Two days does not a trend make, but then again all trends consist of at least two days.

I am sure it has been pointed out by others, but while it is early to call this a correction-in-the-making in equities-land, the behavior of the VIX (see Chart) certainly suggests that this may be a bit more than the somewhat-tepid, garden-variety consolidation we saw in November.

This looks more like a selloff-spike than the November sub-correction.

It bears noting, as well, that Tuesday and Wednesday in the stock market were the two busiest days of the year volume-wise, with 1.25bln shares changing hands both days. That being said, from a technical perspective (see Chart below) the rally has merely been nicked, not mortally wounded. Penetrating a steep uptrend-line is not necessarily antecedent to a plunge, anyway, but you can be sure that if today's lows are broken tomorrow there will be technical traders who take note.

Steep trend for the SPX. Amazing how long it has held!

WTI crude oil touched the psychologically-important (I don't even know why I say that) $100 level today, and though it finished below that level this little spike has some economist starting to wring their hands. As I said before, higher oil prices are not likely to make a significant direct impact on the economy unless oil goes significantly higher and maintains that level for a while. That's partly because when you buy oil and petroleum-derived products (as an American; this is less true in other countries that do not produce much oil domestically) some of the money you're losing is going to someone else. Call it "Big Oil" if you want, although Big Oil is owned by pensioners, orphans, and you if you own an index fund, but the point is that some of the direct effect of an oil price increase is a redistribution flow from consumers to producers. If you're mainly a consumer (and most of us are more consumer than producer), then you will mainly see the costs and not the back-door benefit provided when the producers spend the extra money you sent them. In other words, it will feel worse for you than it actually is for the economy-at-large. Again, this is not as true if you live in, say, the Bahamas (but why would I feel sorry for anyone who gets to live in the Bahamas?!).

While the 0.6% fall in equities (back-to-back triple digit declines in the Dow) will get the most ink, that isn't disturbing by itself. As I pointed out above, while the rise in the VIX and volumes is suggestive, no real technical damage has been done yet. But there are two other things that raise my eyebrows somewhat more.

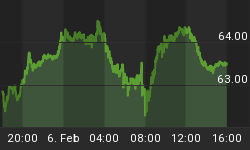

First, the bond market declined today rather than extending the rally. Whatever the "flight to quality" that happened on Tuesday, it wasn't repeated on Wednesday. Second, the same applies to the dollar, which not only declined on Wednesday but didn't even manage much of an advance on Tuesday. The buck is back near February lows (see Chart).

The dollar surprisingly saggy considering the geopolitical landscape. Is it no longer "quality"?

Those two facts suggest that stocks are not declining merely because of unrest in the Middle East. Perhaps there is a whiff of a stagflation outcome, but that shouldn't pressure the dollar since energy is an input into inflation globally. I think Libya may be the excuse for the equity break, in other words, but not truly its cause.

Inflation-indexed bonds (that is, TIPS) and swaps of course continued to do well on the rise in energy (and grains recovered some today too). The 5y inflation swap has now exceeded the Jan 2010 highs and is above 2.50%. The high in 2008, prior to the crisis, was well above 3% but that was with $147 oil and no sense of what was impending.

This seems like a useful time to step back and look at what has happened to inflation expectations since the Fed has begun its current easing campaign. The chart below (Source: Enduring Investments) shows the CPI swap curves for August 27th (the day Bernanke made it plain QE2 was coming), November 12th (the day QE2 technically began), January 4th (where we started the year), and today.

Inflation expectations have clearly risen and continue to do so.

The Fed makes a big deal about how forward measures of inflation expectations have remained "contained." By that they specifically mean 5y inflation, 5y forward, which is a function of the 5y and 10y points on the swap curve. That forward point, it is true, has not risen dramatically because the 5y point has generally outpaced the 10y point higher. But as this time-lapse chart makes clear, it would be absurd to claim that inflation expectations have not risen. The short end of the curve may well have done what it did because of the rally in commodities prices, almost uninterrupted since August, but even longer-dated inflation expectations have risen if you measure them (properly) from when expectations might reasonably have been affected - when Bernanke first told us QE2 was coming.

