It's hard for me to truly grasp the reality of a world in which the downgrade of the British Empire's credit (late on Friday) was the third most-important story, but so it is.

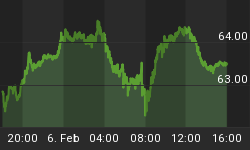

The UK was dropped from AAA to AA1 (one notch, but an important one) by Moody's on Friday, and sterling dropped to the worst level against the dollar since 2010. In the grand scheme of things the drop to $1.51 was not critical, and the cable is still almost in the range it has held for the last few years, but some technicians are sure to see the breakdown as an ugly technical development (see chart, source Bloomberg).

But, fortunately for Britain, the Italians were drawing global attention to themselves and the Euro. As ballots were counted in the election to establish the balance of power in that nation, global markets careened up and down depending on the latest tallies. Ultimately, it appeared that a split government was in the offing, with a general repudiation of the politicians which have been party to austerity measures. The party of Berlusconi, who ran opposing the austerity measures, combined with the "Five Star Movement" party of Grillo, who advocates suspending interest payments on Italian debt and holding a referendum on Italian membership in the Euro, would represent an outright majority in the Senate although the lower house ends up in the hands of Bersani because of a "bonus premium" that guarantees the winning coalition will have a majority.

In the end, the reason the Italian election matters more than the downgrade of the UK isn't because the election raises questions about whether Italy is committed to austerity; it's that the election raises questions about whether Italy is committed to the Euro. This isn't Greece. With a $2 trillion economy, Italy is the third largest member of the Eurozone, behind Germany ($3.4T) and France ($2.6T). It is the size of the other four PIIGS combined. And they've also issued a lot of inflation-linked bonds, by the way, so look carefully if you own an inflation-linked bond fund that invests in non-US bonds, just so you know.

Now, Italy isn't going to default any time soon. They're going to have another election, and in the lead-up to that one there will be more concern and angst. But then the leaders will use that as a bargaining chip, etc. etc.. We're a long way from a default or exit of Italy from the Euro. But we're probably not as far from fear of default or exit.

Still, the immediate uncertainty is past. The markets will calm back down reasonably quickly (which doesn't mean they'll rally, being overpriced to begin with). Each successive fire drill will cause a shorter and less-intense period of instability in Europe, until eventually the crisis completely passes, or one episode turns out to be qualitatively different and the whole thing breaks down.

And speaking of episodic crises brings us to fiscal cliff redux. The U.S. will hit the sequester barrier in a few days, with almost no chance that it will be averted. The Republicans seem comfortable that this isn't such a big deal, and that if it turns out they are right then the scare tactic they feel is being used against them will be defanged. The Democrats seem to believe (and intent on making sure everyone else believes) that any cut in expenditures is tantamount to the End of Days. I don't think the market ought to react very seriously to it, because we're only talking 0.25% of GDP, but that all depends on how much hyperventilating we get from the media.

Still, it's an interesting story because if it turns out that the budget can be cut by 2% (albeit 2% from baseline, which is still an increase over last year) without the economy going into the loo, then we've moved the goalposts for future negotiations. And if both sides can understand that, then cutting spending (even real spending!) by 2% per year will slowly get the budget back on a course that, while not sustainable, at least doesn't lead to immediate immolation.

I am not sure how stocks will react to all of this (have I mentioned they seem expensive?), but I know that all three stories should be bond-bullish. The 10-year yield made it all the way back to 1.87% today after peeking over 2% several times the last few weeks. I think there is further upside to bonds for now, and that may mean that breakevens can also retreat some from near all-time highs. If I am right, then selling 10yr notes if they approach 1.65% or buying 10-year BEI near 2.40% represent better placement for the long term trades, which I expect to be higher in yield and in breakevens over 2013.