The good news is:

• The small and mid cap indices as well as the NASDAQ composite (OTC) closed at multi year highs Friday.

The negatives

The small caps hitting multi year highs is an intermediate term positive implying higher highs for all of the major indices in the next few months.

Most of the breadth indicators did not confirm Friday's highs and that, along with the seasonal pattern, suggests short term weakness.

Advance - Decline lines (ADL) are a running total of declining issues subtracted from advancing issues. Their bias varies widely and occasionally shifts. The NYSE ADL, and ADL calculated from NYSE issues had a slightly negative bias until about 10 years ago when the bias became wildly positive. The NYSE ADL made an all time high in early 2004 (the previous high was reached in March 1956) and since then has been nearly useless because of its extremely positive bias. So it is interesting to note that the NYSE ADL did not confirm last Friday's highs in the small and mid cap indices.

The chart below covers the past 6 months showing the S&P 500 (SPX) in red and the NYSE ADL in blue. Dashed vertical lines have been drawn on the 1st trading day of each month. This is not a dramatic non confirmation, but significant it its rarity over the past several years.

The next chart is similar to the one above it covers the past 65 years so you can see the historical changes in the indicator. Dashed vertical lines have been drawn on the 1st trading day of each year.

New highs came back last week reaching their highest levels since early November, however indicators derived from new highs are lagging.

The chart below covers the past 6 months showing the OTC in blue and a 10% trend of NASDAQ new highs (OTC NH) in green.

The OTC hit a multi year high on Friday while OTC NH is off its high reached in early November.

The chart below is similar to the one above except it shows the SPX in red and NY NH has been calculated from NYSE data.

The SPX is 0.1% off its November high while NY NH is well off its November high.

The positives

The chart below is an update of one I have been showing every week, it covers the past 6 months showing the OTC in blue and a 40% trend (4 day EMA) of the ratio of NASDAQ new highs to new highs + new lows (OTC HL Ratio) in red. Dashed horizontal lines have been drawn at 10% levels of the indicator; the line is solid at the neutral 50% level.

There are trading systems that impose a No Sell filter when variations of this indicator are above 80%. It reached 82% Friday.

The next chart is similar to the one above except is shows the SPX in red and NY HL Ratio has been calculated from NYSE data.

NY HL Ratio has had a more positive bias than OTC HL Ratio so the thresholds should be moved up about 10%. NY HL Ratio reached 91.8% Friday so it is positive any way you interpret it.

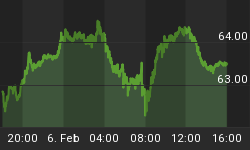

The secondaries lead both up and down; Friday the secondaries hit multi year highs while the more widely followed blue chips fell short.

The chart below covers the past 2 months showing some of the major indices plotted on log scales so you can see the relative difference in performance. Dashed vertical lines have been drawn on the 1st trading day of each week.

Seasonality

Next week includes the 5 trading days prior to the 2nd Friday of December during the 2nd year of the Presidential Cycle.

The tables below show the return on a percentage basis for the 5 trading days prior to the 2nd Friday of December during the 2nd year of the Presidential Cycle. OTC data covers the period from 1963 - 2009 and SPX data from 1953 - 2009. There are summaries for both the 2nd year of the Presidential Cycle and all years combined. Prior to 1953 the market traded 6 days a week so that data has been ignored.

A couple large losses in 1994 and 2002 give the OTC a slightly negative return for the 2nd year of the Presidential Cycle. Returns by all other measures have been slightly positive.

Report for the week before the 2nd Friday of December.

The number following the year is the position in the presidential cycle.

Daily returns from Monday to 2nd Friday.

