As we mentioned last week, there are numerous factors weighing on the spot price of precious metals and this fact can make it challenging from week to week to say exactly which forces will predominate and determine the next direction the market will take. The forces include sentiment, interest rates, speculative demand, but, of course, the bottom line is money. If you can follow the money, understanding where it's moving and why, then you'll know what's driving the metals markets. The operative words over the last two weeks have been:

"In the short term, if next week's data continue to nourish the sentiment that the economy has rounded the bottom, a veritable soft landing, then metals have a realistic shot at overtaking resistance. The hotter the economy appears to become, the more willingness investors should have to get back into mining stocks and the greater the inflation concerns will become."

With GLD outperforming spot gold this week, and GDX well outperforming the major indices, the road we've been paving here is starting to be traveled. Money was recently piling into stocks as the indices reached record-breaking levels, but now that it's the charts themselves breaking, the precious metals complex is again looking like a good place to put your money.

We also illustrated last week how precious metals seemed to be the major beneficiary of the recent bond market selloff, noting that the strong economy was heating inflation worries, but warned that rallies in gold would be particularly subject to profit-taking and selling on "overbought" technical factors. Of course, in a weekly update you can only get a handle on the prevailing trends, but members in the TTC forums receive daily briefings on relevant news and factors moving the metals market. For example, after recommending that buyers load up on Monday's weakness, the following message was posted to the forum before Tuesday's opening on Wall Street:

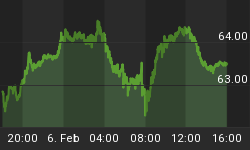

"The news turned negative for the dollar overnight, at least against the euro, but it's probably seen the full extent of its decline for today, so the question becomes whether gold can stay above $638 and GLD above $63.33. Remembering that gold can be reaching near term overbought levels, a move above $645 would be dangerous, but given that inflation concerns are starting to make a comeback as measured by TIPS spreads, and that the market has not yet priced in a rate hike, which is certainly the way the Fed is leaning, i'm starting to watch $650 for some time over the next two weeks. With all it's inflation talk, the fed has been playing right into gold's hands!"

Of course, spot gold made a run towards $650 that very day. When it reversed as the dollar regained lost ground, members were tipped off to expect another near term rally in Wednesday morning's post. If you recall, Wednesday was the day spot gold peaked over $652 intraday.

The relationship we've been tracking between stocks, bonds, and metals, though, was disturbed a bit during Thursday's massive across-the-board selloff, where money seemed to flow out all three markets simultaneously. The biggest move of the week, however, though it probably won't make any headlines, was the jump in 30-year Treasury yields. The move signaled that markets are finally starting to take the Fed at their word and, with the January meeting right around the corner, have started pricing in a possible rate hike.

This interest rate development is particularly important because the economy is probably not as strong as the latest data has led traders to believe. In fact, with interest rates at recent highs, particularly as expressed by the 30-year bonds, there's growing concern the housing market will be unable to work off excess inventory this year as had been hoped. On top of that, there's new numbers out now suggesting that mortgage defaults in housing will continue to escalate over the coming months. These areas of the economy being what they are, it's almost impossible for the Fed to hike rates anytime soon, but the hawkish talk has done more to normalize the yield curve than most probably ever expected. If buyers now rush in to capitalize on the higher yields and return interest rates to more palatable levels for borrowers, the move may siphon dollars away from stocks and metals markets.

Indeed, as the effect of winter weather takes hold and begins to appear in the data, the optimism that led the concurrent rallies in stocks and metals appears to be unwinding. But, as we've been saying, many factors are at work in the metals sector and metals are now gaining strength from oil finally moving higher and from continued uncertainty surrounding what appears to be a potential broadening of the conflict in Iraq. As the gulf widens between public sentiment and the President's ongoing course of action, and with General Petraeus telling Congress this week the situation in Iraq is "dire", the chances of a geopolitical catalyst for precious metals this year, and for a return of the "terror premium" are increasing.

Curious events are also unfolding around the dollar. We had suggested a few months back when Paulson and Bernanke traveled to China that, whatever the stated objectives or conclusions, work was probably being done to secure the future of the greenback. The dollar has had a significant rebound since that time, perhaps culminating in this week's announcement by China's premier that the diversification of its foreign exchange holdings will not hurt the U.S. dollar and will be at least partly focused on increasing domestic consumption. It's a very nice sentiment for the premier to express, but with the specifics of the plan yet to be released, it's easy to conclude that diversification is diversification and will ultimately mean a drag on the U.S. dollar. Since the announcement, we've already seen the dollar reach fourteen year lows against the pound, which is rapidly becoming the central banker's new reserve currency of choice. While the dollar is likely to remain stable generally, this week's rebound against the Euro had more to do with swelling monetary supply of that foreign currency than any inherent strength in the greenback.

Unlike the dollar, the fundamentals for precious metals are bullish so that having the other relevant forces in balance produces a gentle, sustainable upward slope of rising value over time. Whatever the motivating cause, it's an unbalance of these forces that makes money move quickly into the sector at higher and higher prices, producing spikes and crashes. And so while this week brought our rally into the territory of $650 gold, the fact remains that, above this psychological level, gold starts to make headlines and physical demand starts to flag. With bond yields rising and the Fed looming, no one but the metals bulls want to hear about $700 gold right now. Though $700 is still an eventual upside target, a kind of move beyond that in the short term will require a powerful catalyst to produce a voracious speculative appetite for metals that's been unseen since last April, when GLD and IAU were pegged to physical prices. It's possible some of the divergence can be explained by fluctuations in the value of the ETF baskets due to lease or storage rates, though, since this exact variation is difficult to calculate and hardly common knowledge, it's unlikely the principle cause.

Until Thursday, the markets seemed to be trading on the questionable notion that a strong economy would produce greater demand for precious metals as it has clearly been doing for steel. If some of the heat comes out of the economy very soon and lowers treasury yields, then it's possible that a return to that logic would see gold and silver suffer as a result. While $600, or just below, is the key support level, ideally, $640-$650 range will hold over the next week as gold continues to trend sideways toward the multiyear trendline we presented earlier in the month. But, if any of the numerous bullish factors kick up a little dust, and the picture looks bleaker than a mild slowdown so that fast money finds itself looking for a safehaven, metals will probably receive the benefit. The charts below show both metals ETFs well above support, with GLD very near to resistance but SLV having plenty of room to extend before the next major obstacle.

To keep up with the evolving market forces described here, follow the money with us, up to the Fed meeting and beyond, in the TTC forums, where monthly membership costs less than 1/10 oz gold or a 10 oz bar of silver -- one of the best values on the web!