Gold has hit the ground running in this young new year, a stark contrast to its brutal post-election selloff. Rather remarkably, these strong recent gains accrued despite literally zero buying from one of gold's most-important constituencies. The American stock investors who almost single-handedly fueled gold's strong bull market last year are still missing in action since the election. That means big gold buying is still coming.

All free-market prices, including gold's, ultimately result from the balance between popular supply and demand. When supply outweighs demand as evidenced by investment-capital outflows, gold is forced lower. That's exactly what happened after Trump's surprise win in early November. When investors flee gold for any reason, including chasing record-high stock markets, the resulting oversupply really hits prices.

When the votes started to get tallied on Election Day's evening, Trump pulled into a surprise lead in the biggest battleground state of Florida. Gold futures rocketed higher on that, soaring 4.8% to $1337 as the early results came in! But as the plummeting stock-market futures reversed sharply the next morning, that panic gold buying was quickly unwound. That kicked off investors' subsequent mass exodus from gold.

Over the last decade or so, gold ETFs have grown to dominate gold investment. Their soaring popularity is the direct result of their unparalleled efficiency. There is no cheaper, quicker, or easier way for stock traders to move capital into this unique asset to gain gold portfolio exposure. So gold investment has increasingly shifted from the traditional holding of physical bars and coins to owning gold-ETF shares.

The 800-pound gorilla of the gold-ETF world has always been the American GLD SPDR Gold Shares. As of the end of Q3'16, the latest data available from the World Gold Council, GLD's commanding lead among global gold ETFs is impregnable. GLD held 948.0 metric tons of gold bullion in trust for its shareholders, or a staggering 40.6% of the total holdings of the world's top-ten physically-backed gold ETFs!

This dominance along with GLD's extreme transparency make it the best proxy for investment-capital flows into and out of gold. Every single trading day, GLD's managers release the total gold bullion this ETF is holding. This is done in extraordinary detail to placate anti-gold-ETF conspiracy theorists, down to the individual-gold-bar level including serial numbers and weights. This week's list was 1305 pages long!

The day after the election, GLD's physical gold-bullion holdings were running 955.0 tonnes. But as the stock markets soared in the post-election Trumphoria surrounding hopes of lowering taxes and slashing regulations, investors started to flee gold. Gold is a unique asset that often moves counter to stock markets, making it an anti-stock trade. Thus gold investment demand collapses when stocks trade near record highs.

Investors simply feel no need to prudently diversify their stock-heavy portfolios with gold when the stock markets seem to do nothing but rally. So after Trump's win, stock investors soon began to dump GLD shares at far-faster rates than gold itself was being sold. This differential selling pressure forced GLD's managers to sell physical gold bullion to raise the necessary cash to sop up the excess GLD-share supply.

As a tracking ETF, GLD's mission is to mirror the gold price. But GLD shares have their own supply and demand totally independent from gold's, so GLD-share prices are always on the verge of decoupling from gold. The only way to maintain tracking is to shunt excess GLD-share supply and demand directly into physical gold itself. So GLD effectively acts as a conduit for stock-market capital to slosh into and out of gold.

Stock investors jettisoned GLD shares so fast in mid-November that this ETF's holdings fell sharply for 11 trading days in a row. Every day GLD-share selling outpaced gold selling, so every day this ETF had to buy back the excess shares to offset that heavy differential selling. The money came from selling gold bullion, resulting in daily draws in GLD's holdings. That short span saw GLD's holdings plunge by 7.3% or 70.0t!

While this extreme selling moderated in December, it still continued relentlessly. Gold was driven down to $1128 the day after the Fed hiked rates for the second time in 10.5 years. While that was expected, the Fed officials' rate-hike projections for 2017 were more hawkish than expected. That happened to mark the very bottom for gold, yet the heavy GLD selling persisted. That day GLD's holdings were at 842.3t.

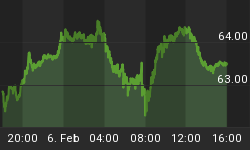

As of the Wednesday data cutoff for this essay, gold has rebounded 5.6% since then. It has rallied back up to late-November levels. A strong bounce out of extreme bearishness was inevitable, as I wrote that very week. But what's wildly unexpected is since gold bottomed GLD's holdings have fallen another 4.4% or 37.3t to 805.0t. GLD still hasn't seen a single holdings build since the day after the election!

