My first post on my brand new blog about 6 momths ago started with a warning about the commercial real estate market and obscenely low cap rates. A few months later I revisited the topic with a couple of anecdotal posts...

- Will the commercial real estate market fall? Of course it will.

- Do you remember when I said Commercial Real Estate was sure to fall?

I then noticed how the mainstream media and blogs started to catch on...

Then I decided to share my proprietary research on a particular REIT and its market...

- The Commercial Real Estate Crash Cometh, and I know who is leading the way!

- Generally Negative Growth in General Growth Properties - GGP Part II

- General Growth Properties & the Commercial Real Estate Crash, pt III - The Story Gets Worse

- More on GGP: A Granular View of Insider Selling and Lease Rate Growth

- GGP part 5 - The Comprehensive Analysis is finally here

- My Response to the GGP Press Release, which seems to respond to blogs...

- For those who were wondering what sparked that silly press release from GGP...

- GGP: Foreclosure vs Asset Sale

- GGP Refinancing Sensitvity Analysis

- GGP part 7 - Share value under the foreclosure analysis

- GGP part 8 - The Final Anaysis: fire sale of prime properties

It appears that now, the price movement in CRE and CMBS is unmistakeably negative. To begin with, it takes money to buy buildings and when you buy buildings you increase demand which drives prices up. This has happened fervently for the last four or five years, driving prices high and cap rates low. So, what happens when you can't find the money to buy the buildings anymore? I'm an equity/real estate guy, but I do look around and ask questions on the fixed income side every now and then.

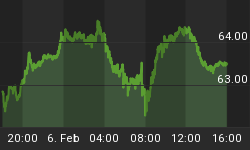

Below is a chart of the AAA cmbs index. The spread is out to around +280. I am told that these are around a seven year duration security, with each 100 bps eqauting to about 7 points (very roughly). This index was +80 one year ago, and +280 is a loss of around 15 points off of par (100).

Additionally this is the top of the heap in terms of quality.

This is the A rated stuff. This equates to $55 - $60 dollar price according to the bond traders. Think about it, and investment grade security losing that much of its value.

I looked at teh BBB and BB charts at markti.com and they look so steep as to be unreal.

The GGP links above in the beginning of this post are well researched and should make very clear where the underlying is headed. GGP is not the only REIT/investor in a bind. So who has this stuff on their books? See Bear Stearns, Morgan Stanley, Ambac and MBIA - to start with. In the case of Bear Stearns:

Deal Type | Min Rating | Total |

CMBS | A | $227,477,273 |

AA | $83,459,000 | |

AAA | $466,812,629 | |

B | $21,524,000 | |

BB | $80,214,000 | |

BBB | $427,298,000 | |

CMBS Total | CMBS Total | $1,306,784,902 |

This is not a comprehensive glimpse of BSCs holdings, only about 25% of it, as insured by the two major monolines. They also have a very large chunk of "unidentified" securities which I think sports a very significant contigent of CMBS derivatives.

Add this to their other real estate related holdings then apply the marks that you see in the charts above and you have quite a few billion dollars of writedowns coming down the pike...

The actual underlying indexes are showing losses as well... From the MIT site.

MIT's commercial property price index shows its second straight quarterly decline

Indicates seven percent drop in commercial property since summer

February 5, 2008

The value of U.S. commercial real estate owned by big pension funds fell another 5 percent in the fourth quarter of 2007, according to an index produced by the MIT Center for Real Estate.

The drop in the quarterly transaction-based index (TBI), which tracks the price at which big pension funds buy and sell properties like shopping malls, apartment complexes and office towers, was the second straight quarterly decline. It was deeper than the 2.5 percent drop in the third quarter, and it means the cumulative fall since last year's midsummer peak is now more than 7 percent.

"This is evidence that the commercial property market continued to fall, and at an accelerated rate, through the last quarter of 2007, no doubt due to the effects of the credit crunch," said MIT Center for Real Estate Director David Geltner.

The TBI, based on properties sold from the National Council of Real Estate Investment Fiduciaries (NCREIF) data base, grew 64 percent from 2004 through 2006, then had another 8 percent spurt in the first half of 2007. The decline in the second half of 2007 still leaves commercial property prices at their level of a year ago, a level that was considered historically high at the time.

"If this is as far as it goes, the price decline we see so far in commercial property as reflected in the TBI may simply represent a correction of the froth that occurred in early 2007 as a result of very aggressive commercial mortgage underwriting practices," said Geltner.

The TBI measure of total returns for the year 2007 was 3.7 percent, which simply reflected operating income, with prices basically unchanged. Despite the upsurge in the first half of the year, this was the poorest calendar year annual performance for the index since 1992, when commercial property experienced its worst crash since the Great Depression. Index Co-Director Henry Pollakowski was quick to point out, however, that fundamentals in the commercial property market are much stronger now than they were in 1992.

"We don't have the kind of over-building we had then, and building occupancies and rents are much stronger. Commercial mortgage default rates are much lower than in the early 1990s," Pollakowski said.

The MIT Center's TBI is based on prices of NCREIF properties sold each quarter from the property database that underlies the NCREIF Property Index (NPI), and also makes use of the appraisal information for all of the more than 5,000 NCREIF properties. Such an index--national, quarterly, transaction-based, and by property type--had not been previously constructed prior to MIT's development of it in 2006. NCREIF supported development of the index as a useful tool for research and decision-making in the industry.

While the NCREIF properties well represent institutional investments such as pension funds, a second index based on a broader population of properties was subsequently developed at the MIT Center for Real Estate. That index, now published by Moody's Investor Services as the Moody's/REAL Commercial Property Price Index, will release its 4th-quarter results later this month. While the TBI represents pension funds' sales, the Moody's/REAL Index represents the broader commercial property market and includes a monthly national commercial property index.