| OTC Presidential Year 2 | ||||||

| Year | Mon | Tue | Wed | Thur | Fri | Totals |

| 1966-2 | 0.13% | -0.38% | 0.13% | 0.67% | -0.24% | 0.31% |

| 1970-2 | 1.07% | 0.16% | -0.83% | 0.73% | 0.67% | 1.80% |

| 1974-2 | -0.52% | 1.47% | 0.87% | 0.15% | -0.24% | 1.74% |

| 1978-2 | 0.33% | 0.94% | 0.66% | 0.08% | 0.19% | 2.20% |

| 1982-2 | 0.90% | 0.57% | 0.02% | -1.44% | -1.43% | -1.38% |

| 1986-2 | -0.54% | -0.55% | 0.01% | -0.37% | -0.50% | -1.95% |

| Avg | 0.25% | 0.52% | 0.15% | -0.17% | -0.26% | 0.48% |

| 1990-2 | -0.02% | -0.94% | 0.66% | 0.29% | -0.72% | -0.72% |

| 1994-2 | 0.09% | -0.60% | -0.94% | -2.06% | -0.01% | -3.52% |

| 1998-2 | 1.87% | -0.28% | 0.77% | -1.68% | 0.66% | 1.33% |

| 2002-2 | -3.89% | 1.73% | 0.42% | 0.21% | -2.65% | -4.18% |

| 2006-2 | 1.46% | 0.16% | -0.27% | -0.74% | 0.40% | 1.01% |

| Avg | -0.10% | 0.01% | 0.13% | -0.80% | -0.46% | -1.22% |

| OTC summary for Presidential Year 2 1966 - 2006 | ||||||

| Avg | 0.08% | 0.21% | 0.14% | -0.38% | -0.35% | -0.31% |

| Win% | 64% | 55% | 73% | 55% | 36% | 55% |

| OTC summary for all years 1963 - 2009 | ||||||

| Avg | 0.14% | 0.03% | 0.02% | -0.36% | 0.23% | 0.06% |

| Win% | 60% | 49% | 54% | 47% | 55% | 51% |

| SPX Presidential Year 2 | ||||||

| Year | Mon | Tue | Wed | Thur | Fri | Totals |

| 1954-2 | 0.78% | 0.46% | -0.17% | -0.49% | -0.37% | 0.21% |

| 1958-2 | 0.11% | 0.57% | 1.21% | -0.21% | -0.24% | 1.45% |

| 1962-2 | -1.25% | 0.08% | 0.50% | -0.34% | 0.24% | -0.77% |

| 1966-2 | 0.14% | 0.75% | 1.09% | 0.40% | 0.11% | 2.49% |

| 1970-2 | 0.54% | -0.52% | 0.08% | 0.42% | 0.38% | 0.89% |

| 1974-2 | 0.91% | 2.56% | 0.58% | -0.33% | -0.56% | 3.16% |

| 1978-2 | -0.14% | 1.34% | 0.05% | -0.42% | -0.46% | 0.37% |

| 1982-2 | 2.22% | 0.67% | -0.64% | -1.28% | -0.31% | 0.67% |

| 1986-2 | 0.00% | -0.75% | 0.67% | -1.11% | -0.33% | -1.52% |

| Avg | 0.71% | 0.66% | 0.15% | -0.54% | -0.26% | 0.72% |

| 1990-2 | 0.35% | -0.74% | 1.15% | -0.26% | -0.77% | -0.27% |

| 1994-2 | 0.01% | -0.05% | -0.41% | -1.28% | 0.34% | -1.40% |

| 1998-2 | 0.93% | -0.53% | 0.18% | -1.56% | 0.13% | -0.85% |

| 2002-2 | -2.22% | 1.40% | 0.06% | -0.37% | -1.34% | -2.48% |

| 2006-2 | 0.89% | 0.40% | -0.13% | -0.40% | 0.18% | 0.94% |

| Avg | -0.01% | 0.09% | 0.17% | -0.77% | -0.29% | -0.81% |

| SPX summary for Presidential Year 2 1954 - 2006 | ||||||

| Avg | 0.23% | 0.40% | 0.30% | -0.51% | -0.22% | 0.21% |

| Win% | 71% | 64% | 71% | 14% | 43% | 57% |

| SPX summary for all years 1953 - 2009 | ||||||

| Avg | 0.18% | -0.01% | 0.03% | -0.29% | 0.20% | 0.13% |

| Win% | 58% | 45% | 52% | 40% | 67% | 54% |

Money supply (M2)

The money supply chart was provided Gordon Harms. Money supply growth has been steady at a slightly elevated level.

Conclusion

The market is a little overbought which should subdue returns for the early part of next week and seasonality goes negative at the end of the week.

I expect the major averages to be lower on Friday December 10 than they were on Friday December 3.

This report is free to anyone who wants it, so please tell your friends. They can sign up at: http://alphaim.net/signup.html. If it is not for you, reply with REMOVE in the subject line.

In his latest newsletter Jerry Minton looks at the idea that continuous exposure to stocks is the way to get the "average" long-term return of the market. If you are retired or about to retire, you will want to read "Unnecessary Risks" at www.alphaim.net and sign-up for Jerry's free bi-weekly newsletter.

Thank you,