- Section I: Gold Market Update; Something's happening here, but what it is, ain't exactly clear

- Section II: The Great Productivity Debate; Greenspan versus Gordon

- Section III:A very short controversy

THE UPDATE

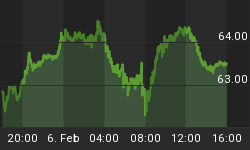

Up until recently, last week would have typically been a bad one for Gold. It began exactly one week after June Gold first spiked back to resistance at $296, and followed a week that saw prices drift slightly lower, developing a flag pattern on the chart. Though normally a bullish pattern, in the Gold market it has historically resolved in a steep decline on a complete disintegration of confidence. Last week, however, was not a subtle departure from the norm. Something IS happening here. The rollover into the August contract was not only smooth, but also bullish. Normally, the old contract would rally and the new contract would fall, reflecting the rollover of net short positions. Last week, however, the reverse occurred, further bearing out the greater bullish conviction in the market, even while we approach the psychologically important $300 mark.

It has been an interesting month so far, with rumors flying about Chinese Gold buying on the COMEX; a last minute triple witching sell off in the Dow Industrials Friday, as traders saw no sign of a single 401K buyer anywhere in sight; missing and then reappearing US Department of Energy hard drives (with nuclear techno secrets on them?); new highs in global Crude Oil prices on the surprising epiphany that Oil producers everywhere are actually already running at or near full capacity; a shocking revelation about the true nature of this stock market rifled through our TV sets last week when 120 indictments were made involving the manipulation of 19 stocks (among the accused are five of the most powerful mob families on the east coast); Joe Kernan admitted that higher interest rates and inverted yield curves are (get this) bad for bank stocks; earnings reports for leading bank stocks revealed that banks don't only invest in mortgages; and both George Soros and Henry Kaufman made surprise appearances on tout TV in what seemed like an attempt to diffuse the growing market anxiety.

However, by far the most significant signs of change were apparent in the Gold and currency markets, and it all started on the day of the weak employment report (June 2nd), or did it? After all, the real break in the dollar occurred on the Monday (May 29th) of that week, and do you know what happened right in between? Mr. Greenspan met with the Bank of England's Eddie George, the European Central Bank President, Wim Duisenberg, and a representative from the Bank of Japan in a closed door secret "Parisian" meeting, in front of over 100 CEO's from the world's largest private banking titans. The location is an irony that café members at le metropole will appreciate.

Nobody yet understands the significance of that meeting "behind closed doors" in Paris, but it was obviously important. This was the largest assemblage of bankers that I have ever seen; yet there was not a peep about it in the press. I think it was Reuters that quoted one "anonymous" banker as saying that there wasn't any significant information to even "phone any of my dealers with."

If that is so, then why the secrecy behind closed doors? If it was simply an exercise in academia, some members of the public might have been interested. It might have even made for good press. Anyhow, all we really know for sure is that the most powerful men on the planet met behind closed doors, and nothing of significance was said! Actually, this whole thing smells as if a very important briefing on upcoming events was disclosed in there, and perhaps the decisively more bullish action in Gold prices so far this month bears that out better than anything else.

So much for Rand…

Arguably, the most important economic debate of the century took place last Tuesday, and pitted the 60-page research of Mr. Robert J. Gordon, from Northwestern University, against the Oracle of funny money himself, Mr. Alan Greenspan. I have, on more than a rare occasion, studied Mr. Greenspan's written testimonies and speeches. Over the years, his conservatism and intelligence has been mistaken for obsolescence, and the business community, for relying on older economic models to manage monetary policy, has publicly chastised him. Consequently, he may have over-compensated on his conservatism, and hence, his new era open mind seems to have affected his well-regarded objectivism. They played him just right. In my estimation, his arguments have increasingly come to rely on a leap of faith in the macro economic implications of the new economy, and are based mostly on anecdotal experience. Perhaps he is hoping to find justification for his increasingly visible mishandling of US monetary policy, though we should not judge him to harshly because the monetary system is flawed in the first place. Nevertheless, his recent gradualism and notoriously hasty aspiration to assert the FED, as a "lender of last resort," is responsible for allowing the (credit driven) speculative forces to get out of control in the first place. To be sure, this might well have happened to the best of us, but that isn't the point.

