“IN MANY WAYS this has been the most remarkably cheerful summer in recent financial history. The stock market speaks for itself. After the serious decline in May, prices of the leading securities have been marching steadily upward... This prosperity might be disquieting if it were accompanied by any of the symptoms of inflation.” …Outlook & Independent -- August 7, 1929

Steady As She Goes

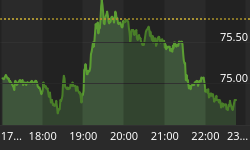

Except for Friday, it has been a very quiet summer in the gold market also. If it weren't for my self-proclaimed incredible patience and the encouraging pattern developing on the long-term chart, it would not be difficult to bore myself into bearishness. That said the tape bounced firmly on Friday, as gold prices found that trading range support was indeed there. In the final round of the session, gold closed up nearly $3 on the day, as the longs came in and swept the market clean. Moreover, this happened on a stronger dollar week. A lot of this activity may have to do with the typical summer rollover to December Gold. But even so, the bullish resolution is another good sign. All in all, the data implies that gold has seen more accumulation than distribution for at least the past year. That, by itself, will not guarantee a bull market, but it sure creates the incentive for one.

Meanwhile, energy prices remained stubbornly resilient, lease rates moved noticeably higher leading into Friday's move, and open interest had moved sharply higher all week long. It is interesting to note the historical relationships between open interest, volume, and price over the past few years.

On the following chart, notice how the bulk of the activity throughout the year has been to reduce the outstanding net short position. The pattern reveals sophisticated short coverers, as their closing strategy still appears to be to wait out the rallies. Since the June mini covering panic, however, they have become progressively more jumpy, living in fear of the kind of rally that almost crippled them almost one year ago this fall, and again in February. Now with bullish consensus readings hovering near 18%, and with time steadily nearing the one-year anniversary of the Washington Agreement, the market is begging for a squeeze. Steady as she goes.

Even with such bearishness on gold and bullishness on stocks, it appears that every few months or so, buyers come out of nowhere to sweep up the float. Then, it seems as if they backfill the covering shorts until they run into solid support, which prompts them into action again. At the moment, that appears to be at the low end of the $270 handle. If all that the bulls needed to know, to build up their confidence was that there is a solid floor underneath them, then the multiple tests of this level must be giving it to them by now. Only time will tell.

Inflation

The debate rages on. The topic is complicated because we have actually seen a little bit of both, deflation and inflation, in different segments of the domestic and world economy. What's more, there is much unlearning that needs to be done before we can understand how both phenomena interact within a closed economic system, let alone a global system of free floating exchange rates. The roots of our current generally accepted definitions for inflation and deflation, in North America, really come from our longer acquaintance with fixed exchange rate regimes. How often do we forget that?

Since the old economy days, however, economic principles of sound and stable money have evolved to the ideology that floating exchange rates work as an effective self-correcting mechanism, which can soften recessions, and consequently enhance long-term growth. On the contrary, however, practical experience with our particular system of floating exchange rates, so far suggests that they are more likely to postpone, to engender, and to accentuate economic imbalances rather than to correct them. Especially when combining with a lender of last resort model, which itself is fiat. Arguably, this kind of inflationary system is flexible enough to lengthen the long (primary) wave of the business cycle, but if so, it can also deepen its natural amplitude. Rags to riches, riches to rags…extremes like that, if you will.

The inevitable corrective forces to such an unstable monetary infrastructure are likely to manifest themselves in a loss of confidence, and thus purchasing power for the underlying currency that the excesses are laid upon. Ludwig von Mises, in describing the process of inflation, notes the following sequence of events leading up to a total breakdown:

“The course of a progressing inflation is this: At the beginning the inflow of additional money makes the prices of some commodities and services rise; other prices rise later. The price rise affects the various commodities and services, as has been shown, at different dates and to a different extent. ”

“This first stage of the inflationary process may last for many years. While it lasts, the prices of many goods and services are not yet adjusted to the altered money relation. There are still people in the country who have not yet become aware of the fact that they are confronted with a price revolution which will finally result in a considerable rise of all prices, although the extent of this rise will not be the same in the various commodities and services. These people still believe that prices one day will drop. Waiting for this day, they restrict their purchases and concomitantly increase their cash holdings. As long as such ideas are still held by public opinion, it is not yet too late for the government to abandon its inflationary policy.” This is where we are today.

