Market Summary

Equites have recovered from the sharp early-year selloff and as seen in the chart below, most of the stock indexes are finally in the black year-to-date. For the week, the S&P 500 Index gained 0.5% while the Blue Chip-heavy Dow Jones Industrial Average rose 0.6%. The Nasdaq fell 1.5% while the small cap Russell 2000 led gains for the major indices finishing up 1.4% for the week. The Nasdaq composite posted two-straight weeks of declines and is 2% lower year-to-date, more than 6% below its 52-week intraday high. The Dow and S&P are up more than 3% and 2%, respectively, for the year so far.

A standard chart that we use to help confirm the overall market trend is the Momentum Factor ETF (MTUM) chart. Momentum Factor ETF is an investment that seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks exhibiting relatively higher price momentum. This type of momentum fund is considered a reliable proxy for the general stock market trend. We prefer to use the Heikin-Ashi format to display the Momentum Factor ETF. Heikin-Ashi candlestick charts are designed to filter out volatility in an effort to better capture the true trend. As highlighted in the chart below, the market was unable to break out of the top of its trading range on flat momentum. Now the question is will the break occur below the range.

In the chart below, the Nasdaq Index is lagging the large cap indexes. The Nasdaq is considered one of the market leaders when investors are committed to "risk-off" trading. If the Nasdaq doesn't catch up with the other indexes it might signal upward price movement will stall out sooner rather than later.

A Friday surge helped push the dollar to its strongest weekly gain against the yen since November 2014, a time when expectations that the Federal Reserve would soon raise interest rates were driving a massive run-up in the greenback. Reports that the Bank of Japan was weighing whether to extend negative interest-rate loans to banks -- a move analysts said would be tantamount to paying banks to borrow money -- helped drive a massive rally in the dollar, helping the U.S. currency log its large gain. Gold prices fell after European Central Bank President Mario Draghi indicated policy makers there could still cut interest rates further and the dollar rose. Treasury prices fell Friday for the fifth straight session, pushing yields to their highest level in a month, as strong gains in oil futures and high-yield debt dampened demand for safer assets including government debt. Treasury bonds logged their largest weekly drop since November, as the Treasury market has been moving under the influence of price action in so-called risk assets, namely equities, oil and high-yield bonds, analysts said. Treasury yields have been on a constant rise, not because investors are pricing in an interest-rate hike soon but because the rally in risk assets has led investors to sell Treasuries.

Market Outlook

As reported on CNN Money, the good news is that the recent dramatic comeback on Wall Street has erased painful losses in your portfolio. The bad news is there are growing questions about how long the rally can last because it isn't being fueled by improving corporate profits. That's why all of a sudden, U.S. stocks look pricey. In mid-February, when stocks were in free-fall mode, the S&P 500 was trading at 15.2 times its forward earnings. Not cheap, but not Manhattan Fifth Avenue prices either. Since then, the S&P 500 is up 15% and is even flirting with all-time highs. Its price-to-earnings ratio is now sitting at a lofty 17.5, the most expensive valuation multiple since September 2009 and among the highest levels since late 2004, according to S&P Global Market Intelligence. In some ways, it makes perfect sense for stocks to be more expensive these days. Many of the big fears -- a global recession, surging U.S. dollar and crashing oil prices -- have receded since then. Investors are now willing to pay a higher premium for stocks. Yet those fading fears haven't necessarily translated to stronger earnings, which reflect the true value of companies and their stocks. In fact, the S&P 500's earnings per share are now expected to be down 8% in the first quarter, compared with expectations earlier this year for a slight gain. It could end up being the third straight quarterly decline and the deepest since 2009. "The central banks have trapped us into buying expensive stocks because money market funds and the bond market give you extremely low returns," said Ed Yardeni, president of investment advisory Yardeni Research. Still, market valuations may not have much more room to expand from these levels without raising concerns of a bubble. That's why even longtime stock market bulls like Yardeni are ready for the market to take a breather. The chart below displays the recovery from the market bottom in February for major asset classes. Notice how investors are avoiding "safe-haven" assets and pouring funds into the riskier categories.

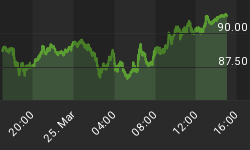

The CBOE Volatility Index (VIX) is known as the market's "fear gauge" because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends the VIX higher. You can see in the graph below, as the S&P approaches its all-time highs the VIX sinks to its lowest depth.

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 04/20/2016. The most recent AAII survey showed 33.40% are Bullish and 23.90% Bearish, while 42.70% of investors polled have a Neutral outlook for the market for the next six months. As we have been reporting the past few weeks "...The current AAII survey continues to signal a near-term neutral trend..."

The National Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers' responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The current survey result is for the week ending 04/20/2016. First-quarter NAAIM exposure index averaged 45.89%. Last week the NAAIM exposure index was 63.97%, and the current week's exposure is 82.50%. The current NAAIM equity exposure is the highest since last summer. At this lofty level, it is reasonable to expect money managers to reduce the amount of equity in clients' portfolio especially considering signs that stock valuations are becoming excessive.

Trading Strategy

"All the valuation metrics are saying stocks are expensive," said Ed Yardeni, president of investment advisory Yardeni Research. If multiples keep rising, "I'm going to have to conclude that profit taking is advisable," he said. So far, 77% of first-quarter earnings have exceeded expectations, which is superior to the 63% beat rate in a typical quarter. "What's driving the market right now is earnings and oil," said Thomas Wilson, Managing Director of Wealth Advisory at Brinker Capital. "If earnings results come in above the very low bar of expectations that are out there and you combine that with a continued rising price of oil, which should equate to an upward trend in the market next week." In the graph below you can see that along with Healthcare, Energy and the related Materials sector are the outperformers.

Feel free to contact me with questions,