The point is, arguably, that in the process, he has forced himself to embrace New Economy 101 - a (bullish) Discussion on Productivity Theory, in order to justify his oversights with respect to monetary policy. The importance of the productivity issue cannot be underestimated, for today's stock market prices discount a very bullish conclusion. As a result, I am going to attempt to do the impossible - to decipher the economic argument contained within his speech last Tuesday, and compare it to Mr. Robert Gordon's research, in order to draw attention to this point.

But first, back to the market…

In the context of a global central banking system that is saturated in dollars, George Soros' recent criticism of the ECB's interest rate hike was interesting. He charged that raising interest rates to support the Euro was a mistake, and that they should intervene directly in foreign exchange markets to buy Euros instead. The advice is not necessarily bad, but it is moot. What he is saying is that the ECB should control the money supply directly rather than simply create the incentive for markets to correct these imbalances themselves. What he is also saying is that the ECB should sell some dollars. Perhaps he is sincere in his advice, believing that higher European interest rates will only accelerate a dollar collapse. Perhaps, though, Soros has recognized the opportunity that might present itself if he could bully the ECB into starting something in currency markets. It is not inconceivable that the situation in the Gold market is exactly as extreme in one direction as is the situation in the dollar market in the opposite direction. If that is the case, it is my experience that it takes little effort to catalyze the forces, which are perhaps already set to explode.

On that note, Mr. Doug Noland1 makes a compelling case for the unstable nature, and of the reflexive relationship that has revealed itself, between growth in the derivatives industry and growth in overall systemic financial risk. Noland intelligibly explains why the initial gradual growth in the use of derivatives has accelerated. Roughly interpreted; flawed, but generally accepted hedge models (such as VAR), when applied to portfolio insurance, have (through their tentative success) created a false sense of security in financial circles. This has simply created the incentive to take on even more risk, since it has become perceived that it is possible to manage all of this risk now. The result is an explosion in the uses of derivatives, mostly speculative. The conclusion, of course, is that now there is tremendous systemic risk in the financial system, and the realization is growing that no one has yet (stress) tested these models against the increasingly volatile nature of financial markets.

Now that US stock markets have run into a wall, and judging by the number of concerned commentaries about derivatives that I've recently read, there is some obvious concern about the potentially forced unwinding of some these complex insurance programs. Furthermore, the money spigot has been drying up, and every cent is trapped on the same side of this paper pyramid, or so it would seem by glancing at the level of stock market permeation within US society and abroad:

- Exhibit A, recent liquidity spreads in credit markets;

- Exhibit B, the level of Dollar reserves that global banks hold;

- Exhibit C, bullish consensus trends;

- Exhibit D, etc, etc.

The writing is on the wall. The stock market faces the unwinding of its own speculative excesses, and the models upon which a $5 Trillion derivatives industry is supported are perhaps about to face their first real stress test. If they do not hold up, it may be a revealing look at what proportion of today's risk premiums properly reflect the risk in US assets, and which proportion is simply delusional.

It is, of course, my belief that they are mostly delusional. Someone, who has more time than me, ought to develop a labor index, which measures the extent of the labor force employed or affected by non-viable public companies.2 Perhaps then we can begin to get a sense of the actual delusion?

The market's FED focus is a mistake

In light of the speed with which information is readily available to use today, it is amazing that everyone's focus is still so much on the FED today. It was fifteen months ago when I first informed my clients that there was going to be about about the time of formation of what looks like a left shoulder (unconfirmed pattern) on the three-year DJIA chart on the previous page. From there the question became, what level of interest rates would finally stop this thing? Historical relationships were moot because there was little historical precedent for such high expectations in equity returns going forward.

