It's now official: the traditionally no-income asset class including gold, silver and platinum has actually outperformed the major stock market indices every year since 2001. That's five straight years running. But never take your eyes off a charging bull!

Gold is up 23% for the year, silver up more than 45%. But rather than pat ourselves on the back and assume further gains are guaranteed, those of us who saw this phenomenon coming and got involved ought to now look at what lies ahead and determine what 2007 has in store for the precious metals complex. Before we get to that though, let's take a quick look at where we stood a week ago.

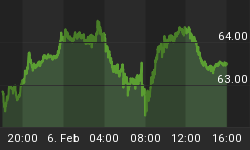

Last week we described "a strong picture that could see the metals continuing to attempt small rallies in the thinner holiday trading ... though profit-taking and consolidation will probably continue through the New Year." Andspecifically we said, "GLD rests more comfortably above support at $615 with plenty of upside potential." The chart below indicates gold clearly bouncing off its support, aggressively taking back the $630 mark.

We called attention last week to the fact that SLV was trading between its 50- and 200-day moving averages, calling these "obvious support and resistance". The chart below shows the silver ETF nestling comfortably into resistance for the yearend.

And last week our rate-hike bias finally saw some vindication in the bond market with priced-in odds of a cut in the first half of 2007 falling to 35% and odds for June 28 cut roughly even. The adequate, if not excess, liquidity evidenced by the equities markets, and now the ECB's M3 data, signal that only a dramatic tailspin into recession could possibly force the Fed to lower interest rates with the dollar under pressure as its recently seen. Of course this means that bond buyers looking for a rate cut next year are probably still too optimistic if economic data continues to support moderate growth and a recovery in housing.

The November 26 Precious Points update titled "Gold and Goldilocks" began to contemplate the possible impact of higher interest rates on precious metals with the observation that, at least in recent history, shifts in interest rate policy tend to create counter-intuitive moves in metals until the transmission effects of the new policy are more or less confirmed. That is, lower rates initially produced cheaper metal in '91 and '92 until the real Fed Funds target rate dipped below zero and Greenspan stopped loosening. The higher rates from 2005 through this past May accompanied higher metals prices because they were not believed to have compensated for the liquidity produced by an entire year of 1% nominal rates.

With Bernanke at the helm, the end of interest rate hikes in May was concurrent with a convincing contraction of overall money supply as measured by M2. Though metals sold off violently at the time, they have retraced much of their earlier gains as the money supply has been allowed to expand with the onset of concern over the housing slowdown. Because the higher rates now exist with a nuanced combination of open market activities, they have yet to produce the stronger dollar and lower metals prices one might expect. The resulting uncertainty about Fed policy, as exhibited at times by contradictory outlooks in the stock and bond markets, is becoming a quixotic hallmark of this transparent, yet flexible Bernanke Fed.

The incremental rise in rates, and the concurrent expansion of monetary supply, also wreaked havoc in long accepted relationships between precious metals, major stock indices, and the dollar and led to some speculation that the dollar and gold were no longer inversely correlated. Though the traditional inverse relationship held true in the later part of the year, it's quite likely that these nontraditional movements linking stocks, the dollar, and precious metals, being functions of the interest rate policy described above, will reemerge in 2007, particularly when the Federal Reserve sends mixed messages between its open market activities and unofficial rhetoric. We also spent some time this year examining the apparent decoupling of gold and oil, only to conclude that crude has become subject to unique supply and demand factors that have temporarily stalled its inevitable appreciation in dollar-denominated value.

Clearly, a number of dynamic economic forces are always at work on precious metals prices, and 2006 saw the emergence of some unique trends that deserve attention going forward. All economic forces are interrelated at some level, from global liquidity and foreign currency reserves to domestic growth and housing inventories, and because of the significant power they represent, the Federal Reserve statements and policy, as well as how these are anticipated and received by market participants, can be an effective gauge of how all market forces converge to act on the prices of gold and silver, which is why they get so much attention here.

We continue to believe that technical analysis provides profound trade setups through the identification of support and resistance levels, with substantial prognostic ability surfacing through the charting of wave counts and patterns in the relatively volatile precious metals markets. My personal bias is that macroeconomic factors, including total money supply and relative value of the dollar, are the catalysts most often fueling the price moves of interest to the largest number of precious metals investors, and is the general content most suited to a weekly update format. Of course, a careful combination of technical, economic and fundamental disciplines is always at the heart of our outlook.