“But then finally the masses wake up. They become suddenly aware of the fact that inflation is a deliberate policy and will go on endlessly. A breakdown occurs. The crack-up boom appears. Everybody is anxious to swap his money against "real" goods, no matter whether he needs them or not, no matter how much money he has to pay for them. Within a very short time, within a few weeks or even days, the things which were used as money are no longer used as media of exchange. They become scrap pater. Nobody wants to give away anything against them."

“It was this that happened with the Continental currency in America in 1781, with the French mandats territoriaux in 1796, and with the German Mark in 1923. It happened with the dollar in 1973. It will happen again whenever the same conditions appear. If a thing has to be used as a medium of exchange, public opinion must not believe that the quantity of this thing will increase beyond all bounds. Inflation is a policy that cannot last.”

The Bears Are Divided

Deflationists might claim that we have already had our inflation in stock prices, real estate prices, energy prices, in many developing countries such as Russia, and that the current inflation rates are understated anyway. Some bears in this camp await a credit crisis to suddenly deliver us into a nasty depression, while others contend that the over investment in technology will also produce an enduring deflation in the years ahead. This is a very logically correct expectation set, prior to the advent of the current monetary arrangement.

Actually, I also held that position myself at one point until I discovered that the strong dollar policy has been a large contributor to the illusive prosperity that was being created all around me. That was my first clue. It was then that I first began to question my own education about the way that a market economy really works…something that I am still questioning.

Inflationists will say that we have already seen deflation this decade in raw materials prices, technology, and energy prices. Even though this kind of deflation was to our benefit, they maintain that the monetary inflation that we have provoked, in order just to avoid real deflation, will ultimately result in a vicious stagflation reminiscent of the seventies before it turns into a depression. Inflationists are persuaded that our current power structure will ruin the currency before allowing the inevitable deflation to spoil their kingdom. The fact that there is nothing in the policy structure preventing them from doing so is all the evidence we need.

The question, therefore, is not whether the current economic imbalances will resolve themselves, but how. Will the sporadic micro (isolated) inflations broaden into an inflationary crisis, or will the burden of global debt and excess technological capacity bury demand for the foreseeable future?

Stagflation

I know you will hate to hear this, but the truth is a little bit of both. Whew, glad we cleared that up. OK, so now, since I "lean" towards the inflation camp, allow me to inject a little spinal fluid into my person, and challenge that we will likely first see a broad inflation before a broad deflation, at least here in North America.

Conventional economics describes stagflation as a supply shock. In order to explain the concept, teachers will show you a whole bunch of northwesterly pointing arrows emanating from that big aggregate supply curve. This way, it was easy to blame OPEC for manipulating supply; since we were taught that stagflation was caused by a shift in this curve, rather than poor monetary policies at home.

How many times have you heard the statement, "it's the dollar stupid?" Actually, that is exactly what it is. Perceived this way, one could deduce the difference between deflation and stagflation, to be the dollar, and the difference between inflation and stagflation, to be demand.

That is how we could have both, inflation and deflation. Conceivably that is why the term stagflation was invented in the first place: to explain the coexistence of both, falling demand and rising prices, which rare phenomenon most recently, and most visibly, occurred in the seventies. Do you know what else first occurred in the seventies, by accident? One of history's most courageous attempts at global free-floating exchange rate systems, linked to nothing but government fiat. It is this system, and the inconspicuous moral hazards that accompany the active government "management" of any system, which is at the root of most monetary crises today. That is why we will again have stagflation, though to me, it is just inflation. If Oxford defines inflation as an artificial rise in price, what could be more artificial than that which is induced by the consequences of currency abuse?

