Interest rates soared again last week. This weekend a lot of people are running a lot of numbers and getting some terrifying results.

It seems that the past few years of falling interest rates have lulled a big part of the global economy into financing with variable-rate debt. So when interest rates go up, there's a world-wide reset in interest costs that, best case, amounts to a tax increase on individuals and businesses and, worst-case, threatens to blow up the whole system.

The most familiar but least worrisome part of this story is the adjustable rate mortgage, or ARM, which is basically a teaser-rate home loan that rises over time towards the prevailing 30-year fixed rate. This rate jumped from 3.5% to 4.5% in just the past month, which means ARM resets are now aiming at a higher target. For ARM holders, the resulting higher monthly mortgage payment is exactly like a pay cut or tax increase, leaving less around at the end of the month for new cars, vacations, etc. So discretionary spending drops and, other things being equal, the economy slows down. This is serious for a system that, when evaluated using real numbers (see Shadowstats.com) is already in recession.

Another victim is the long-term bond. Retail investors poured about $1 trillion into bond funds between 2009 and 2012, in part because bonds had been going up pretty much forever, and in part because investors were scared and bonds were sold by credulous financial planners as safe.

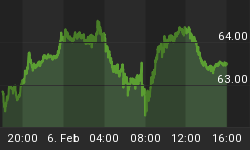

For a while it worked. Bond prices soared as long-term rates kept falling, which helped both individuals and pension funds rebuild capital lost during 2009's debacle. But since the beginning of this year US bond funds have seen $60 billion depart, while bonds themselves have fallen hard (though, okay, not nearly as hard as gold). The following chart shows the price of US 20-year Treasuries, which are down by almost 15% since April.

In other words, the "safe" part of individual and institutional portfolios is tanking. Here again, this is like a big pay cut which makes the holders of these funds less rich and therefore less likely to spend money.

But the real systemic risk enters with sovereign debt. One of the many ways the US, Japanese and European governments hide the effects of their mounting debt is by doing most of their borrowing for short periods of time, a few months to one year, where rates are close to zero and money is effectively free. In some cases short-term rates have fallen faster than borrowing has risen, producing lower interest costs even while debt has been piling up. Now, with long-term rates rising, governments have a choice: either roll their maturing long-term debt into very short-term paper, which would keep interest costs down but make it necessary to roll over even more debt each year, or keep the maturity of their debt constant and see their interest costs rise dramatically. Or have their central banks buy even more debt and write off the interest, which might prolong the lie for a while, but at the risk of a tidal wave of newly-created currency wreaking various kinds of havoc.

Now for the big one: Hedge funds and money center banks have created hundreds of trillions of dollars of interest rate swaps, in which holders of a security that pays a fixed rate of interest exchange this income stream for a variable stream based on some benchmark interest rate. The players on the variable-rate side of the bet lose big if rates keep rising. And most money center banks and many, many hedge funds are in this position. All it will take is a few of them to be overwhelmed by these bets going sour to pull down the whole show -- exactly as happened with credit default swaps in 2009.

The interesting (if that's not too neutral a word) thing about all this is that the events mentioned here will happen simultaneously if rates keep rising. ARM and bond fund holders will have less money to spend, slowing economic growth; governments will see their interest costs spike, making borrowing more expensive and risking a flight from their now clearly-mismanaged currencies; and derivatives markets will see growing instability in interest rate swaps, which might threaten rest of the rat's nest that is the global banking community.

All because interest rates return to historically normal levels.