Back in 2001-2002 I used the term "retroflation" in a series of newsletters and articles to describe what I saw as a battle between the forces of inflation and deflation. The Kress 30-year cycle had peaked in late 1999 and with it the 1990s bull market in stocks. The U.S. was in the throes of economic recession and tech stocks were in freefall. Yet the Kress cycles called for a major bottom in late 2002 with the 6-year/12-year cycle bottoming and the Fed was already beginning to aggressive cut interest rates, showing that it was serious about re-inflating the economy.

The long-term Kress cycles were obviously going to be a deflationary factor throughout the first decade of the 21st century. But the power of the Fed was too great to ignore and it was obvious the Fed wasn't going to sit idly and watch the forces of Kress cycle deflation wreak havoc on the global economy and financial system. The Fed fought back furiously with the biggest credit bubble this nation has ever seen. This of course led to a wild speculative frenzy in the real estate and commodities markets as well as in stocks. But with the Fed being the Fed, it wasn't long before they followed its long-standing policy of "leaning against the wind" and started tightening up on money and credit creation in 2004-2006. This led to the Credit Crisis and the 2007-2009 economic recession.

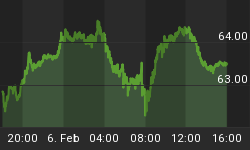

Now, as was true in 2001-2002, the Fed has seen fit to vigorously re-inflate the economy and the first effects of this were seen in the reversal of the gold and silver price in late 2008 and in other key commodity prices, such as copper, in early 2009. Joining the party in 2009 were the oil price and major grain prices. As one reflection of the re-inflation of commodity prices it is worth noticing that a leading indicator for the general commodities market, CME Group (CME), is showing a strong foundation for a longer-term recovery. Take a look at the 1-year daily chart shown below for an example of this. (Note: this is not an investment recommendation and is only being shown for illustration purposes).

Getting back to the concept of retroflation, what this term describes is the ongoing struggle between the long-term Kress cycles within the 120-year cycle series that are leaning heavily against the financial system and the united power of the world's central banks in staving off these deflationary forces. The analogy I've always used to describe this battle is that of a rubber inflatable mattress that has developed a series of leaks, both internally and externally among the various chambers. You can patch the external leaks but the internal leaks are almost impossible to fix. The result of this patchwork is that when you try re-inflating the mattress, instead of the air distributing equally throughout the mattress it creates bulges on one side of the mattress. You can push this air out of the bulge but then it only becomes distributed to another side of the mattress, creating yet another bulge somewhere else. This crude analogy explains what we've seen in the past few years with the Fed's reflationary efforts creating first a bubble in stocks, then real estate, then commodities.

You may remember that in the early phase of the previous cyclical market recovery in 2003 once the 6-year/12-year cycle had bottomed that stocks and commodities both benefited equally in the recovery rally that followed. This has once again proven to be the case in 2009 following last year's 6-year cycle bottom as the S&P 500 Index has seen its biggest recovery rally since 1975. Some commodities have recovered even more and this is reflected to some extent in the CME chart shown above. We're getting a bit ahead of ourselves in making this speculative statement but one can almost see the beginning of a repeat of the 2003-2007 experience which led to the financial woes the market experienced last year. In the 2003-2007 retroflation experience, the key industrial commodity prices soared, which led to a liquidation of America's wealth to other countries, most notably in the Middle East. The oil price alone did untold damage to the U.S. consumer and isn't given enough attention in the financial post-mortems so popular today (it's much more popular to focus attention on the real estate bubble). It would be beyond the scope of this commentary to get into some of the reasons for the runaway oil price, none of which had to do with the popular "Peak Oil" theory, but involved aggressive hedge fund participation and artificial supply manipulation among heavyweights in the oil industry. Suffice it to say that the maximum damage was inflicted in those years of the runaway oil price until the economy could no longer bear it and collapsed under the strain.

As an aside, one recent example of the manipulation of supply can be seen among state-owned oil companies. In his Money Forecast Letter, Adrian Van Eck observed that these companies responded to last year's dramatic price drop by routing oil tankers around the Cape of Good Hope instead of taking the usual route through the Suez Canal, adding days to their trips. According to Van Eck, tankers were also ordered to lower their speeds to make every effort at delaying ships of oil and gas to the ports. Refineries were also cut back and some wells were shut down as a false shortage was created. As Van Eck observes, "In the end, oil producers will win out. They have learned how to do so."