Deflation

When the stock market crash of 1929 first landed on US demand, it forced a razor-sharp contraction in the nation's money supply, and with one fell swoop collapsed its credit worthiness. Yet, the misplaced policies that came afterward were most likely responsible for the duration of the depression, which was characterized by relentlessly falling prices for everything, and which we today describe as deflation. New investment is discouraged, spending is completely put off, and saving becomes an appreciated habit. Once this arrives, monetary policy is rendered useless to get us out. It becomes like "pushing on a string." The Japanese will attest to that.

There were many differences between then and now of course, but for the purpose of this discourse there were a few relevant ones: the global exchange rate system was largely fixed, the dollar was still pegged to gold, and most importantly, the United States was a net creditor to the world.

It is my contention that only the net creditor nation can really have this kind of deflation, particularly under a free-floating exchange-rate system, hence Japan's recent experience. The primary reason being that it is in the debtor nation's interest to inflate its way out of debt. A spoiled debtor nation will never tolerate the deflationary burden of its debt.

The last time that North America had faced any sort of real deflation threat since then was in 1980, when there were few remaining alternatives left to finally correct the decade long currency collapse, and high real interest rates were forced upon the economy. This brought demand to a halt and all but killed employment. But then, Americans were still important, if not net, creditors.

Today, the United States is no longer a net creditor

Deflation, at least the way most economists perceive it, is an inescapable, if unintended, corrective force for excess malinvestment. Naturally policymakers attempt to avoid it, yet all they do is postpone and deepen the final day of reckoning. Floating a fiat system was an effective way to postpone the consequences of the abuse of the dollar under Bretton Woods. "Managing," or inflating, the fiat monetary system to produce asset inflation, turned out to be an effective way to postpone the consequences of that abuse of the dollar over the last decade. Arguably the best way to avoid deflation is to prevent the preceding economic excess that breeds malinvestment in the first place. The longer this process of misallocating national resources goes on, the more painful will be the inevitable correction. It is as simple as that.

Yet another important basis of support for my claim - that it is more likely for the creditor nation to endure the real deflation - is that if global demand collapses, the only flow of money will be to pay debts, to make large divestitures, and to repatriate badly needed profits. Unfortunately, the beneficiaries of these kinds of flows today, would not be the United States. Note the chart below, which shows that US investment income from overseas investments has been overtaken by our investment income obligations to foreigners roughly at about the time that Mr. Greenspan dubbed the destination, for the phenomenal capital inflows, an "Island of Prosperity."

There are mainly two reasons that the dollar has stayed strong over the past three years; foreigners still prefer US investment returns for one, and secondly, they gladly endow the US consumer, who apparently has a "propensity to import," with an inflated purchasing power. All of the other stuff that you hear about, such as budget surpluses (if they exist), productivity, diversified financial system, goldilocks economy, etc., are simply reasons for foreigners to consider maintaining their claims on US assets in good standing…whether to continue empowering the "virtuous cycle."

I don't know how many of you may feel about your current debt load, but the average household in America might find that if they do not continue to maintain this "propensity to import," that the owners of their dollars and debt may discover less reason to own them. Then, maybe Mr. Greenspan might find that this propensity to import capital was merely the result of a convenient economic position that had financially benefited from the collapse of other currencies, one by one, as equally in fact, as it was the result of a learned nation of good storytellers.

It is because many economists and investors correctly expect that a credit collapse in North America would eventually lead to deflation, that they might expect a rising dollar. Fortunately for our smart leaders, however, the Plaza Accord, signed by the Group of Seven in 1985, really allows for the United States to abuse the reserve currency by agreement, should they need the currency "to better reflect fundamentals," and to achieve the overriding goal of the Plaza Accord - economic growth. In other words, the US has the "right" to devalue the reserve currency in favor of growth should it so desire. Interestingly, it also has the mandate to do this should it become convenient to correct its external (trade) imbalances. Nowhere is the United States legally bound to a stable money policy, and now that the US is a net debtor, it is not in its interest either.

The Elasticity of Money?

