Where to begin when you've got a lot of ground to cover? Great question, whether you are setting out on a vacation, an overhaul of a company's strategic direction or in my case - peeling back some of the opaque layers, hiding a great deal of the obfuscated facts in today's gold market.

I would like to share a few words of wisdom of economist Jude Wanniski - who is perhaps best known as the associate editor of The Wall Street Journal from 1972 to 1978. In 1976 Wanniski coined the term supply-side economics to distinguish the revival in classical economic thought from the more dominant "demand-side" Keynesian and monetarist theories. The importance/function of a free market price of gold, from Wanniski's Supply Side Economics Universtiy Lesson # 13:

3. "It must be a SIGNAL. David Ricardo in 1823 said it best when he argued that money is working at the peak of efficiency when the central bank need hold no gold. By that he meant if the market totally believed the bank would not depart from the price commitment, the bank would not have to keep physical resources in reserve, but could lend them as well. Modern supply-siders, whether Mundellians or Lafferians (who have differences of opinion on the correct mechanisms of a gold standard), agree that the most important function of gold is as a signal. It is a price that is determined by all of humanity, in the sense that anyone can demand gold or supply gold, the same way anyone can demand or supply bread or cheese. A gold standard is democratic, while fiat money is elitist. When everyone can participate in setting the gold price by demanding and supplying in relation to the supply of dollars, it is more likely that mass will find the optimum price than if Alan Greenspan and his colleagues make decision[s] sic behind closed doors".

Wanniski is telling us that the significance of a rapidly rising price of gold is a SIGNAL of trouble ahead. These troubles specifically refer to the inflationary policies being pursued by Central Banks - the creators of money. This assessment of the importance/relevance of a rising price of gold is consistent with the utterances of another famous economist, Mr. Paul Volcker - former Chairman of The Federal Reserve, from this Jay Taylor essay:

"In looking back at the rise of gold from $35 to $850 during the 1970s', Paul Volcker said, "It was probably a mistake to allow gold to rise so high." Not only does that statement presuppose that the U.S. could have controlled the gold price, but it also suggests the establishment's arrogance in assuming they have a right and obligation to do so. How anyone believes gold is not manipulated from time to time is a mystery to me, given all the evidence provided by the Gold Anti Trust Action Committee (GATA), Reginald Howe's lawsuit as well as the Blanchard lawsuit, and given the importance of keeping the public believing in paper as money rather than gold. I guess people simply believe what they want to believe".

Mr. Paul Volcker and for that matter all Central Bankers, view the rising gold price signal as an unwelcome occurrence because it signals failed policies on their part. What I find troublesome in his words, is the suggested belief that Central Bankers have the right and obligation to intervene to prevent a rise in gold's price. Is there any other conclusion that could possibly be drawn from Mr. Volcker's utterance?

The Reality: A Rising Gold Price Is An Enemy of the State

If we are to believe the words of Mr. Volcker, a rising price of gold is an enemy of the State. Enemies of the state are typically dealt with in harsh terms, no? Is it not true that Iraq and Afghanistan were both invaded because they were deemed to be "enemies of the state"? Extraordinary means can be and often are taken to subvert anything deemed to be an enemy of the state.

Gold is no different.

In times of war, armies are deployed to carry out or exercise the will of the collective ruling elite. Often, these actions are preceded or accompanied by sanctions, or perhaps even less visible covert or "dark" operations which might be aimed at economically destabilizing or toppling a regime - perhaps by coup or maybe without ever firing a shot. These types of operations are often done secretly and/or behind the scenes. If you have any trouble getting your head around the process, just ask Hugo Chavez how it works.

When nations assemble their defenses, volunteers for armed service are generally viewed to be superior combatants to conscripts - for obvious reasons. When a task or perceived threat is too large for one party to handle, alliances are often formed. Geopolitics and money can make strange bedfellows. We would easily recognize military alliances such as NATO or economic alliances such as the European Economic Community [EEC]. These types of alliances have shared or common goals and work toward a common end.

Talk Is Cheap: But Price Action Makes Market Commentary

A man whom I deeply respect is Bill Murphy. Murphy is the Chairman of GATA and he writes a daily column aptly named "Midas" - specifically on the machinations or related inner workings of the gold market. As an ex commodities trader, Murphy intuitively understands that a rising gold price sends signals to different players in the market economy. One way he articulates his understanding of this concept is to constantly state in his daily writings,

"Price action makes market commentary".