In hindsight, of course, it seems that the poorer performance in the broad market over the past fifteen months or so, began to gradually weigh on investor psychology, yet the liquidity needs of the narrowing, but ever hungry, tech-market kept sucking every last bit of liquidity out of the global financial system. Still, the market has generally deteriorated, internally, over the past year. The media finally began to broadcast the stocks vs. yields relationship, by the fourth quarter, 1999. It must have been by pure coincidence (undoubtedly), that the Treasury decided on loudly announcing its intentions; to buy back long dated treasuries on the premise that their surplus tax revenues were going to stay a surplus for a decade, or ever more. Unwittingly, this inverted the yield curve, and foiled their plan. It created a disturbance in yield curve related hedges at the same moment that Mr. Greenspan was trying to drain excess Y2K reserves out of the banking system, and rein in wealth effect dependent demand. I believe that this move by the Treasury was their hasty response to recognizing the rapidly changing circumstances. Still, this whole corrective process has only begun.

Yet, just as the game has already changed, Wall Street bulls think that they should focus even harder on FED policy, since their whipping by tighter monetary conditions prevailed after all. The lesson that should have been learnt is to "never fight the FED," but it hasn't. Stock bulls are waiting for the first sign of easing to suck more liquidity into this paper trap. Since this would likely be a stimulus to the economy, than not, it is clearly a sign of arrogance, if not ignorance, as the current direction of FED policy will not generally reverse until much more economic capacity is freed up in the US. Hence, the game is no longer one about the FED. It is about the condition of the market, and how it will affect the economy on the way down. The simple fact is that the technical condition of the market began to deteriorate even into the New Year, which is six months ago now. In order for this to resolve bullishly, the market has to broaden out, the link between the stock market and the economy needs to be (at least) wounded, earnings have to wash out from the capital gains influence, and the "correction" has to be more severe than anything we've seen in the past three years. Remember that corrections exist to purge excess and test bullish hypotheses, neither of which has completely run its course yet.

Of course, the typical pace with which these revelations have become obvious to the media, and therefore the average investor, means that the investing public won't know what's going on for another nine months or so, which is too bad for the next President.

So if the market is so efficient, why is there such a slow adjustment to reality? The answer partly lies with how long it takes a consensus to build in such a volatile environment, but it also partly lies in our vested interest in equities today. If you own a tech stock that is down 50% suddenly, are you likely to persuade yourself to sell it or to hold on to it. Since most people (in my experience) would choose the hold option, they obviously have already made up a reason to do so that doesn't reveal (to themselves) their ego's refusal to take the loss. In other words, investors become ever greater believers (hopers) at the initial stages of a primary bear market...

What does this have to do with the dollar and Gold?

Ok, so the stock market falls and the economy falls. Why would the dollar fall, especially since the rest of the world economy is still dependent on US consumption? The main answers to that question kick off a 60-year-old tale, at about the time when this whole game (the dollar based international monetary system) began. This game has been going on for a long time now, ebbing and flowing as would normally be expected, but the way we have kept it going so far has been by inventing new "made in USA" investment vehicles for the Euros and Asians to buy with their extra dollar holdings. As you may already know, the international dollar system was officially kicked off with a hook and a crook. President Nixon chose to refuse the calls on US gold in the seventies, forcing foreigners to "keep" this capital in the United States or collapse Bretton Woods. Ever since then, this quandary has turned into a game of keeping dollars from being repatriated, by whatever means necessary.

Prior to this decade, deficit spending, by virtue of crowding out international credit markets with US dollar denominated issues of Treasury debt securities, actually accomplished this, believe it or not. That, however, ran into disrepute because it produced outsized public obligations. Luckily, or perhaps planned, for the Clinton administration, the US stock market has outgrown and outperformed the international credit markets anyway, giving foreigners a more exciting, alternative option for their dollar holdings. However, now that inflation seems to have arrived on the horizon again, that the public/private debt has grown to unsustainable levels, and with the stock market appearing like the leaning tower of Pisa resting atop a sky-high paper pyramid, why on earth would anyone want to keep their excess financial assets in dollars? Perhaps Treasury bonds would be a good place for those dollars? Only if you believe that the balanced budget won't derail when the government's surplus capital gains tax revenues disappear, and only if you believe that the US economy will experience a soft landing, which of course warrants a big leap of faith that today's economic imbalances don't need to be unwound.

