Market Wrap

Week Ending 12/29/06

Economy

December Consumer Confidence rose 3.7 points to 109, the highest reading since 2002. Some claim that the number is responsible for the rise in interest rates that recently occurred, which will be covered in more detail in the bond report below.

Europe reported that their money supply is expanding at the fastest rate in almost 16 years, which has led to speculation that higher European Central Bank interest rate increases are in the wings. M3 was up 9.3% from a year ago the ECB said.

Central banks are still buying US dollars no matter what you hear. Don't listen to what they say - watch what they do.

So far, the discrepancy between the Fed holding off on raising interest rates, while the European Central Bank has not only raised, but alluded to further rate increases, has not yet affected the demand for dollars.

The International Monetary Fund reported that dollars accounted for 65.6% of reserves, up from 65.3% during the prior quarter. However, dollar reserves are down from the year ago rate of 66.3%, and even further below the 72.6% rate of 2001.

In comparison, the Euro has been increasing - but still remains far behind the US dollar. Presently, the Euro accounts for 25% of reserves. Two years ago it accounted for 24%, and in 2001 the figure was just over 19%. So it's use has been growing.

China has the largest reserves of any nation, which now surpass $1 TRILLION. 70% of China's reserves are in US dollars.

Stocks

The Dow was up 1.0% for the week, and 16.3% for the year. The S&P 500 gained 0.5%, and is up 13.6% for the year. The Transports added 1.1%, and are up 8.7% for 2006. The Utilities tacked on another 0.2%, and are up a very respectable 15.8%.

Credit, credit, credit - everywhere you look there is credit: tis the name of the game - the world is afloat on a sea of liquidity that came from nowhere and will hence return, as ashes to ashes - and dust to dust. But where does credit initially settle for awhile: - in markets that need the elixir of life, where fortune is found to be the sibling of strife.

Credit and liquidity have fueled asset inflation around the world. The Dow is up just over 16% for the year; the FTSE 100 is up 10.4%, France's CAC 40 17.5%, Germany's DAX 22.0%, and Spain's IBEX 31.8%. But wait - the party has just begun.

The Shanghai Composite index ended 2006 with a gain of 130%, Vietnam 144.5%, Venezuela's stock market is up 156%, Peru 168%, Botswana 74.2%, Croatia 60.7%, and Russia's RTS Index has increased 221% in the last two year.

Yet the stock markets in the oil rich Middle East have been pummeled to the downside. Saudi Arabia is down 52.5% for the year, Jordan 32.6%, Qatar 35.5%, and the United Arab Emirates 43.3%.

Why the discrepancy between the oil rich nations and the rest of the world? Why are these markets far out performing the US and European established bourses? Is there a message and meaning in all this - or is everything OK, just smile and be happy?

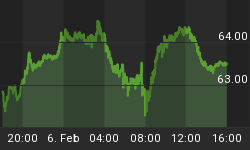

As the following chart of the NYSE Composite shows - everything is looking good. Perhaps a question to consider is when do markets look the most bullish; and when do they look most bearish?

Bonds

For several reasons, we consider the bond market to be of crucial significance due to the fact that bonds move inversely to interest rates. If interest rates rise - bond prices fall. If interest rates fall - bond prices rise. If the bond market trips - unreal estate falls with it.

The Fed does not want to see the yields on the long end of the bond market rise, as that means that mortgage rates would also rise. That in turn would hurt real estate more than it has already been hurt, which would not be a good thing.

Housing or residential investment accounts for 5% to 6% of the economy. Add to that the billions of dollars in home-equity loans that tapped into whatever liquidity they could to keep the music playing, and you can see the reason why household spending has increased even while the private savings rate is non-existent.

No one saves any more - its borrow, borrow, borrow - shop till you drop. Why - because the elite bankers want you to be subservient to them and to keep paying a perpetual and ever-increasing interest rate stream - to them.

It's called Slavery - 21st Century Style - the New World Order of Debt Servitude.

Two-year yields gained 9 bps to 4.81%, and are up 20 bps for the month - which should have every one sitting up and paying attention, but alas - many eyes are diverted away by the many fleeting waifs of the material world.

Five-year yields were up 10 bps to 4.69%, and 10-year Treasuries gained 8 bps to 4.70%. The Long-bond was up 5 bps to 4.81%. The spread between the two-year and the ten-year closed the week out inverted 11 bps.

Interest rates have begun to rise, not just on the short end of the curve - but on the long end as well. The following charts illustrate the point.

We have constantly been repeating that the Fed wanted and would get their coveted inverted yield curve, which they have. They wanted shorter rates higher then longer rates.

Why - because they wanted to make it look like they were actually trying to slow the economy or inflation down - without having a deleterious affect on mortgage rates, and thus upon the housing market: somewhat like M3 - now you see it, now you don't.

A couple of observations: although the Fed got their inverted yield curve, we have always questioned for just how long they would be able to keep it. We repeatedly suggested the possibility that the market may end up raising rates on the long end - regardless of what the Fed or anyone else wants.

Imagine that. Big Ben has nightmares about it, while Sir Alan soaks in his bubble bath to relieve the guilt, and to see up close just what a bubble looks and feels like.