So gold somehow managed to rally sharply in recent weeks without any capital inflows from American stock investors. They not only weren't buying GLD shares, they continued to aggressively sell them as evidenced by a couple big GLD-holdings draw days so far in January. This situation is remarkable, as it implies the investment gold buying hasn't even started yet. That means big gold buying is still coming.

Some perspective is necessary to understand the supreme importance of GLD capital flows for gold's performance. This first chart looks at gold and GLD's holdings over the entire lifespan of this pioneering gold ETF. After its November 2004 birth, every subsequent year shows what happened to both its gold-bullion holdings and the gold price. Stock-market-capital flows via GLD have long dominated gold's fortunes.

While differential GLD-share buying and selling isn't the only force moving gold, it is certainly one of the two primary ones along with American gold-futures trading. In general gold rises and falls based on the capital inflows or outflows via GLD as evidenced by its builds and draws. Gold almost always rallies in years stock traders buy GLD shares faster than gold, and conversely falls in years where they sell GLD faster.

In 2005, 2006, 2007, 2008, 2009, and 2010 gold rallied majorly on strong GLD builds. When investors want to prudently expand their portfolio gold exposure through adding GLD shares, this ETF's resulting physical-gold-bullion buying propels gold's price higher. This makes sense, as the more capital bidding on any particular asset the faster its price will rise. That's simply supply and demand in action as expected.

2011 was the lone year since GLD's birth where the gold price disconnected from GLD's holdings. That year gold rallied another 10.2% despite a 2.0% GLD draw. But with a mere 26.2t move, that was also the least-volatile GLD-holdings year by far. So GLD's holdings were essentially unchanged, certainly not down materially. That relative cessation of differential GLD-share buying or selling allowed gold to decouple.

2012 again saw a solid GLD build, and gold rallied in lockstep. By that point, GLD had never suffered a sustained draw. Gold ETFs are a double-edged sword, just as easy to sell as they are to buy. In early 2013 the Fed's radically-unprecedented new open-ended third quantitative-easing campaign started to levitate the stock markets. So gold investment demand cratered as stocks seemingly did nothing but rally.

American stock investors dumped GLD shares with a vengeance that year, resulting in an epic 40.9% or 552.6t GLD draw! That wild unparalleled flood of gold-bullion supply spewed by GLD as it sold to raise the cash to buy back the excess shares offered hammered gold 27.9% lower. That made for gold's worst year since 1981, soon after a gold popular mania failed. That extreme gold-ETF selling kept feeding on itself.

The more stock investors dumped GLD shares, the more gold fell. The more gold fell, the more investors wanted to dump GLD shares. That ugly episode proved that gold ETFs and their easing of capital flows into and out of gold would amplify both bulls and bears. 2014 and 2015 saw gold continue to fall as the differential GLD-share selling continued. GLD's draws those years ran 89.2t and 66.6t, key reference points.

Despite the sharp post-election selloff driven by that Trumphoria stock rally, gold still advanced 8.5% last year. On Election Day it had been up 20.3% year-to-date! 2016 proved gold's first up year since 2012. And not coincidentally, 2016 was the first year that saw a GLD build since 2012. And that 179.8t of gold-bullion buying GLD had to do last year was actually the third-largest GLD-build year in this ETF's history.

So realize that stock-market capital flows into and out of gold via this dominant world-leading GLD gold ETF are critical. Gold rallies when stock investors are buying GLD shares faster than gold, leading to builds as that excess buying is shunted into gold. And gold falls when GLD shares are sold faster than gold, which forces this ETF to sell bullion to buy back its own shares. Gold only makes sense with this knowledge!

Unless you understand GLD's commanding role, you can't understand why gold has been where it's been or going where it's going. This next chart zooms in to the past couple years or so, and increases the analysis resolution to quarterly. The reason gold soared in Q1 and Q2 last year is because stock-market capital was flooding into GLD. And the reason gold collapsed in Q4 is because half of that capital fled.

Gold's lone up quarter in 2015 in Q1 was the result of a GLD build. The other three quarters of that year saw gold fall on increasing differential GLD-share selling. Interestingly gold bottomed the day after the Fed hiked rates for the first time in 9.5 years in December 2015, at a 6.1-year secular low. Exactly a year later last month, gold again bottomed the day after the next Fed rate hike. It's irrational to fear Fed rate hikes!