Don't forget that this is an important election year

In the context of reflexive relationships3 we cannot exclude politics, since any bias in economic expectation sets obviously reflects directly in policy, and therefore has a substantial influence on financial markets. Certainly, the Treasury's bond market play is a result of its perceptions, however misguided they may be. Support for China's trade status comes in complete disregard to their human rights violations, but perhaps it comes as a result of political perceptions tied to their growing economic clout. Before discussing Mr. Greenspan's speech, it might be worthwhile to consider what his political persuasion might be, as he will be a central figure leading up to the election.

Whether a democrat or republican, it is in the democratic interest that financial markets stay sedate (not go down) for as long as possible, while it is in the Republican interest that the markets crumble sooner rather than later. That is because, if they collapse anywhere around an election campaign that is being led by the Republicans, it may suddenly become interpreted as fear of the new incumbent. If they crumble before summer, when the campaign is still only simmering, it would clearly be to the advantage of the Republicans. As you can see, timing is everything. Whatever happens, we are surely about to find out Mr. Greenspan's political persuasion. The moment of truth will be decided in his actions (or inactions) over the next six months or so.

The GREAT PRODUCTIVITY DEBATE

The issue of productivity cannot be understated; for it is inarguably at the heart of this great US bull market. Ultimately, whether the numbers are true or not, might mean the difference between another plateau and the beginning of a financial retribution of disproportionate size. The stakes are enormous, but guess what folks, they still don't really know how to measure the damn thing. On May 1, 2000, Mr. Robert J. Gordon, an economist at Northwestern University, raised doubts about the validity of the recent productivity gains that Wall Street has championed, in a paper titled, "Does the New Economy Measure up to the Great Inventions of the Past?"4 Unfortunately, this paper is sixty pages long, so it makes for a serious study, but a worthwhile one because the author has attempted to answer the question that even Mr. Greenspan has avoided for so long - how much "real" productivity growth is out there?

The report must have stirred not a few defensive emotions, for perhaps coincidentally, Mr. Greenspan gave a speech six weeks later, on the similar subject of Business Data Analysis5 (a productivity discourse) before The New York Association for Business Economics, via videoconference; June 13, 2000 - the discourse centered on the thorny issue of measuring productivity more accurately. In fact, it seemed as if Mr. Greenspan was debating Mr. Gordon's research, point by point. Ah heck, that could be a coincidence too. These coincidences get in the way of a good conspiracy don't they? All in all, however, I found Mr. Gordon's conclusions to be far more convincing, and far less ambiguous, if only by virtue of their better statistical support. The work is extensive, scientific, and spans our economic history from 1860 to the present. That's a hard act to follow.

My goal, then, is to criticize Greenspan's objectivism (or lack of it). His main hypothesis is that by disaggregating the macro data and focusing on the individual sectors (in this case, the corporate nonfinancial sector) that show the best performance (the sum of the parts is greater than the whole argument…or is that bottom up analysis), there should be better representation of the aggregate. Pretty bullish, huh? Mr. Gordon also dissects and statistically separates the individual sectors, and additionally, attempts to quantify the difference between the "cyclical" contribution to productivity and the "structural" contribution to "trend growth." However, he does not conclude that the corporate nonfinancial sector is a better representation of the aggregate, as his adversary does, but perhaps an unsustainable over-representation in the aggregate, benefiting through faster multi-factor productivity (MFP) growth in the durables sectors.

Both economists (coincidentally I'm sure) separated the nonfarm business sector into three - nonfinancial corporate, financial corporate, and noncorporate - generally distinct sectors. Both generally chose to eliminate the two sectors - financial corporate and noncorporate - which have the most controversial influence (or lack of), and to focus then, on the sector - nonfinancial corporate - which has the largest statistical representation in the entire nonfarm business sector (70%) anyway. Although, Mr. Gordon actually did attempt to measure the productivity gains in the noncorporate (or service) sector, and came away with some elaborate insights about the role of productivity in this mostly "intermediate" sector of the economy.