Also, even though the Fed has gotten about as dreamy of a scenario as they could have hoped for via interest rates, the housing and peripheral markets reliant thereon, have taken a bit of a hit. If rates were to really rise there could be trouble in Dodge. We watch with great interest and await the outcome.

Lastly we would add that the market itself may weigh in on the interest rate issue, and if and when the market speaks - even the Fed will pay heed - or suffer the consequences.

This is a lesson we do not think Mr. Bernanke has learned as of yet - but he may soon get a crash course therein.

Currencies

The dollar is down a little over 8% for the year as measured by the dollar index . For the week the dollar lost 0.3% to close at 83.43.

The euro is up 12.6% against the yen, and 11.4% against the dollar this year. Investors are speculating that the ECB will outbid the Federal Reserve and the Bank of Japan in raising interest rates.

The yen fell against 14 of 16 major world currencies this year, which is attributable to its zero bound interest rate policies of the past several years. When it sells cheap - it is cheap.

The pound had its biggest advance since 1990, as it became the world's third most popular reserve currency. Also helping it along was the Bank of England, which raised interest rates to their highest level in five years.

The British pound was up 14% this year against the U.S. dollar, and gained versus 13 of the 16 major world currencies.

Fed Foreign Holdings of Treasury Debt increased $10.0 billion last week to a record $1.75 Trillion. International reserve assets, excluding gold, are up 18.9% to a record $4.81 Trillion. Total global debt jumped 14.1% from 2005 to a record $6.9 TRILLION DOLLARS.

Oil Market

Oil fell again this week, down $1.36 per barrel to close at $61.05. As the chart below shows - it appears that oil is trying to put in a bottom. Time will tell.

Natural Gas prices fell a hard 44% this year, the second worst decline since trading began in 1990. Unleaded Gasoline dropped 5% during the week, and Natural Gas fell 3.8%.

Gold & Silver

Gold closed the week out at $638.00 - up $15.70 or +2.52%. The weekly close was the high for the week.

As the chart below shows, gold has several positive developments going for it. It is above its 50 dma, it has broken out above its upper trend line, RSI is strong, a positive cross over of its 50 dma over and above its 200 dma has occurred, and a positive MACD cross over is pending. Next on the list is the MACD cross and breaking through resistance at $655.50.

Silver

For the week silver was up 0.30 cents to close at $12.94 for a 2.37% gain. As with gold - silver also has several positives going for it.

Of interest is the significance of the RSI 30 level being the past catalyst for the start of substantial rallies.

The chart below shows the past performance in regards to this issue, as well as other positive indicators.

XAU Index

The XAU Index closed up 3.76 points at 142.25 for a gain of +2.71%. The chart below shows a number of positive indicators. Most importantly is that the index remains above the break out of its upper trend line.

Several positive divergences are occurring, and a positive cross over of the 50 and 200 dma is very close to happening.

There still remains several pieces of the puzzle to fall into place:

-

The MA Cross Over

-

A break of the XAU/GOLD Ratio above its upper trend line

-

A positive cross over of the MACD Indicator

-

Resistance at 150 taken out

HUI Index

The HUI Index closed the week at 338.24 - up 10.22 points for a gain of +3.12%. The daily chart shows a mixed bag - some indicators are positive, while others are negative.

Slowly but surely overhead resistance is being worked off, which is good. It takes time, as there is a lot of overhead supply to be chipped away at. There are several positives:

-

Positive 50 dma cross above the 200 dma

-

Positive divergences of RSI, MACD, & Histograms

-

Index sitting right up against its upper trend line which it needs to break back above

A Different View

HUI Weekly

HUI Monthly

The above monthly chart shows a bull market signature of higher highs and higher lows being kept intact.

The gain has been nothing short of spectacular, while the recent correction has been nothing but normal bull market corrective action, which builds strength and staying power for a sustainable and continuing bull market - long into the future.

Stock of The Week

We are going to highlight just one gold stock this week: Kinross Gold Corp. (KGC). Kinross is one of the stocks we hold in our own personal portfolio. Last week we added to our position.

We like the several positive divergences shown on the chart, as well as the positive cross over of the stochastic indicator, and the pending one in the MACD. Once $12.16 is taken out it should be good sailing straight on to morning.

Summary

Interest rates are key - if the long end rises much further there is going to be trouble in paper fiat land, via mortgages and real estate, and all the derivatives and structured finance that no one knows how it will function under fire. Three standard deviations and its all burnt toast.

They've set the pins up - now all that's left is the knocking them down. We wish it wasn't so, but we are afraid it is. It might be a good time to cut back on any form of debt, and to place some savings in gold and silver.

The dollar looks like its ready to fall over the next cliff in its descent into the underworld. The ferryman may not even allow it to cross over to the other side. None of which has been lost to the precious metal markets. The next leg up appears to be close at hand.

Needless to say, the stock market has performed admirably - the Dow is up 16% for the year, a most respectable showing. We still prefer gold and silver stocks - some of which move that much in a couple of week's time.

We can't help but think of those who think "bigger and badder", yet don't carry the idea to its further logical conclusions. If one can be the puppeteer of the world, how hard can it be to play one man? What would you do if you were "bigger and badder".

See the market indicator chart and the gold stock portfolio below. Happy New Year. Good luck. Good trading. Good health. And that's a wrap.

Come visit our new website: Honest Money Gold & Silver Report

And read the Open Letter to Congress