Gold then skyrocketed 16.1% higher in Q1'16 on a monstrous 27.5% or 176.9t build in GLD's holdings. Gold investment demand quickly shifted from deeply out of favor to back in favor for one simple reason. The lofty Fed-goosed stock markets were rolling over into a correction-grade selloff as 2016 dawned. As the anti-stock trade, gold investment demand soars when stock markets materially weaken and stoke fear.

Gold's first new bull market since 2011 was overwhelmingly driven not just by gold ETFs, but specifically by GLD alone. According to the definitive arbiter of gold supply-and-demand measurement, the World Gold Council, total global gold demand climbed 219.4t year-over-year in Q1'16. Thus GLD's 176.9t build accounted for a staggering 80.6% of that jump! Traditional bar-and-coin demand merely rose 0.7% YoY.

So if American stock investors hadn't flooded back into GLD in Q1'16 as US stock markets rolled over, there never would've been a new gold bull! Love it or hate it, the hard reality is American stock-market capital flows into and out of gold via GLD now dominate this metal's price behavior. That became even more apparent in Q2'16, when gold rallied another 7.4% on another huge 16.0% or 130.8t GLD build.

Per the WGC, overall global gold demand climbed 139.8t YoY that quarter. That means GLD alone was responsible for a mind-boggling 93.6% of the world total! Again bar-and-coin demand was dead flat, the whole gold story was differential GLD-share buying. Indeed in Q3 gold stalled because that differential GLD-share buying ceased. Gold drifted 0.4% lower in Q3'16 on a trivial 0.2% or 2.1t GLD draw that quarter.

So realize that pretty much everything that happened to gold last year before the election was the result of stock-market capital flowing into and out of gold via the GLD conduit. Thus it shouldn't be a surprise that the brutal gold selloff after the election was driven by extreme differential GLD-share selling. On Election Day, GLD's holdings were actually only just 3.4% under their bull-market high seen back in early July.

That subsequent extraordinary 11-trading-day 7.3% GLD draw was driven by US stock markets surging to new all-time record highs per the benchmark S&P 500. Stock investors were so enthralled by Trump's promises of lower taxes and less regulation that they lapsed into euphoria. Just as in 2013 to 2015, they figured why bother owning counter-moving gold if stocks are going to do nothing but rally indefinitely?

The resulting extreme differential GLD-share selling ultimately drove a massive 13.3% or 125.8t Q4'16 draw! Those stock-capital outflows were nearly equivalent to Q2'16's 130.8t inflows. But gold didn't bottom at Q2 levels since futures speculators joined the stock investors in aggressively dumping gold. Q4's enormous 125.8t GLD draw dwarfs those 89.2t and 66.6t draws seen in the full years of 2014 and 2015.

With so much capital fleeing gold, forcing GLD to spew so much gold bullion into the market to buy back its excess shares offered, it shouldn't be surprising gold cratered to a 12.7% loss in Q4. That was one of gold's worst quarters ever, driven by one of GLD's biggest draw quarters ever. Gold prices are driven at the margin by investment capital flows, and there is no bigger pool of gold investment capital than GLD investors'.

Given GLD's ironclad dominance over gold prices, the disconnect between gold and GLD holdings in recent weeks is utterly stunning. Every day the first piece of data I check is what happened in GLD's holdings the day before. They aren't reported until evenings well after the markets close. So ever since gold started to rally in late December, I've been looking for GLD builds to resume. Yet they still haven't.

As of Wednesday, GLD had not seen a single build in 42 trading days since the day after the election! That now rivals a 42-trading-day span in mid-2013 as the longest in history without any GLD builds. If you'd told me a month ago that gold could mount a nearly-month-long 5.6% rally despite not only zero GLD builds but a cumulative 4.4% draw, I would've laughed. That's wildly improbable based on modern history.

Yet here we are. Gold's bull market of 2016 is resuming after this metal's 17.3% plunge mostly since the election, which didn't breach the 20% new-bear threshold. And American stock investors not only didn't drive it, but they are actively fighting it. That means the gold investment buying hasn't even started yet from the only group of global investors who really matter! Big gold buying is still coming via GLD shares.