Noting that the non reversing, but widening statistical discrepancy in favor of the national income accounts over the national product figures, since 1992, Mr. Greenspan concludes that "This difference is reflected directly in faster growth of productivity measured on the income side than that measured on the product side of the accounts." In other words, he bullishly believes that the National Income accounts better reflect the productivity influence. To this degree, his judgment call may not be wrong, because the National Product accounts may well better explain the dynamics of consumption patterns. I have to agree with his choice. However, these discrepancies can just as easily be explained in other, less optimistic ways as well, and until other influences are washed out of the data, there is just not enough of a time series to support the true validity of Greenspan's choice.

Theoretically, Productivity equals the real growth rate in incomes per hour divided by the growth rate in the unit costs of the labor input. Still, however, these individual data "inputs" cannot accurately exclude the influence of other macro developments. For example, how much of the influence on prices (the inflation rate) has resulted from a strongly rising dollar and a slack global economic environment? Are not unit labor costs understated if they do not reflect the growing use of stock options, or remuneration other than the traditional wage? Is perhaps corporate profitability overstated if the stock market itself contributes to earnings and increasingly finances the burden of wages? Furthermore, how can we properly account for the difference between a cyclical and a structural influence on the productivity inferences made, until the numbers are measured from the trough of the last business cycle to the trough of this one? Hence, the real truth on this issue will not be understood for at least a few years.

Until questions like this are answered, none of the data inputs used to measure productivity are reliable and the real issue, therefore, remains unresolved (one of the reasons that I favor Mr. Gordon's 140-year time span). In fact, Mr. Greenspan shrewdly avoids this issue by saying, "Domestic operating profit margins, rising as they did from 1995 into 1997 in an environment of falling inflation, necessarily implied falling rates of total unit cost increases - most credibly the consequence of rising productivity growth." "Most credibly?" Sure Uncle Al, that's right, and millions of investors, all on the same playing field, simply couldn't be wrong either.

But I suppose that I should have a little more faith in our leader's judgment, for he certainly has no incentive to rationalize his deliberate gradualist posture on monetary policy, even while confronted with an eye-catching global stock market bubble. To be sure, he sort of qualifies his above statement by quoting one of his 'on the other hand' arguments where he admits to the potential influence from the "Substantial increases in US capital investment…" relative to labor input. This process he terms "Capital Deepening," but concludes that these influences are very difficult to quantify. It seems that any time something gets a little too hard to quantify, like the money supply; you just have to keep rolling with the punches.

In true scientific form, it seems that Mr. Greenspan must have spent considerable time studying the microeconomic level of business activity as he indicates by, every so often, pointing to his real life, day-to-day experiences as if he were a schoolboy forced to improvise because he didn't quite complete his presentation. Yet he asserts that the productivity numbers still understate the bullish acceleration in macro productivity. This is in sharp contrast to Robert Gordon's view that the productivity numbers overstate reality. Likewise, Mr. Greenspan's judgment call, that "The effect of these technologies could rival and arguably even surpass the impact the telegraph had prior to, and just after, the Civil War," is in sharp contrast to Mr. Gordon's conclusion, which argues that the aggregate quantifiable benefit to society of the Internet is marginal, as compared to the telegraph, because consumers are only switching from one large medium to another.

The invention of the telegraph allowed a sudden explosion in communication capacity because it represented the discovery of the original "medium." Mr. Gordon calls this a "first-order invention. In fact, Mr. Gordon suggests that the golden age of US productivity growth followed what is called the second industrial revolution, in 1860-1900, which yielded a cluster of genuinely paradigm-shifting, "first-order" inventions: electric power, the internal combustion engine, modern industrial chemistry and telecommunications. These were all inventions of entirely new things. The Internet, on the other hand, is merely a substitute for some of these first order inventions, rather than a new paradigm as such.

