - but keep tight stops.

Feel free to contact me with questions,