Truer words have never been spoken or written. When a given market is advancing, press clippings relating to said market are positive. When a market is stagnant, press is neutral to negative and when a market corrects or "pulls back" - look out.

From an historical perspective, bull markets in physical gold or gold equities can create excitement or even frothy markets. These prices can take off quickly because the 16 mining companies that make up the XAU index [the guts of the gold mining industry] have an underlying or collective market capitalization of only about 116 billion dollars. Owing to the relatively small market cap size of this sector, "melt up" situations that feed on themselves can easily occur. I surmise this is what Mr. Volcker was really referring to when he said, "It was probably a mistake to allow the price of gold to rise so high".

The gold market has had repeated booms and busts throughout history. Since the official end of the Bretton Woods system in August, 1971 when President Nixon closed the gold window, the world has not had a gold backed currency. Many would argue this is why gold has been in such a prolonged 'funk'. Evidence suggests otherwise. Owing to obscenely large money and credit/debt creation within the past ten years it is inconceivable why the price of gold is not dramatically higher today. GATA has proven that the gold price has been suppressed significantly due to Central Banks dishoarding somewhere in the neighborhood of 16,000 tonnes of sovereign gold, physically removing gold from the vaults through lease agreements and forward sales facilitated by bullion banks. Like Enron, Central Bank's accounting for gold has been misleading if not outright deceptive.

Despite this [or perhaps in spite of it, take your pick?] empirical evidence would suggest that lately, the gold price is trying to do some catching up - beginning to rise with authority - sending a signal to market participants. Upon revisiting Mr. Volcker's "it was a mistake" statement, I question the solution he posed. While acknowledging that a "melt up" in the price of gold is detrimental to the existing fiat monetary order, it could be argued that this only occurs due to negligence on the part of Central Bankers overtly by printing too much money or tacitly through loose interest rate policy leading to excessive debt creation.

In this light, if any discipline or remedial action is to be contemplated at all - it should first be aimed at reigning in spendthrift governments through policy aimed at limiting available credit and, hence, money creation. Folks who purchase gold do so to prudently protect themselves from Central Bank/government largess. It begs the question; should one be punished for exercising prudence in their finances?

Who or What Determines What Prudent Measures Are?

In many instances, the investment community relies on ratings agencies - the Moodys, the S & P's and Fitches for Credit Ratings and organizations like the Mercers, Ibbotson's and the like for a determination as to proper or prudent asset allocation. A wide range of other proprietary research outfits offer guidance and coverage on individual stocks and sectors of the economy. When it comes to money creation - this task rests fundamentally with Central Banks.

In the case of sovereign nations, reserve requirements in recent years have consisted almost exclusively of U.S. Dollars and gold with Euros just recently starting to make inroads.

Balancing the amount of fiat currency held versus gold bullion as reserves should have its basis in a number of factors including a given country's current account, aggregate reserves, political stability along with geopolitical concerns to name but a few. These monetary considerations where gold is concerned are increasingly playing a more important role than the traditional propellant of the gold price - namely, jewelry demand. Further, there is a strong argument to be made that we have reached "peak gold" with a global demand/supply deficit having existed for many years. The rate of discoveries versus the rate of depletion suggests this trend will continue for the foreseeable future.

The reckless creation of money and easy credit has created imbalances affectionately known as asset bubbles. These asset bubbles are an alternate manifestation of inflation and the rise in gold's price is a further signal to the market. Consequently, investor interest in bullion and gold shares has been reignited. The signals are unequivocal - and the market has begun voting with its pocket book. The market is rediscovering its traditional "flight to safety trade".

If the rate of increase in the price of gold is allowed to accelerate - as Central Bankers are all too aware - financial disasters are possible. This is a reality - though seldom admitted or articulated by the world's Central Bankers.