American stock investors totally ignored gold in late 2015 until the US stock markets retreated decisively enough to crack the complacency bubble driven by record highs. GLD's holdings fell to a 7.3-year secular low the day after the Fed's first rate hike in nearly a decade in December 2015 as stock markets remained near records. It wasn't until the stock markets started selling off that gold investment demand reignited.

Right after that December-2015 rate hike, the S&P 500 dropped 1.5% and 1.8% on back-to-back trading days. That relatively-minor selloff was enough to convince hyper-complacent stock investors that maybe owning a little gold to diversify their stock-heavy portfolios wasn't a bad idea. January 2016 would see a lot more major S&P 500 down days with losses of 1.5%, 1.3%, 2.4%, 2.5%, 2.2%, and 1.6% as selling accelerated.

That heavy stock-market selling ultimately fueling a correction-grade 13.3% S&P 500 selloff was exactly what triggered last year's new gold bull. And once that investment gold buying got underway, it took on a life of its own as investors love to chase winners. Even though the S&P 500 bottomed decisively for the year in mid-February, gold kept powering dramatically higher until early July on continued heavy GLD buying.

This precedent is exceedingly bullish for gold today. As I explained in depth in an essay at the very end of 2016, a major stock bear still looms. The US stock markets were radically overvalued before that crazy Trumphoria rally, which blasted them up to formal bubble valuations! Corporate earnings are simply far too low to support the high prevailing stock prices, which are purely the product of greed and euphoria.

Even if Trump proves a miracle worker, the much-anticipated lower tax rates and regulation-slashing is going to take some time to implement. I can't imagine anything big happening on those fronts before late 2017 or early 2018 at best. In the meantime, the stock markets are long overdue for at least a 10%+ correction and more likely a 20%+ new bear. That will once again revive major gold investment demand.

If a 13% stock correction ignited a 30% gold bull in the first half of 2016, imagine what a real bear would do for gold prices. American stock investors are radically underinvested in gold today, with essentially zero portfolio exposure. So as stocks inevitably sell off as the impossible Trumphoria expectations inevitably lead to deep disappointment, there is vast room for American stock investors to diversify back into gold.

While gold has indeed looked impressive in recent weeks, we haven't seen anything yet compared to what will happen when differential GLD-share buying explodes again. Gold's upside in early 2017 truly has the potential to even exceed early 2016's strong gains! The stock markets are far more precarious now than a year ago, and the more downside they suffer the more investors will shift capital back into gold.

This coming major new upleg in this young gold bull can certainly be played with GLD or call options on it. But the gains in the gold miners' stocks will dwarf the gains in gold, since their profits growth greatly leverages gold's upside. As I discussed in depth last week, we are already seeing that. Over that recent less-than-a-month span where gold rallied 5.6%, the leading gold-stock index already surged 21.0% higher!

At Zeal we aggressively bought and recommended great gold stocks and silver stocks to our newsletter subscribers back in December when everyone remained hyper-bearish. Our unrealized gains on these brand-new trades are already running as high as +50% this week! If you too want to thrive in these markets, it is essential to stay informed all the time. Wealth is multiplied by first buying low when few others will.

We've been in the contrarian-research business helping investors and speculators thrive for over 17 years now. Since 2001 we've recommended and realized 906 stock trades in real-time to our newsletter subscribers. Their average annualized realized gains including all losers are now running way up at +22.0%! You can put our expertise to work for you through our popular weekly and monthly newsletters. They draw on our vast experience, knowledge, wisdom, and ongoing research to explain what's going on in the markets, why, and how to trade them with specific stocks. Subscribe today for just $10 per issue!

The bottom line is big gold buying is still coming. American stock investors, the driving force behind all of gold's major moves for years, haven't even started returning to gold yet. The leading GLD gold ETF hasn't seen a single build since the day after the election, and has continued to suffer major draws in early 2017. Gold's sharp rebound out of its post-election lows despite a GLD-selling headwind is remarkable.

Just as a year ago, all it will take to rekindle gold demand from American stock investors is a correction-grade stock-market selloff. And one is way overdue and increasingly likely thanks to all the extreme distortions of valuations and sentiment the Trumphoria rally spawned. As stock complacency cracks, American stock investors will rush back to gold to diversify their portfolios and thus catapult it much higher.