Thursday evening's public discussion between Fed Chairman Janet Yellen and former chairmen Volcker, Greenspan, and Bernanke - these last three in order of gravitas and effectiveness and (perhaps not unrelatedly) reverse order of academic accomplishment - was a first. Never before, apparently, have four current and former Fed chairmen appeared on the same stage. This is less amazing than it seems: prior to Alan Greenspan it was the practice of the Federal Reserve to remain out of the limelight.

Honestly, we all probably would have been better off had they stayed there.

Still, it was a fascinating event. The International House, which hosted the event, called it the "Fabulous Four Fed chairs," but since they did not serve contemporaneously a better image is probably Mount Rushmore...if Mount Rushmore had the faces by Nixon, Hoover, Carter, and Andrew Johnson instead of Washington, Lincoln, Teddy Roosevelt, and Thomas Jefferson.

Okay, all bond guys have a soft spot for Paul Volcker, who was the last Fed Chairman to try monetarism and managed to break the back of inflation using its common-sense prescription. But he should have stayed retired. The Volcker Rule has sucked a tremendous amount of liquidity out of the market (in conjunction with other Dodd-Frank rules) and is clearly a stain on his resumé.

Everyone was hoping that this collection of experienced policymakers would give us some clear consensus about what the Fed should do now - raise rates as per the original path that was implied? Raise rates more slowly? Maintain rates? Keep on adding liquidity? Instead, there was almost nothing useful to be gleaned from the conversation. The three ex-chairmen seemed to be competing to make the funniest statement (some intentionally, and some unintentionally like Bernanke's statement that "unwinding the balance sheet is very straightforward") without saying anything constructive, challenging, or even useful about current and future Fed policy; Yellen seemed to want to say useful things but it isn't clear she has anything useful to say.

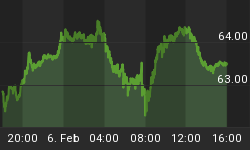

One overwhelming consensus was that the economy is doing just fine, but isn't a "bubble economy." Volcker did allow that "there are aspects of the financial world that are overextended." Oh, do you think so? Maybe something like the chart below, which is an updated version of Figure 9.7 from my book?

I guess that might be considered overextended.

Here are two other interesting snippets:

- Bernanke, asked "how will you unwind" the extraordinary measures he instituted, wisecracked "Fortunately, I don't have to," which considering the scale of what he did is a clever witticism that I am sure Dr. Yellen appreciated. After expressing, as I noted earlier, that unwinding is really easy, he pointed out languidly that the Fed's balance sheet, relative to GDP, is "about the same size of most other central banks." Does he really think no one was paying attention since 2008? The reason all central banks have huge balance sheets is that the Fed did it first and they all followed. If you consider "most other central banks" to include others throughout history...no, it's not even close.

- Yellen didn't address the elephant in the room, but went so far to pat its rump and then pretend it wasn't there. She described the criteria the Fed had had for the December increase in interest rates (substantial progress towards employment goal, and inflation heading back up), but didn't feel like explaining that when even more progress had been made on employment, and inflation was even higher, at the next two meetings the Fed decided to pass. She noted that "headwinds" in the "legacy of the financial crisis" and "weak global growth" meant that "the neutral rate is very low," but unless that neutral rate happens to be 0.25%-0.50% such a comment begs the question. Those headwinds haven't gotten any worse since December! As such, she left completely unanswered the $64,000 question[1] which is "what the heck would make you tighten again?"

In short, all of these notable central bankers (which is a little like saying "these notable hobos") seemed to agree that everything is just fine and there is no urgency with respect to anything right now. I've spent the last quarter-century deciphering three of these four speakers, and I must say I can't decide whether "everything is fine" means "the Fed can go ahead and tighten now, because everything is fine," or "there's no reason for the Fed to tighten now, because easing forever doesn't seem to be a problem."[2]

So, markets remain suspended from the pendulum of complacency, which right now seems to be quite a bit on the "complacent" side but will, I suspect, shortly swing the other way to "disturbed and uncomfortable". I must say that nothing I heard tonight suggests further Fed tightening is imminent. However, that point in itself makes me disturbed and uncomfortable and at some point the market will oscillate around to that view - perhaps next Thursday when I think there is a good chance that core CPI rises to 2.4% y/y.

Administrative Note: On Friday at 4pm ET, I will be on Bloomberg TV's "What'd You Miss?" with Joe Weisenthal, Alix Steel, and Scarlet Fu.

[1] In keeping with my usual tilt to keep focused on inflation and real values, it should be noted that the $64,000 question would today be the $523,277 question. The quiz show ended in November 1958 with the CPI price index at 29; it is now at 237.111.

[2] Interestingly, this last point directly echoes some of Keynes' points in the General Theory. I will revisit that point next week.

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"