The Allied Front Against Gold

To ensure that economic "nature" does not take its course, Central Banks have promulgated a "win at any and all cost" campaign to impinge on gold's price rise - in the face of profligate money printing - for a great many years. The de-basement of the currency has been continuous and is evidenced by the fact that the U.S. Dollar has lost more than 95% of its purchasing power since 1913 - the year the Federal Reserve was formed. The Reagan Administration was the last "good opportunity" that government had to reel in the ever increasing dominance of the Federal Reserve and its march toward ever increasing inflation. In the words of the late, famed Austrian economist, Murray N. Rothbard, when the Reagan-ites came to power,

"There were two fundamental reforms the Reagan Administration could have proposed to end our Age of Inflation. First, either the abolition or the brutal checking of the Fed. Nothing was done, since monetarism wishes to give all power to the Fed and then naïvely urges the Fed to use that power wisely and with self-restraint. Second, the Administration could have followed Reagan's campaign pledge and reinstituted the gold standard. But the Friedmanite monetarists hate gold with a purple passion and wish all power to government fiat money."

Rothbard knew the Monetarists well. The Monetarists are a group of economists so named because of their preoccupation with money and its effects. Perhaps the most famous of the Monetarists is Milton Friedman who developed much of the Monetarist macro economic theory we learn in academia today. In macroeconomics, "Monetarism" under the leadership of Milton Friedman, its best-known advocate - represents the most renowned phase of the Chicago School of Economics.

Two points worth highlighting are:

First, over the past hundred years, American mainstream economic thought has been almost exclusively dominated by two major groups; the Keynesians and the Monetarists:

"For the longest time, Chicago was the only school in America not swept by the Keynesian Revolution ......... But in Friedman's Monetarism, it found a theoretical and empirical means by which to begin rolling back the Keynesian revolution".

While these two competing economic schools of thought could both rightly be accused of intellectual bigotry among the intelligentsia - their deep seated rivalry is rooted in a sense of ownership-via-birthright to calling the economic shots in America.

Secondly, there is a direct relationship between the University of Chicago and the monetarist's doctrine and their disdain for gold. More on this later.

Morning Has Broken.... And The 'Death Star' Aligns Against Gold

Now for a real world example of how ideology meets reality. The following factual account is one that depicts the collision of ideology and the "raters" with the adage that highlights the importance of market commentary. This involves one of my readers sharing a personal/professional experience he recently had in his place of work. Without mentioning his name, he is a senior IT professional at a major Financial Investment firm in Texas that manages approximately 30 billion in assets. And because nobody tells his story better than himself, here's what he had to say:

"Recently, when the Cheuvreux Report came out, I went straight to the chief principal at [my] firm to give him a copy. This guy is the chief stock picker in the firm and his decisions strongly influence the stocks that are bought and sold by the firm. After several days, he contacted me and stated that the report had really stimulated his interest, and are there any gold stock recommendations that I could provide? I thought about it and gave him the tickers HL (Hecla), NEM (Newmont) and AEM (Agnico-Eagle).

I was astonished with what [our] research department communicated to me several days later. You see, not only could our firm not buy any of my PM recommendations, the firm could not buy even a single solitary share of any gold/silver stocks and here is why:

1). Our firm uses Morningstar ratings on stocks and stocks cannot have the lowest rating [one star] to be considered by our firm.

2). Not only did my three recommendations all have the lowest rating (One star)..... every single gold stock with analysis was the lowest rating (One Star) !!!!

3). This was embarrassing to me and so I decided to read into what kind of content was in Morningstar analysis. When reading the analysis in Morningstar about my first pick - HL(Hecla) the text is so negative, if I did not personally know anything about this stock, I would have agreed with rejecting this stock completely. It read like a hopeless and horrible company and I was embarrassed that I even suggested this dog.

4). However, I became suspicious when seeing a target price for Hecla at $2.00, when the current price was $5.25 per share !!!! The author would not recommend buying this stock unless it was in the low one dollar range !!! Outrageous !!!

5). Hecla is admittedly a little speculative, so next I looked next at Newmont. This is a bellwether gold stock and a much more stable choice - Horrible analysis. Target price..... $28.00 when currently price was recently over $60.00. Shocking !!!

6). Agnico-Eagle was even more ridiculous - as far as Target price and buy and sell price recommendations. Were talking about target prices 60% or more than the current price!!!"

Now I'm going to admit, when I first read this - I felt that perhaps someone was over reacting or maybe the stress of his job was getting to the poor man. But, as I have come to learn - when I hear stories like this - particularly regarding gold - flags now go up.

Who's Flag Does Morningstar Really Fly?