Bob Hoye of Institutional Advisors writes this in his third quarter report on Gold: “Through most of our review, gold and money were synonymous and declined during each bubble. Gold, in declining through ours, has been acting remarkably like money...The dramatic drop in investment demand for gold during a bubble and then increase in the post-bubble era makes the determination of price targets, or more importantly trend changes through fundamental analysis particularly elusive. As mentioned above, the eventual positive trend changes in gold's investment demand is directly related to exhaustion of financial speculation, which is being monitored by our Boom Indicators. At the climax of previous bubbles, speculators aggressively employed leverage against soaring financial markets. In effect, the position was long irresistible assets and "short" scorned money. When the senior currency was convertible, speculators were automatically short gold as well. In the post-bubble liquidity crisis, the panic to pay down debt can be described as short covering of money.”

Well, close but the senior currency does not really have to be convertible for speculators to throw cash and gold into the same short equation. But after reading this, one would get a sense that the exchange "value" of the dollar might appreciate then. In fact, however, if the issuers of the reserve currency face financial collapse, then who will want the currency except for the debtors? They might print ever more currency, so that they can pay their debts, but at what "exchange" terms will the creditors accept such an unsound currency? Increasingly, the situation looks a lot more like Ludwig von Mises described the process of inflation in human action.

I believe that, as always, policy makers will act to avoid the deflation that they perceive on the horizon. In the twenties, US policymakers may have been much more concerned with inflation than deflation, if only because of the recent visible experience in Germany with hyperinflation in 1923, and because their experience with the mild deflations up to that point perhaps made the prospect of another one more tolerable than the consequences of debasing a currency.

In stark contrast, if that is the case, then today we seem to be constantly running away from deflationary drafts. Taking our cue from falling commodity prices priced in overvalued paper, and collapsing global economies, increasingly we adopt inflationary policies, and we can always justify them. Look at the CPI not asset prices…or…look at core CPI and exclude the influence of oil prices. I say we, because the possible prospect of hard times is well promoted among the voting middle class of America, who will likely cast their votes in favor of the candidate with more inflationary promises, not less, this year.

As an example of the other kinds of reactions to a growing concern with financial retribution, consider that the G7 recently set up a body (the financial stability forum) to promote financial stability in the system. The IMF has been running around checking everyone's arrangements for his or her supervision of the banking sector. The BIS has been issuing studies that attempt to quantify the level of systemic risk in the financial system, and the effect of imposing new capital adequacy standards to fit the changing circumstances. The US administration has been making trade deals (read concessions) at an accelerating rate with the Chinese, likely because their financial clout can now pose a national security issue…well, OK, maybe because the Chinese probably helped out with their campaign a little. Twenty years ago, that would have been another Watergate. Normally, these bureaucratic moves are deflationary, as today they would squeeze this already bursting bubble. The unexpected collapse would force the lender of last resort, the Fed, into action, but all of a sudden, there is a conflict. The lender of last resort is the largest debtor.

Is there a plan?

Obviously, there exists some kind of a plan to deal with this contingent - when everybody heads for the exit at the same time. I wonder what it is? Whatever it is, it is likely to be too little too late. Besides, a plan cannot work on this scale unless the planners have all of the correct information. To those who still think our planners do, I say, then how did we get into this mess in the first place? Preventing the problem would have been more feasible. Dealing with the problem of an enormous asset/credit bubble after it has developed, will only politicize the economic process to the favor of the owners of all of this paper wealth. Or, is that already happening?

I was recently browsing the BIS Review for something interesting and came across a recent speech by Mr. O'Connell, the Governor of the Irish Central Bank. Since the Irish economy has been so hot, I thought it might be worthwhile to read it.

“There is now an awareness and an acceptance, at senior management and board levels, of the need for greater emphasis on the proper conduct of affairs. ” 19 July 2001

He was speaking about the imposition of a better supervision of Euro area banking and financial activities. This is analogous to announcing that you have found the bomb after it has already been set to go off. In light of the previous outcomes of similar, though somewhat smaller, monetary imbalances, let us hope that they at least know what kind of bomb it is. Our policymaker's record of judgment or, more appropriately, moral hazard is not good. When the dollar was ultimately allowed to float in 1973, for example, some of the more influential economists in Mr. Milton Friedman's camp predicted it would appreciate. Since that blunder, we have comically built this system upon one bad call after another.

