Market Summary

For the week, the S&P 500 Index was basically flat up .2% while the Blue Chip-heavy Dow Jones Industrial Average finished where it started. The Nasdaq finished led the market up 2.2% on the strength of biotech’s while small cap Russell 2000 was up .5% and Midcap 400 moved down .54%. You can see in chart below how all the major asset classes are higher for the first half of the year.

A tool to help confirm the overall market trend is the Bullish Percent Index (BPI). The Bullish Index is a popular market “breadth” indicator used to gauge the internal strength/weakness of the market. Like many of the technical market internal indicators, it is used both to confirm a move in the market and as a non-confirmation and therefore divergence indication. Nasdaq stocks have been leading the market direction for the past eighteen months. Last week’s analysis stated “…Whenever the Nasdaq index stocks falter the overall market usually stalls which is what currently appears to be the case… If the BPCOMPQ chart continues its current downtrend it might be difficult the major stock indexes to start making new highs again…” Right on queue in the updated chart the BPCOMPQ suddenly started trending higher and it appears are ready to follow.

A standard chart that we use to help confirm the overall market trend is the Momentum Factor ETF (MTUM) chart. Momentum Factor ETF is an investment that seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks exhibiting relatively higher price momentum. This type of momentum fund is considered a reliable proxy for the overall stock market trend. We prefer to use the Heikin-Ashi format to display the Momentum Factor ETF. Heikin-Ashi candlestick charts are designed to filter out volatility in an effort to better capture the true trend. Recently we have been saying “…stocks are due for a pause this week to absorb overbought conditions and as investors analyze the comments coming out of the upcoming FOMC meeting…the MTUM ETF consolidating into a tight trading range…momentum is starting to turn negative. The long-term trend remains bullish; however neutral is the near-term trend to allow absorbing overbought conditions before the market continues higher…” This analysis is playing out as advertised; the major indices will probably approach new highs over the next few weeks.

In the chart below the dollar had its best week in two months, helped by the hawkish tone from the Federal Reserve, and we expect this tactical rally to continue,” said Hans Redeker, currency analyst at Morgan Stanley, in a note. Gold climbed for a third session in a row Friday, but its rise on the back of declines in the U.S. dollar and recent weakness in assets perceived as risky wasn’t enough to give the metal’s prices a boost for the week. “Gold is consolidating from the recent drawback, but is still in a correction mode, to be clear,” said Nico Pantelis, head of research at Secular Investor.” We should be nearing the bottom of the current correction in the next week or two, from where a bigger climb should start. We think August could be an ideal month to kick-start this new uptrend in gold, which could last till the end of the fall.” While stocks are near record highs, Treasury prices have not broken down and are still in demand. They are telling mixed sentiment as the safety trade in bonds is still intact and is reflecting little expectation for any future rate hikes.

Market Outlook

According to an article by Sara Sjolin published in MarketWatch, if investors are looking for 10% return over the next six months, look no further than the U.S. stock market. Yes, the American benchmarks may have consistently set fresh all-time highs over the past weeks, but the rally isn’t over yet, according to Jim McCaughan, CEO of Principal Global Investors, which oversees $424 billion in assets. “In the U.S., this is the bull market that nobody loves. It has been going on since 2009, but there are a lot of people on the sidelines that have been cautious about it,” he told MarketWatch at the International FundForum conference in Berlin earlier this week. “But the market hasn’t gone to bubble levels yet. It hasn’t gotten to the point where we say its ‘1999 overvalued.’ That was when P/E forwards of 50 times were common and the average P/E now is 18 times. It’s high, but it’s not high compared with where bond yields are. I’m still of the view that U.S. equities remain a buy on setbacks,” McCaughan added.

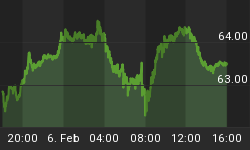

The CBOE Volatility Index (VIX) is known as the market’s “fear gauge” because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends the VIX higher. In the updated chart below the CBOE Volatility index is reflecting the bullish trend for equities. The closely watched CBOE Volatility index (VIX) is showing little signs of downside risks for stocks. With mixed economic data and earnings season still three weeks away, it would most likely be geopolitical risks that could provide any volatility.

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 06/21/2017. A modest decrease in the percentage of individual investors who expect stock prices to decline sent pessimism to a four-month low. Bearish sentiment, however, remains close to its historical average in the latest AAII Sentiment Survey. Bearish sentiment, expectations that stock prices will fall over the next six months, declined 0.6 percentage points to 28.9%. Pessimism was lower on February 15, 2017 (27.7%). Bearish sentiment has been slightly below its historical average of 30.5% during six out of the last seven weeks. Additionally, this week’s survey shows small increases in optimism and neutral sentiment. Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, rose by a mere 0.2 percentage points to 38.4%. This is both the eighth consecutive week and the 13th out of the last 14 weeks with a neutral sentiment reading above its historical average of 31.0%. Bullish sentiment, expectations that stock prices will rise over the next six months, rose 0.4 percentage points to 32.7%. Optimism is below its historical average of 38.5% for the 17th consecutive week and the 22nd time out of the last 23 weeks. Record highs for the S&P 500 and the NASDAQ have encouraged some individual investors, but the Trump administration’s ability (or lack thereof) to move forward on economic and tax policy remains on the forefront of many others’ minds. Also, playing a role in influencing sentiment are earnings, valuations, concerns about the possibility of a pullback in stock prices and interest rates/monetary policy.

The National Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers’ responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The current survey result is for the week ending 06/21/2017. First-quarter NAAIM exposure index averaged 92.85%. Last week the NAAIM exposure index was 92.61 %, and the current week’s exposure is exactly the same at 92.61%. Last week we mentioned this might happen when we said “… Money managers will probably maintain the current level of equity exposure heading into end-of-quarter performance reporting…”

Trading Strategy

An article in the Almanac Trader referenced how the NASDAQ delivers a short, powerful rally that starts at the end of June with the NASDAQ averaging a 2.4% gain since 1985 during the 12-day period from June’s third to last trading day through July’s ninth trading day. This year the rally could begin around the close on June 27 and run until about July 17. In the S&P 500 Sector ETF graph below the Health Care sector is exploding as the Senate healthcare bill will be voted on next week. The Bill is an improvement over the House attempt but many expect it won’t pass as four Republicans will most likely not vote in favor of it. Look for some quick profits over the next few weeks and the opportunity to set up some longer-term credit spreads.

By Gregory Clay