If this seems like no big deal, consider the following, as my IT friend points out,

"This may seem like a minor deal, but the chief principal at my firm was not considering buying a few hundred shares. Can you imagine how many millions of dollars of PM sector investment capital is diverted by Morningstar gold trashing? These reports and analysis are the facts that are checked by research departments and powerful investors. What kind of information are they getting? Are all the other rating firms doing the same?"

So, I went to Morningstar's web site at www.morningstar.com - took a two week "free trial" subscription and inputted by industry "Gold & Silver" to see what kind of research would come up? Low and behold, I found that EVERY HUI member that is covered is rated with the lowest Morningstar rating (One Star, or Death Star perhaps?) designation. Reports accompany many of these stocks from "experts". All these reports were very recently written, and in fact - every one I perused was written by a female analyst named Parvathy Krishnan, C.F.A.. Here's a sample of what I found:

Goldcorp GG: NYSE - Today's close: 26.86 - Morningstar Rating: 1 star - Recommendation: Consider buying at 12.70, Consider Selling at 24.10 - Coverage/analysis: dismal - Bus. Risk: Above Average - Economic Moat: None - Mkt. Cap: 5.1 Billion - Analyst: Parvathy Krishnan C.F.A.

Hecla Mining HL: NYSE - Today's close: 5.11 - Morningstar Rating: 1 star - Recommendation: Consider buying at 1.00, Consider selling at 2.50 - Coverage/analysis: dismal - Bus. Risk: Speculative - Economic Moat: None - Mkt. Cap.: 606 million - Analyst: Parvathy Krishnan C.F.A.

Agnico-Eagle AEM: NYSE - Today's close: 25.35 - Morningstar Rating: 1 star - Recommendation: Consider buying at 2.60, Consider selling at 6.10 - Coverage/analysis: dismal - Bus. Risk: Speculative - Economic Moat: None - Mkt. Cap.: 2.18 Billion - Analyst: Parvathy Krishnan C.F.A.

Iamgold IAG: NYSE - Today's close: 8.06 - Morningstar Rating: 1 star - Recommendation: Consider buying at 1.80, Consider selling at 4.30 - Coverage/analysis: dismal - Bus. Risk: Speculative - Economic Moat: None - Mkt. Cap.: 1.17 Billion - Analyst: Parvathy Krishnan C.F.A.

Kinross Gold KGC: NYSE - Today's close: 9.58 - Morningstar Rating: 1 star - Recommendation: Consider buying at 2.50, Consider selling at 4.80 - Coverage/analysis: dismal - Bus. Risk: Above Avg. - Economic Moat: None - Mkt. Cap.: 3.3 Billion - Analyst: Parvathy Krishnan C.F.A.

Meridian Gold MDG: NYSE - Today's close: 24.89 - Morningstar Rating: 1 star - Recommendation: Consider buying at 5.70, Consider selling at 13.50 - Coverage/analysis: dismal - Bus. Risk: Speculative - Economic Moat: None - Mkt. Cap.: 2.48 Billion - Analyst: Parvathy Krishnan C.F.A.

Freeport-McMoRan FCX: NYSE - Today's close: 51.00 - Morningstar Rating: 1 star - Recommendation: Consider buying at 24.20, Consider selling at 45.80 - Coverage/analysis: dismal - Bus. Risk: Above Avg. - Economic Moat: Narrow - Mkt. Cap.: 9.38 Billion - Analyst: Parvathy Krishnan C.F.A.

Newmont Mining NEM: NYSE - Today's close: 48.17 - Morningstar Rating: 1 star - Recommendation: Consider buying at 17.80, Consider selling at 33.80 - Coverage/analysis: dismal - Bus. Risk: Above Avg. - Economic Moat: None - Mkt. Cap.: 21.6 Billion - Analyst: Parvathy Krishnan C.F.A.

Golden Star Res. GSS: AMEX - Today's close: 3.06 - Morningstar Rating: 1 star - Recommendation: Consider buying at 1.30, Consider selling at 3.10 - Coverage/analysis: dismal - Bus. Risk: Speculative - Economic Moat: None - Mkt. Cap.: 437 million - Analyst: Parvathy Krishnan C.F.A.

Glamis Gold GLG: NYSE - Today's close: 27.15 - Morningstar Rating: 1 star - Recommendation: Consider buying at 5.70, Consider selling at 10.90 - Coverage/analysis: dismal - Bus. Risk: Above Avg. - Economic Moat: None - Mkt. Cap.: 3.55 Billion - Analyst: Parvathy Krishnan C.F.A.