Still, Mr. Greenspan uses a very bullish report, recently prepared (read; 'quickly' prepared) by FED staff, to support his case, and even admits that it reconciles with his own anecdotal account (as if he were a standard of comparison). He argues that the whole idea of productivity gain, is that it is supposed to reduce the amount of total hours that we work, but instead, the "labor resources freed up by technical advance have found ready opportunities elsewhere." Here, I have to interject, because almost certainly, these "labor resources" are pursuing mostly 'financial' endeavors related to stock market speculation these days, and simply observing the enormous amount of growth in the financial sector can corroborate this (mis) allocation of labor. I do not doubt that they "have found ready opportunities elsewhere." However, I prefer to call it an asset-inflation induced misallocation of labor, and like any inflation induced misallocation of resources, there is a point when delirium sets in. But how do we know that so much of this "freed labor" has actually been misappropriated?

I am sure that this may be quantified, but I see no need to go beyond the anecdotal evidence if nobody else will. I have seen enough of a sample of new companies, which survival is purely dependent on the kindness of Wall Street (fleeting though it may be), which also employ many of my friends, and which have been using increasingly weaker assumptions for their business models. Based upon the anecdotal evidence, therefore, ours has progressively more become a stock market economy, where it is the stock market's job to fund anything that the vested masses would like it to. So there you have it. A not insignificant amount of the recently "freed" labor force is highly likely to be in the direct, or indirect, employ of any one of a dozen public companies that are using fly by the seat of their pants, non-viable, business models, financed by Wall Street and the very generous nature of the FED, the fickle yet record appetite of foreign investors, and arguably, your future. No wonder Greenspan has resorted to rationalizations. I wonder when we will be told that it is illegal to sell stock, and when we will be forced to buy more of their bonds? Well anyway, through poorer savings and consumption habits, we have shown our arrogance for the value money.

In other words, the marginal utility of the dollar as a store of wealth may have already started to decline and has been so far offset by the bullish impact that "the velocity of its circulation" must have on its value as a medium of exchange…Ed Bugos

Back to the debate…

Mr. Greenspan further observes that the rapid growth in Information Technology coincident with the development of ever more innovative financial markets, over the decade, has resulted in a more efficient invisible hand, as "The resulting process (resulting from the process of "creative destruction," where capital moves faster from failed technologies to ones at the cutting edge) of capital reallocation across the economy has been assisted by a significant unbundling of risks in capital markets."

Whoa, what a bullish conclusion. How a financial system, which has experienced an extended period of asset "inflation," can work efficiently puzzles me. Inflation, by its very nature, is a distorting influence on an economy. Why is that different for asset prices? In the American textbook of economics, asset inflation is considered a symbol of prosperity. That is why. It is only everywhere else in the world; especially where bubble economics has already visited, that asset inflation is identified as a destabilizing force. The reason is that the "Dollar System" acts as a disciplinary standard for every one else, but there is nothing to act as a disciplinary standard for the Dollar, as you can see from Greenspan's unaccountable leap of faith in the new economy.

Henry Kaufman, on CNBC last Thursday, said that the stock market has caused lots of problems for monetary policy. I think that it is the other way around. There is no discipline for US monetary policy, and hence, for the dollar. Arguably, that's why we have this (stock market) problem (unwittingly caused by monetary policy) in the first place.

In his paper, Mr. Gordon argues that the invention of the Internet (actually invented in the seventies for the Government's own internal use) has not boosted the growth in the demand for computers, which he asserts can be explained by the same unit-elastic response to the decline in computer prices as existed prior to 1995. He acknowledges that the Internet provides information and entertainment more cheaply, but much of its use involves substitution of existing activities from one medium to another. However, I must admit that his explanation downplays the significant time saved in the pursuit of raw research materials, technological development, and better communications options. He correctly ascertains that much Internet activity involves the defense of market share by existing bricks and mortar companies from rising stars like Amazon, in my view a productive use of the Internet only if Amazon had a viable business model to turn them into a "real" business entity. Finally, he notes what all of us already know. That is, in practice, the Internet is a great time waster, not time saver, because of how many employees use it during work time to monitor, or trade, their stock market accounts, and to do their online shopping during work hours. According to studies6 done this year, Internet traffic for consumer-oriented and financial-trading websites peaks during the middle of the day, not in the evening when people are at home.