These are curves for headline inflation, since that's the only thing which trades in the market (although in principle we could use these to derive expectations for core inflation). But clearly, the curve is now telling us that the market expects inflation to rise above the Fed's purported target and to remain there for a generation or so. Yield curves are notoriously poor predictors, but if the Fed were serious about wanting to keep inflation expectations reined in they would have to take a long, hard look at tightening credit right now. The fact that there is no chance of that - because of the parlous state of the economy generally and the growth risks from energy and renewed sagging of home prices - should tell you what you need to know about the Fed's true credibility when they pledge to "be aggressive" on inflation. Easy to say, not easy to do.

Now, if inflation is indeed something we need to worry about, equity bulls will immediately suggest that this is a great reason to buy stocks. After all, equities are real assets (in that they represent shares of a business which participates in the real economy) so it stands to reason that they should do well in inflationary environments. Well, it may stand to reason but unfortunately it does not stand to the data. What the data show is that while earnings may grow with inflation, the multiple assigned to those earnings is lower when inflation is higher. So the intrinsic value of your share in the business may keep up, but the thing you care about, the market price of that share, will tend to lag as inflation rises.

The fact that this happens is actually somewhat odd. There is no natural reason that a share of a business should be worth a lower multiple at higher levels of inflation, and this is a big puzzle for economists (as opposed to investors, who tend to care less about the theory of why this happens than the fact of its happening). I've just finished reading a paper by John Y. Campbell and Tuomo Vuolteenaho of Harvard called "Inflation Illusion and Stock Prices" that demonstrates a very high correlation between stock market mispricing and the level of inflation. According to the authors, "...the level of inflation explains almost 80% of the time-series variation in stock-market mispricing." In a nutshell, the question is this: if a stock price is the discounted value of future dividends, then when the interest rate at which we discount those dividends rises because of expected inflation, then the growth rate of those future dividends should also rise by a similar increment, and the level of inflation should not affect the valuation of equities. Or, put another way, the real growth of dividends and the real interest rate should be somewhat related and more stable than we actually observe stock prices to be. But stock prices aren't just volatile - they systematically underperform when inflation moves higher and vice-versa. This suggests (the authors illustrate) that investors are subject to money illusion, and they test this hypothesis:

"Modigliani and Cohn (1979) propose a more radical third hypothesis. They claim that stock market investors (but not bond market investors) are subject to inflation illusion. Stock market investors fail to understand the effect of inflation on nominal dividend growth rates and extrapolate historical nominal growth rates even in periods of changing inflation. Thus when inflation rises, bond market participants increase nominal interest rates which are used by stock market participants to discount unchanged expectations of future nominal dividends...From the perspective of a rational investor, this implies that stock prices are undervalued when inflation is high, and may become overvalued when inflation falls." (©John Y. Campbell and Tuomo Vuolteenaho)

They proceed to test this hypothesis and prove to my satisfaction that bond market investors are smarter than stock market investors (well, anyway that's my summary of the conclusion).

It's a pretty neat paper, and worth the $5 you need to pay the authors for a copy.

This is a basic truth, I suspect, with most assets that are purported to be inflation-linked. There is no reason that I can see that equity investors would be subject to inflation illusion while, say, timber investors or real estate investors would not be. If you want inflation protection, in other words, the closer you can stay to explicit inflation-linkage, the better.

.

Tomorrow's economic data includes Initial Claims (Consensus: 405k vs 410k last), Durable Goods (Consensus: +2.8%, +0.5% ex-transportation), New Home Sales (Consensus: 305k vs 329k last), and even the FHFA Home Price Index. I am not sure any of this really matters as much as Libya and the rest of the region; as much as the Irish elections on Friday; or as much as any erosion in sentiment among the true believers in the equity world. I remain close to home.