Harmony Gold [ADR] HMY: NYSE - Today's close: 13.89 - Morningstar Rating: 1 star - Recommendation: Consider buying at 2.20, Consider selling at 4.20 - Coverage/analysis: dismal - Bus. Risk: Above Avg. - Economic Moat: None - Mkt. Cap.: 5.46 Billion - Analyst: Parvathy Krishnan C.F.A.

Eldorado Gold Corp EGO: AMEX - Today's close: 4.15 - Morningstar Rating: 1 star - Recommendation: Consider buying at .50, Consider selling at 1.20 - Coverage/analysis: dismal - Bus. Risk: Speculative - Economic Moat: None - Mkt. Cap.: 1.1 Billion - Analyst: Parvathy Krishnan C.F.A.

Gold Fields [ADR] GFI: NYSE - Today's close: 19.46 - Morningstar Rating: 1 star - Recommendation: Consider buying at 5.70, Consider selling at 10.90 - Coverage/analysis: dismal - Bus. Risk: Above Avg. - Economic Moat: None - Mkt. Cap.: 9.58 Billion - Analyst: Parvathy Krishnan C.F.A.

Bema Gold BGO: AMEX - Today's close: 4.28 - Morningstar Rating: 1 star - Recommendation: Consider buying at .40, Consider selling at .90 - Coverage/analysis: dismal - Bus. Risk: Speculative - Economic Moat: None - Mkt. Cap.: 1.71 Billion - Analyst: Parvathy Krishnan C.F.A.

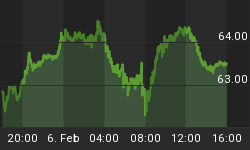

I was attempting to list all 16 of the components of the HUI Index - but I fell short - because I could find no analyst's report for either Coeur D Alene Mines or Randgold Resources. If you happen to work at either of these fine institutions - don't worry - I'm sure Parvathy will get around to smearing you too - as you can see, she's a very busy girl. Coincidentally folks, if any of you happen to be curious - over the past four years - the HUI Index is up somewhere in the magnitude of 400 %. Here's a graphical depiction of what the HUI Index has done over the past few years:

It sure looks like Parvathy has it in for all gold companies, eh? So, just for fun, to see if ole Parvathy had it in her to "rub a little salt in the wounds" - I wanted to get her take on Barrick Gold - only because I've studied the company myself and know them to have the most "toxic hedge book" in the universe. Well, I've got to hand it to her - she didn't disappoint:

Barrick Gold ABX: NYSE - Today's close: 26.18 - Morningstar Rating: 2 stars - Recommendation: Consider buying at 14.00, Consider selling at 26.50 - Coverage/analysis: relatively positive - Bus. Risk: Above Avg. - Economic Moat: None - Mkt. Cap.: 13.96 Billion - Analyst: Parvathy Krishnan C.F.A.

By way of explanation, Economic Moat which Parvathy refers to can be defined as follows:

A figurative term that Warren Buffet coined to refer to the competitive advantage that one company has over other companies in the industry

The wider the moat, the larger and more sustainable the competitive advantage. By having a well-known brand name, pricing power and a large portion of market demand, a company with a wide moat possesses characteristics that act as barriers against other companies wanting to enter into the industry

So folks, in summary - from my examination - not only have I broken into a cold sweat but I have found only one gold mining concern that Morningstar rates high enough for a great many institutional investors to even consider buying - and that one firm happens to be "short" somewhere in the magnitude of 13 million ounces of gold. To put that into perspective, Jim Willie points out,

"..a 13 million oz short position exceeds all gold exchange traded fund (ETF) holdings. In the past six quarters, try imaging the harsh reality of a $1000 million loss for Barrick".

And just for fun here's Barrick's chart:

Now I've got to tell you, having done this research - I've now got bigger questions running through my head. Oh, questions like who is Ms. Parvathy Krishnan C.F.A. anyway? I mean, she works for Morningstar - a renowned ratings agency. Wouldn't you suppose the good folks over at Morningstar would be aware that one of their analysts are "cutting a swath" through one of the hottest sectors of the investment landscape over the past couple of years?

I just had to investigate - figuring of course, there must be more to this than meets the eye.