Finally, twenty years later when faced with enormous cumulative imbalances, collapsing currencies (and economies) everywhere around us, and an unprecedented level of malinvestment, these bozos decide that it is time to build a better supervisory framework. Good luck. Provided that we somehow miraculously avoid an external shock to the system, such as an OIL CRISIS or something, more and more legislation will have to be invented just to prevent the inevitable economic consequences of an unstable financial system, before we finally realize that it just has to unwind on its own.

Perhaps by then we will realize that economists such as Eugene Birnbaum were right - i.e. floating exchange rate systems engender attempts to stabilize the realm through over regulation, when all that is needed for less regulation and more stability, is to stabilize the "coin" of the realm. Then maybe, we can do it right. Ah, but the politics of such a correct policy move are mind boggling, aren't they?

The Deflation Will Be in Japan

Last Tuesday, Bank of Japan Governor Masaru Hayami foreshadowed his inevitable decision to abandon the 18 month old zero interest rate policy on Friday, by raising the key overnight rate a ¼ point:

“Hayami said today his banking counterparts in Asia have asked him not to guide yen's value lower, adding that he doesn't see ``any need to weaken the yen further.'' He also repeated the BOJ should as soon as possible end its 18-month policy of keeping the overnight interbank rate near zero percent. ” Bloomberg...Aug 8 2000.

Increasingly, Japanese economic interests appear to contradict ours. Yet, that could not be further from the truth. It makes too much sense that it is to the mutual benefit of both Japan and the US to strengthen their bilateral relations. But there are too many reasons to discuss here. Who are these counterparts then? This long discounted direction in interest rate policy might suggest a common interest with China, in that this part of the world has been growing weary of dollar dominance anyway. Nonsense. In any case, as US financial markets grow weaker, the prospect of a Yen that could become a currency safehaven grows stronger. Note the resilience of the Yen in light of the not insignificant Tokyo stock market decline.

Unfortunately for Wall Street, whose usual sources of credit must be conspicuously absent, they may find it convenient to tap the Japanese debt markets where the demand for Samurai Bonds (foreign securities, mostly debt, denominated in Yen) is on the rise. There they can borrow at one-third the cost of accessing funds in the US markets. JP Morgan, Citicorp, Goldman, and a slew of developing country governments have either already done that this year, or are on the waiting list. Let this be a warning to the evil bankers: do not attempt to put on a Samurai carry-trade. It will not work. Possibly the Bank of Japan's move on Friday was also a message, that it is not afraid to look out for number one. Under the new policy, he has more control over the growth in the monetary base.

The foreign capital that has recently flowed into Japan, on the whole, has not panicked. Perhaps foreigners understand that although the National Debt has compounded, the Bank of Japan's gigantic foreign exchange reserves, vast private savings, and the country's cumulative Balance of Payments surplus, will work like a magnet for foreign capital in the midst of global economic turmoil.

Just four weeks ago, Mr. Masaru Hayami, the bank's governor, gave a speech entitled, Financial System Stability and Future Agenda - need to strengthen the capital base - in Tokyo, 14 July 2000. Although Mr. Hayami breathes a deep sigh of relief about the prospect that overall financial system stability appears to have been restored, he submits that Japanese banks' tier 1 capital base is still inadequate, relative to the US standard2. As a cure for this state of affairs, he recommends that Japanese banks move to redeem their high cost debt, and add to their internal reserves by turning a profit.

And how might I ask that they do that when the BOJ has started raising the cost on short-term capital to them?

