Market Summary

Feb. 11th was the 2016 low for the stock market. Since then easing concerns about slowing growth in China, as well as a possible U.S. recession, have triggered an explosive rally that in five weeks wiped out Wall Street's worst start ever to a year. After a sixth straight winning week the Dow Jones industrial average staged its biggest comeback from a deficit during a quarter since 1933. U.S. stocks erased losses for the year as the Federal Reserve's scaled-back path for interest-rate increases sparked demand for riskier assets. Crain's reported that actions by central banks to stimulate growth have fueled a rebound in risk assets from equities to raw-material prices, after almost $9 trillion was erased from global stocks at the start of the year. The Fed's updated projections indicate two quarter-point increases this year, down from four forecast in December. "Never underestimate the power of the Fed to impact the markets. The doves are clearly winning the argument resulting in yesterday's dovish announcement, which dragged the Fed back far more in line with market views on the potential for rate hikes in 2016," said Richard Perry, analyst at Hantec Markets, in a note. For the week, the S&P 500 Index advanced 1.4% while the Blue Chip Dow Jones Industrial Average rose 2.2%. The Nasdaq added 1.0% while the small cap Russell 2000 crawled up 1.3% for the week. As confirmed in the chart below, the Fed's dovish interest rate comments have stabilized treasury prices and continue to catapult gold stocks.

A standard chart that we use to help confirm the overall market trend is the Momentum Factor ETF (MTUM) chart. Momentum Factor ETF is an investment that seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks exhibiting relatively higher price momentum. This type of momentum fund is considered a reliable proxy for the general stock market trend. We prefer to use the Heikin-Ashi format to display the Momentum Factor ETF. Heikin-Ashi candlestick charts are designed to filter out volatility in an effort to better capture the true trend. Last week's analysis played out as advertised as we opined "...Next week is critical for determining the market trend...stocks are in a trading range. Most market technicians believe the most likely scenario is the MTUM will break out and continue higher in the direction of the current trend..." Technical analysis suggests there is still plenty of room for the uptrend to continue.

Put/Call Ratio is the ratio of trading volume of put options to call options. The Put/Call Ratio has long been viewed as an indicator of investor sentiment in the markets. Times where the number of traded call options outpaces the number of traded put options would signal a bullish sentiment, and vice versa. Technical traders have used the Put/Call Ratio for years as an indicator of the market. Most importantly, changes or swings in the ratio are seen as instances of great importance as this is commonly viewed as a change in the tide of overall market sentiment. The current Put/Call Ratio indicates traders are confident in the current bullish move as they are aggressively buying call contracts anticipating higher stock prices.

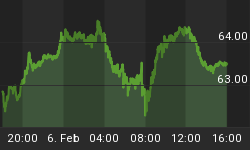

"This is a strong rally and the main catalyst is the return of easy money," said John Kilduff, a partner at Again Capital, a New York-based hedge fund that focuses on energy. "The Fed announcement yesterday was the latest sign that central banks are going to continue with stimulus. This is putting downward pressure on the dollar, which favors commodities." As evidenced by the Dollar Index (USD) in the chart below, the crashing U.S dollar is boosting commodity prices as demonstrated with the Commodity Index (CRB).

In the chart below, the dollar posted its biggest two-day loss since 2009 as the Federal Reserve's scaled-back path for interest-rate increases sparked demand for riskier assets. The dovish outlook sent the dollar sharply lower and spurred a rally in dollar-denominated commodities. Dollar-denominated assets like gold and treasuries jumped. Gold prices bounced higher as the U.S dollar continued its retreat after the Federal Reserve scaled back expectations for its next interest-rate increase.

Market Outlook

A few weeks ago we discussed the relationship between stocks and energy price when we said "...equity and energy prices have been trading in lock step all year. Market pundits have offered various analyses on why this is happening. There is usually unique asset classes associated with the movement of stock prices, e.g. dollar, bonds, interest rates, etc. Until this relationship is broken, some investors are observing energy prices as a clue to stock movement, especially for day trading..." Regardless of the driver, the oil rebound is putting Wall Street in a buying mood. The oil crash was viewed by many as a sign of impending economic collapse, causing the stock market to tank at the beginning of the year. But now the Dow has recouped all of its losses for the year, up from a stunning loss of nearly 2,000 points at one point. As mentioned previously, February 11th was the market low and the graph below displays asset performance since. In the graph you can see the results since the February correction are equivalent to more than an entire year of gains. What's notable is that the smaller cap higher risk stocks are leading the way, which confirms investors are committed to trading "risk-on".

The CBOE Volatility Index (VIX) is known as the market's "fear gauge" because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends the VIX higher. Our recent analysis has played out as predicted where we wrote "...VIX has fallen to its lowest level for the year...the VIX is in a downtrend which coincides with the surge in "risk-on" trading...If investors continue "risk-on" trading expect the Volatility number to keep falling lower...the Volatility Index continues falling to the lowest level since the end of last year. As investors have become more confident in the U.S. economy and near term direction of the stock market, expect the VIX to fall near November lows..." As recent market risk has subsided expect the VIX to stabilize near the support line, which is the November low mentioned last week.

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 03/16/2016. The most recent AAII survey showed 30.00% are Bullish and 26.90% Bearish, while 43.20% of investors polled have a Neutral outlook for the market for the next six months. Our recent analysis is validated as we have been saying "...As a reliable contra-indicator the current AAII survey signals continued follow through on a countertrend bounce... The latest AAII survey signals the current bullish trend has more room to run...Unless the Fed proffers a negative surprise during their meeting, the stock market should continue grinding higher according to the most recent AAII sentiment survey..."

The National Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers' responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The current survey result is for the week ending 03/16/2016. Fourth-quarter NAAIM exposure index averaged 44.61%. Last week the NAAIM exposure index was 51.01%, and the current week's exposure is 62.72%. Last week's prognostication came to fruition where we stated "...Professional traders are probably on hold as they await the results of next week's FMOC meeting. If they like what they hear from the Fed we expect the NAAIM Exposure Index to go higher..." The Fed's dovish stance is what money managers wanted to hear to continue increasing equity exposure.

Trading Strategy

Last week we mentioned "...As reported in the Stock Trader's Almanac... March's option expiration week...has a bullish bias...However, the week after tends to be bearish for DJIA and S&P 500..." The Trader's Almanac also says next week is a shortened trading week due to Good Friday and Easter. The days before Good Friday are generally positive and the shortened week also has a bullish slant. Rallies by industrial, raw-material and energy stocks helped the equity indexes climb all the way back from losses that reached over 11% a little over month ago. The updated graph below confirms our recent trading suggestions are working out as we said "...all systems are on go as all the major S&P sectors are positive over the past 30 days. As recession talk subsides and potential Fed rate increases fall off the table investors are increasingly willing to take on more risk...the best performing sectors are considered the highest risk equity classes. We are currently in the middle of what is considered the "best six months of the year" for the stock market. We like undervalued or oversold shares to bid on because the current bullish trend has more room to run..."

Feel free to contact me with questions,