Looking ahead to next year, technically speaking, the precious metals could face some headwinds. As we noted, SLV is now at resistance and gold is up on low volume and still trading in a large triangle from the May highs. We accurately called the recent tops in gold and silver and stated in advance that the subsequent corrections would not develop into anything like the dramatic selloffs we saw in May and September - at least not yet. Most traders and analysts are eyeing a triangle pattern in the short term, but as the charts below suggest, long term channel support favors a return to the lower trend line before another powerful move above last May's highs.

As the long term charts show, the lower trend line can either be reached by a drop in price or from an advance in time. From here then, we would expect metals to remain within a wide range near current levels, possibly with more immediate downside than up, until time brings them back to the rising channels. Interestingly, the charts also reveal that this is the exact scenario that played out in 2004-2005, the period immediately preceding a parabolic ascent. Therefore, traders should take a balanced approach that considers the possibility of a consolidation period in 2007 as a prelude to another period of fantastic gains. We will be evaluating the near term structure in gold and silver to determine whether the lower line of that channel support is an immediate price target or if there is significant resistance farther up to create a horizontal pattern. Also of note is the fact that, platinum, which spiked recently on rumors of a new ETF, closed well off its highs for the year and nearest its multiyear trendline. The chart below suggests that, of the precious metals, platinum can resume its uptrend with the least amount of price and time consolidation.

Talking economics, overall liquidity and uncertainty should act to buoy metals prices near current levels, though some profit-taking after last week would not be unexpected. The bond market still expects the Fed to cut rates next year, and last week's selloff in equities probably indicates that some of the buyers there were expecting the same as well. Protracted multiple contraction will obviously not benefit mining stocks, though the metals themselves could benefit from a reallocation. With virtually no earnings reports scheduled, this week's housing, auto and jobs data, as well as the release of the FOMC minutes, will refocus attention on the health of the economy and interest rates.

Whatever the effect on stocks, further strengthening in the economy will eventually eliminate chances of a rate cut. The effect of the current private equity revolution on interest rate policy and precious metals, though, is not yet known. Superficially, it would seem that the utilization of these funds should take some pressure off the Federal Reserve and strengthen the case for rate hikes. If the Fed raises rates and leaves room for still further hikes, we could continue to assume that liquidity is high and that, as in 2005-2006, precious metals will continue to appreciate in value. While the Fed's rhetoric has created a plausible route for emergency interest rate cuts, with the Euro nipping at the dollar, the ECB poised to raise rates, and with Russia and others threatening the dollar's world reserve status by moving to price oil in local currencies, lower Fed rates seem highly unlikely.

Perhaps the strongest case for metals in 2007 was made by Alan Greenspan, who not only predicted that foreign governments will continue to diversify their currency reserves, creating several more years of dollar weakness, but even called holding reserves in a single currency "imprudent". Even if foreign central banks do not replace dollars with gold, as it now seems one European country may be doing, the pressure on the dollar could actually benefit the U.S. economy.

Week to week, the likelihood of a recession in the U.S. seems to decrease, but, of course, the possibility remains. Much more likely than a full-blown recession, though, is that lower-than-expected GDP growth or corporate earnings, both of which could occur if oil renews its march to $100, prompt the Fed to create additional liquidity without necessarily lowering interest rates. This is another bullish scenario for metals. In fact, the only real threats to metals are sudden world peace or low liquidity, as even the sort of middle-of-the-road, Goldilocks action that's kept the metals largely muted for the last half of this year tends to empower the bullish fundamental supply and demand forces behind precious metals.

Though higher prices have inspired increased mining activity for both gold and silver, new supply has been and is expected to continue being absorbed by new investment and industrial demand. With silver in particular finding more new uses that take the metal permanently off the market, the bullish long-term picture here seems firmly intact. While demand for gold jewelry diminishes severely at prices near the highs earlier this year, commercially viable ore grades are simply becoming difficult to find and miners are increasingly relying on silver and base metal byproducts to maintain their margins. This supply factor alone makes physical precious metal one of the safest investments for the long term and one that is likely to contribute gains to your portfolio for many seasons to come.

Wishing you all the best,