In the year to date, both stocks and commodities have benefited from the reflationary efforts of the central banks. Leading industrial user China has shown remarkable recovery and its stock market is reflecting the market's optimism for continued recovery in this new 6-year cycle. A reflection of China's new cyclical bull market can be seen in the China ETF (FXI) shown here. (Note: this is not an investment recommendation and is only being shown for illustration purposes).

So the commodities arena is definitely heating up and it's starting to look like commodities will once again outperform stocks in the economic recovery, as was the case in the 2003-2007 reflation. Assuming this is the destined outcome of the cyclical recovery, at some point we can probably expect to see more consumer inflation pressures, especially as reflected in retail food prices (which are already too high). An interesting parallel is provided by current Fed Chairman Ben Bernanke, who showed in his book on the Great Depression that retail food prices in the U.S. never fell in the early stage of the 1930s recession and didn't decline appreciably until 1933-1936. This is precisely the second half of the Kress 6-year cycle of that part of the depression and also coincided with the final "hard down" phase of the 40-year cycle. If history repeats that means we likely won't see retail food prices being pushed lower by the deflationary cycles until around 2011 (when the current 6-year cycle peaks) and through 2014 (when the 40-year cycle bottoms).

Worth noting is that the stock market also rose during the 1933-36 period while the 6-year cycle was in its ascending phase during the Depression. This gives us an historical basis of a continued stock market recovery this year (especially with the 10-year cycle still peaking) and of possibly spill-over strength in certain market sectors until 2011 when the last of the 6-year cycle, the last of the major Kress cycles in the 120-year series, peaks.

What are the thoughts of the insiders in the natural resource sector concerning the prospects for a natural resource recovery? Each week I speak to top executives with various natural resource companies, often printing the interviews for the benefit of subscribers to my Junior Mining Stock Report newsletter. Here is a sampling of what some of the top minds in U.S. and Canadian-based resource companies are saying right now.

Steve Altmann, President of ECU Silver Mining, thinks the recovery in silver price still has legs. "Internally," he told me, "we think the opportunity for silver prices are going to be absolutely huge. Everybody recognizes is that silver has the same investment fundamentals as gold. However, what it does have unlike gold is its industrial application, that is silver is one of the best conductors on the planet."

He further explained, "Silver applications are used everywhere and many people don't realize the application of its use in our everyday life. For instance, it's in our computers, TVs, wall switches, cell phones and several electronic instruments and it's also making a large impact into the medical field in terms of its anti-bacterial nature. Silver has much stronger industrial applications than gold and as we come out of this economic crisis and turn into a robust economy we'll be seeing a huge appetite for silver, particular when the silver Comex inventories are at historical lows. So we have a dynamic where we have silver performing like gold positively as an investment vehicle but more so down the road for its fundamental uses. This means the opportunities for the silver price to increase dramatically are all in place."

Jon Slizza, V.P. Finance for Azteca Gold Corp. explains what the credit crisis has meant to mining companies and their production plans. He told me, "To my way of thinking, we are either heading toward a future of a 'lost decade' like Japan had where we're suffering from disinflation, or a nasty bout of hyper-inflation. Governments around the world have responded to the credit crisis with the nuclear option in terms of monetary policies. I think that ultimately all the money printing will lead to currency devaluations that will look like wild inflation in the price of everything to the man on the street.

He adds, "Regardless of which future we are to suffer through, one thing is undeniable: these last six or nine months of turmoil has seen metals prices crater while at the same time capital and credit has disappeared. All kinds of projects around the world of all sorts, from energy to metals, have been either shelved, turned off or put off and the result will eventually show up as shortages in some of these critical elements which we use to build our societies. There is much infrastructure yet to be built on this planet, and much of what was built decades ago needs replacing. Bridges are falling, water mains are bursting, and much of the electrical grid is inefficient...at least here in the U.S.

He concludes, "If the 'big money' ever moves into precious metals to a significant degree, for example large pension funds increasing their allocations to commodities, gold and silver could really fly."

When asked if he thinks the uranium price recovery can continue, Gregg Sedun, President and CEO of Uracan Resources, responded positively. "Yes, we're very optimistic of a uranium price recovery and we think the fundamentals within the uranium business are tremendous. In so many different businesses and commodities you see the pendulum swinging in opposite directions. A year ago the markets were heavy and went to an extreme within six months or less last fall. With the uranium price it's the same - it went too far up and has come too far down on this latest contraction. We've seen the bottom in our view and we see more experts project that price is the only thing that matters....Our view is that the long-term uranium price has a lot of upside."