I have two important points to add. First, the cyclical component of productivity may be unusually exaggerated, on account of the outsized contribution that stock market gains alone have made to total output (the national income/product accounts) from 1995 to the present. Second, the force of the Internet tends toward zero profitability, because in some industries it can actually eliminate barriers to entry and encourage more competition. Consider the possible hypothesis that at some lower level of general profitability, a monopoly may be necessary to preserve the current infrastructure, whose ongoing development is at least partly dependent on non-ever-profitable organizations. In fact, perhaps the Internet is really a natural monopoly, something else that we probably won't know for years. Certainly, the Internet will lay the foundation for an outsized productivity boost someday, but it first needs to be built, organized, and harnessed. Then, just as we are today reaping the productivity gains of IBM's invention of the PC over two decades ago, we will someday get somewhere using the Internet, provided that we build the darn thing right. I see it as a means, not an end.

Nearing the end of his speech, Mr. Greenspan appropriately praises the many benefits to the business community of all of this technology, much of which is undeniably true. However, allow me to clarify that there are really two major, but very separate, issues that are important here - the socioeconomic importance of technological innovation and the quality of the financial system - which Mr. Greenspan insists on combining into one story. His understandably zealous aspiration to seek a better measure and/or understanding of the technological productivity influence on the economy has resulted in a bullish bias (probably because it is largely based on anecdotal observation), which itself has elevated the perceived present value of the technology revolution. A convenient principle, which perhaps helps to justify the compromises he has had to make in monetary policy.

When Greenspan observes that all in all, there is a reduction in the "degree of uncertainty and, hence, risk," he of course is talking on a micro level again (i.e. Anecdotally), where decision-making has arguably improved with the monumental improvement in information technologies. What he is refusing to acknowledge, however, is that this risk seems to have been shifted to the macro level of the financial system, which is directly under his supervision. Dangerously, however, the evidence suggests that he may come to believe that the oversight in policy was necessary, in order to create this whole technology revolution in the first place. What Mr. Greenspan refuses to acknowledge on this topic, is that due to the multiple factors (MFP) influencing the productivity record at any one point in time, structural (or permanent) changes cannot be measured either in the moment, or from trough to peak. They have to be measured from trough to trough, or from peak to peak, if you want to eliminate the effect of business cycles.

I cannot resist this. On closing, Mr. Greenspan gives the biotechnology sector a decent tout as he says, "The dramatic advances in biotechnology, for example, are significantly increasing a broad range of productivity expanding efforts in areas from agriculture to medicine." Hmmm…didn't Soros give a similar tout on CNBC recently? We'll see how we use all of this technology (knowledge) when the macro financial pendulum swings back the other way and knocks us right on our asses. He remarks that "some of the increase in output per hour may well reflect cyclical rather than structural changes," but then tramples all over that with "the evidence of a decided improvement in the growth rate of structural productivity from the macro data has continued to strengthen." I thought the macro data overstated the figures? I guess he must be thinking anecdotally again.

So, with all due respect to both men, please tell, which of these two gentlemen is the promoter, and which is the scientist? When you've answered that, ask yourself this; have you ever met a promoter whose job it is to preserve your capital?

And finally, a VERY SHORT CONTROVERSY

For a little controversy, what do you think the odds are that the glory of Gold will rise again, and that the Government will own the Internet? Sounds crazy doesn't it? The funny thing is that we may choose both realities ourselves! But that's a topic for another day. Wouldn't it be a howl though, in light of all the fuss and speculation in highway stocks today?

1 Author of the "Credit Bubble Bulletin," a PrudentBear publication.

2 A criterion for what constitutes a non-viable public entity would have to be established, but that would not be difficult. You would not include private companies, as they have to be viable in order to survive, which makes the calculation easier. All you would need to do is to sum the number of employees that work for these companies, and make an adjustment (perhaps a multiplier of some kind) that reflects the stimulated indirect employment in the government and other industries, etc.

3 A concept developed by George Soros in his classic, "Alchemy of Finance."

4 For your reference, see the June 18th issue of The Economist, or you can find Robert Gordon's 60-page document online at Northwestern University

5 You may find a copy of Greenspan's speech at the Board of Governors of the Federal Reserve System website.

6 Undeniably a vague reference to the exact comment made by the author of the Economist article about this topic.