QVM Clients:

There is still no agreement concerning the US debt ceiling. Standard and Poor's is doing road shows to pension and other institutions preparing them for a possible US credit rating downgrade. Key figures such as Mohamed El-Erian (former head of Harvard endowment, and current CEO of the large asset manager PIMCO) say a downgrade to AA from AAA is becoming probable, even if a debt deal is reached, due to loss of credibility, and due to the failure to solve the deteriorating debt-to-GDP ratio.

That said, there are as of yet no signs of a catastrophic market response. The level of hand wringing done on the TV news shows this weekend is not matched by the action in the futures and overnight markets.

It is important to note, for example, that the US stock market is still in an upward sloping pattern and is not showing transition to bear condition at this time. Corporate profits and growth in the US are still good, and valuation multiples are not high by historical standards.

The uncertainty factor, however, is very high. There is uncertainty as to government action, and uncertainty as to investor interpretation. Markets are likely to be choppy with sea-saw days of large ups and large downs as government matters are worked out. The potential for a strong relief rally or a strong down draft is a reality we face.

The attached chart of the year-to-date S&P 500, along with its 200-day average in gold shows it to be still in an ascending path. The red horizontal line shows the price of near futures for the index as of 10:00 PM tonight. It's down about 1%, as are the futures for the NASDAQ 100 and the Dow Jones 30 Industrials, but that is hardly a panic and well within daily volatility ranges.

The 1400 level for the S&P 500 is still a general consensus target for year-end (something in the 4% gain range). That does not compare favorably to the potential for a 10+% correction, or worse.

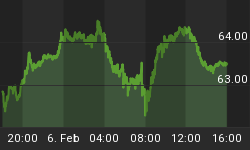

We can't be as positive about the Chinese stock market, which is flat at best, if not down in direction. That corresponds reasonably with the efforts by the government there to moderate growth and remedy some of the excesses they experienced as a result of the post-2008 stimulus programs. (see attached chart).

Stock markets in Japan, China, Taiwan, Korea, Singapore and Malaysia are all down at this time, but only about 0.25% to 0.90% -- again within normal daily volatility. UK futures are down about 0.5%.

Because the index is still in an up trend, we are holding our equity positions, but because of the high uncertainty, we have been maintaining about 30% cash for weeks now and will wait for more information before committing those assets to risk.

The potential for a repeat of 2008 was much greater a couple of weeks ago, with both the US and Europe in hot water. Europe has cooled things down for a while, although they have not really solved anything. The US is likely to "kick the can down the road" too, but reputational damange will linger with likely impact on US borrowing costs.

The paradoxical aspect of US Treasuries is that people have flocked to them in panic for safety, at the same time that their long-term credit worthiness is being questioned. In the short-term that makes interest rate movements all the more perplexing.

US Treasuries are down a bit in price, but not so much to be unusual. The 2-yr, 10-yr and 30-yr rates are 0.40%, 3.00% and 4.31% now, versus 0.40%, 2.99% and 4.26% Friday. No signs of panic there.

Crude oil is off. Brent down 0.72% and West Texas Intermediate down 1.04%, at 117.81 and 98.89 respectively.

Gold is up 0.78% at 1612.80.

Copper is down 0.56%.

All-in-all, no big deal in the markets so far with respect to the circus in Washington D.C. That is not an all-clear by any means, but the Monday Armageddon potential on every business news show this weekend has not yet begun to materialize. There could be a rush to the exits in the morning. Who knows how many worried retail investors are just waiting for 9:30 AM. Markets could also move down over time by a thousand cuts. That is all to be determined and dealt with when as and if it occurs.

For tomorrow morning we plan to be watchful, but have no current plans to change allocations.