The following is commentary that originally appeared at Treasure Chests for the benefit of subscribers on Tuesday, May 18th, 2010.

What would you say if it was suggested that our business and political leaders, the larger bureaucracy, and their market managers were all acting in an increasingly irrational fashion, and are exacerbating negative long-term effects with all their meddling in things they should better leave alone, those being any market they decide to manipulate for whatever reason. Would you say that one sentence sums up a large part of the condition our condition is in without naming all the names, politics, etc. as none of this really matters in the end? In my opinion this is certainly true with regard to the two-party system in the US, and that of all Western economies as a result, where all the meddling has gone well past any prior useful purpose, and now in fact threatens to become the measure of decay from within. That's how all empires end you should know, from within, with the American Empire ultimately no exception to this rule undoubtedly.

Of course because we are talking about a global empire here not paralleled in magnitude since that of Rome, the pathology of ill-fated behavior and process associated with the unwinding can be quite lengthy and complex, with crisis episodes at various intervals along the way. The Greek bailout last week is a classic example of this, where as the critical nature of events accelerated because of previous meddling on the part of European Union (EU) in microcosm, more meddling was naturally required to compensate for previous policy, with intensity on the increase as the prognosis for the Union became better understood. Or at least this what EU officials were undoubtedly thinking when they cobbled together a bailout for the PIGS, thinking this should buy us some time in being so large ($1 trillion), at a minimum.

And now that any semblance of credibility has been lost to the EU, along with it's failing currency that continues to crash despite last weeks measures designed to stabilize the eurozone, they are exposed for the fraud of inflation, which is a precursor of what is to come for all Western economies. High yield funds are witnessing record outflows and credit spreads are threatening to do a repeat of the subprime crisis, or worse. So, don't think this mess is limited to Europe, like our bought and paid for mainstream media and their buddies in government and business would like you to believe. Of course Europe might be the present epicenter in the larger demise of Western influence, along with its hegemony, despite a similar fate virtually certain for the euro sooner or later. Here, it's only a question of how long Germany is willing to pay other peoples bills at the behest of the international banking cartel. Once Germany decides to pullout of the EU, and they will eventually, the euro will be history.

Impossible? Goldman Sachs apparently thinks so, however knowing them these comments are more likely directed at getting the euro turned higher because they are long in their proprietary trading accounts than anything else. And the euro did in fact turn higher yesterday which on top of making certain traders happy, will likely make the larger price management machine happy as well considering they can use such a turn to support US equities, along with suppress precious metals in that the EU is now being portrayed as the monetary profligate in the media instead of the US, taking the heat off the Fed, US inflation measures, etc. So, don't be surprised if this theme is milked in the media more, however it should only have limited impact on trade, meaning it's influence in supporting stocks and depressing precious metals prices should be fleeting.

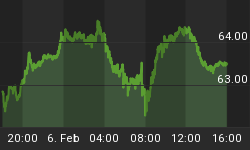

Certainly as far as precious metals are concerned, with physical shortages now becoming almost chronic, we would not run out and sell any core positions due to such a prospect. Instead, we would use any weakness to accumulate, with both shorter term, and of course longer term prospects for gold and silver still well in hand, especially as this pertains to the physical metals. For traders, if the count below is correct, weakness today should prove rewarding, especially with the open interest put / call ratio on GLD ticking up considerably yesterday (which will help to draw prices higher into options expiry Friday), along with seasonal strength still in play. Either way however, whether prices go higher short-term or not, longer-term investors might consider holding off any purchases in waiting for a larger degree correction likely into fall. Tops in May / June have historically led to bottoms in November during the present bull, which could play on the trade. (See Figure 1)

Figure 1

It should also be noted such an outcome, that being gold continuing to sail higher to $1350ish in coming weeks does not necessarily need to be accompanied by falling stocks either, where it should be recognized the larger degree correction into fall discussed above will likely occur due to a deflation scare as stocks come off into the same timing window. In fact, if stocks can remain buoyant this week using the euro ploy discussed above to thwart the influence of declining open interest put / call ratios on the US indexes, then, like gold and silver, they will likely enjoy more strength into June, furthering the expanding pattern. It's either that or weakness later this week could develop into a head and shoulders pattern or three peaks and a domed house formation(s) in the broad measures of stocks. Not knowing which will occur no pictures to this effect will be displayed here today, however we will be sure to keep you posted as process unfolds. One thing is for sure however, significant weakness today would go along way in negating a more bullish outcome past this point, bringing in the possibility of a deflation scare dead ahead. (See Figure 2)

Figure 2

How could this be? Well, for one thing, if stocks get creamed here, and things don't necessarily go as planned for the euro, the Dow / TSX (TSE) Ratio is threatening to breakout again, where a monthly close above the swing line would have to be taken seriously. And the thing about this chart, and its deflation message, is it's not on many radar screens, which makes such an outcome very possible from a contrarian perspective considering increasing stock market and economic (the Canadian housing bubble is now imploding) vulnerabilities at present. Chinese stocks have been the other half of the inflation trade for the longest time, however now we have them on the ropes, leading the way in this regard. Now, all we need is for what is perceived by many to be the safest inflation trade on the planet (because Canada is thought by many to be unaffected by the slowdown) to begin rolling over against the Dow and a panic of sorts could ensue, blowing out credit spreads on a global basis, and bringing in the specter of a credit crunch, part deux. (i.e. a resumption of the secular trend.)

Unfortunately we cannot carry on past this point, as the remainder of this analysis is reserved for our subscribers. Of course if the above is the kind of analysis you are looking for this is easily remedied by visiting our web site to discover more about how our service can help you in not only this regard, but also in achieving your financial goals. As you will find, our recently reconstructed site includes such improvements as automated subscriptions, improvements to trend identifying / professionally annotated charts, to the more detailed quote pages exclusively designed for independent investors who like to stay on top of things. Here, in addition to improving our advisory service, our aim is to also provide a resource center, one where you have access to well presented 'key' information concerning the markets we cover.

And if you are interested in finding out more about how our advisory service would have kept you on the right side of the equity and precious metals markets these past years, please take some time to review a publicly available and extensive archive located here, where you will find our track record speaks for itself.

Naturally if you have any questions, comments, or criticisms regarding the above, please feel free to drop us a line. We very much enjoy hearing from you on these matters.

Good investing all.