So, Ripley's Believe It or Not, here's what I turned up - the bios of the executive suite of Morningstar Inc. [listed below] including Chairman and CEO, COO and the five listed members of their board of directors. While it would surely be an act of moral outrage to suggest that everyone who attended university in Chicago was a monetarist - would it really be any more ridiculous than the notion that 100 % of HUI stocks are rated sell? You all can judge that for yourselves - I've seen enough to formulate my own opinion.

Joe Mansueto

Chairman, CEO &

Director

Morningstar, Inc.

Before founding Morningstar, Mansueto was a securities analyst at Harris Associates. He holds a bachelor's degree in business administration from the University of Chicago and a master's degree in business administration from the University ofChicago Graduate School of Business.

Cheryl Francis

Director

Morningstar, Inc.

Cheryl Francis was elected to the board of directors of Morningstar in 2002. She has been vice chairman, Corporate Leadership Center, since 2002 and an independent business and financial advisor since 2000. From 1995 to 2000, she served as executive vice president and chief financial officer for R.R. Donnelley & Sons Company, a print media company. She currently serves as a member of the board of directors of HNI Corporation and Hewitt Associates, as well as a trustee for Cornell University. Francis holds a bachelor's degree from Cornell University and a master's degree in business administration from the University of Chicago Graduate School of Business.

Steve Kaplan

Director

Morningstar, Inc.

Steve Kaplan served as a member of Morningstar's advisory board beginning in 1998 and was elected to the board of directors in 1999. Since 1988, he has been a professor at the University of Chicago Graduate School of Business where he currently is the Neubauer Family Professor of Entrepreneurship and Finance. Kaplan holds a bachelor's degree in applied mathematics and economics from Harvard College and a Ph.D. in business economics from Harvard University. He also serves on the board of trustees of the Columbia Acorn Funds where he serves as a member of the governance and compliance committees.

Paul Sturm

Director

Morningstar, Inc.

Paul Sturm served as a member of Morningstar's advisory board beginning in 1998 and was elected to the board of directors in 1999. Since 1992 he has worked at SmartMoney magazine, where he currently writes a monthly column on investing.

From 1985 to 1989, he was assistant managing editor for BusinessWeek. From 1980 until 1985 he held a similar position at Forbes. Prior to that, Sturm worked as a business writer for a variety of publications based in New York, Washington, and London.

Sturm holds a bachelor's degree in economics from Oberlin College and a master's degree in journalism from Columbia University. He received a law degree from Georgetown University Law Center.

Tao Huang

Chief Operating Officer

Morningstar, Inc.

Tao Huang is chief operating officer of Morningstar, Inc. and responsible for corporate strategy and directing the day-to-day operations of the company.

Huang joined Morningstar in 1990 as a software developer and from 1996 to 1998 served as chief technology officer. From 1998 to 2000, Huang served as senior vice president of business development and head of international operations.

Huang holds a bachelor's degree in computer science from Hunan University in China, a master's degree in computer science from Marquette University, and a master's degree in business administration from the University of Chicago Graduate School of Business.

Don Phillips

Managing Director & Director

Morningstar, Inc.

Don Phillips is a managing director of Morningstar, Inc. and responsible for corporate strategy, research, and corporate communications. He has served on the company's board of directors since August 1999. Phillips joined Morningstar in 1986 as the company's first mutual fund analyst and soon became editor of its flagship publication, Morningstar ® Mutual Funds™, establishing the editorial voice for which the company is best known. Phillips helped to develop the Morningstar Style Box™, the Morningstar Rating™, and other distinctive proprietary Morningstar innovations that have become industry standards. Journalists regularly turn to Phillips for his insight on industry trends. Investment Advisor magazine has named him to its list of the most influential people in the financial planning industry. Financial Planning magazine has named Phillips one of the planning industry's "Movers & Shakers." Registered Rep. has named him one of the investment industry's 10 key players.

Phillips holds a bachelor's degree in English from the University of Texas and a master's degree in American Literature from the University of Chicago.

In case you forgot my earlier ruminations about the Monetarists and the Chicago School of Economics - let's not forget how the late great Murray N. Rothbard explained,

"Friedmanite [Chicago School] monetarists hate gold with a purple passion and wish all power to government fiat money."

For those of you who really think you've never been mugged in Chicago - think again.

It seems to me we've all - at least - been berated!