That's probably up in the air, but I suspect that there will be plenty of banking opportunities in that part of the world over the next decade. Reading his speech, I discovered that there seems to be a growing market for failed Japanese banks; foreign investors and domestic non-financial corporations have been buying them up and establishing Internet banks, as well as other new innovative banking programs. The management environment in Japanese banking circles has evidently already changed, to one of a more intensely competitive race for market share in the investment banking business, consumer banking operations, and customer specific (targeted) businesses. Mr. Hayami's vision for how he foresees Japanese banks turning a profit:

By embracing the same virtuous circle that US banks evolved from in the early 1990's. His message to bankers is to stop acting like bankers, and start acting like businessmen.

This banking epiphany in Japan is not isolated. There seems to be a trail of epiphanies wherever the influential investment-banking arm of Goldman Sachs seems to appear. Consider for example, a recent speech by Mr. Herve Hannoun, the First Deputy Governor of the Banque de France. It was titled, "The Banque de France's View on Gold and Comments on the Euro," at a dinner organized by Goldman Sachs on the occasion of the Financial Times Gold Conference held on 26 June 2000.

Banque de France Compromises its Gold Views

In the speech, Mr. Hannoun emphasizes the Bank's official line; that Gold is an important reserve asset, and that the Bank opposes gold “selling.” However, he appeared to submit to the argument that favors the managing (leasing) of gold reserves in exchange for a reasonable rate of return.

With respect to holding its gold, the Banque de France's view is that "it is an asset of last resort par excellence."

As a rationale for owning gold today, the bank points out that:

1. “The absence of any credit risk is an intrinsic quality of gold: gold offers full security as long as it is properly stowed in central banks' vaults”

2. It has demonstrated its value as an asset with high relative liquidity in times of stress

3. It is a worthwhile hedge against the dollar's current position as the world's “First-Ranking Reserve Currency,” or in other words, a hedge against a decline in the Dollar.

On the subject of gold lending, Hannoun stresses that “Central banks must be aware that their (foreign gold) deposits may favor the financing of speculative gold sales.” At first glance, it sounds like he is presenting an objection to a GS sales pitch, as he makes it clear that he knows that these deposits encourage speculative short selling. However, Mr. Hannoun compromises the bank's number one (above) position on gold, by not mentioning the possibility that the majority of global gold loans that have already been made, may have been made to the detriment of the so called "intrinsic quality of the gold" - in so far as the loan has introduced a large degree of credit risk to the owners of the underlying reserve asset.

In articulating the Bank de France's policy on gold lending, Hannoun proudly suggests that his Bank's view “is now widely shared by the central banking community.” I am assuming he means at least those that signed the Washington Agreement in the fall of 1999: “Consequently, our policy regarding gold lending could be expressed as follows: a responsible holder must have a responsible approach to management. This means that the Banque de France has to and does pay due attention to the trade off between its own interests (i.e. enhancing the return on its assets) and the impact on the market.”

Obviously then, the Banque de France appreciates that the lending of too much gold will depreciate the asset, which defeats the purpose. The bank has also come to believe that gold should provide a return like every other asset.

Unfortunately, the treatment of gold as any other asset contradicts its role as a reserve asset, and making the directive of a central bank to fulfill a profitable account of its assets, necessarily compromises its role as a lender of “last” resort. The treatment of gold as any other asset is counterproductive to its true intrinsic worth as a reserve asset.

Nevertheless, it is perceived that the Bank de France and the Bundesbank were the driving forces behind the Washington Agreement, and it is therefore likely that any future gold selling/lending, managed by the institutions bound under that agreement, will be managed with respect for the effect on gold prices. Also, for the record, as a result of only now officially submitting to the arguments in favor of managing (leasing) the central bank's gold reserves, Hannoun is denying that the Banque de France has been an active lender of gold thus far. Thus, at some future time, will the official disclosure that gold reserves be managed like any other currency or asset not undermine organizations such as GATA, whose prime directive is to prove manipulation? This way, they (the manipulators) can say, “what manipulation? It is just management. C'mon, we've been doing it for years anyway.” What a coup.

Of course, that will not save them from the economic (and social) consequences that will result from the fact that they had indeed “managed” these gold reserves for years, without regard for the true intrinsic quality of Gold and without respect for the inevitable market forces that will correct such increasingly conspicuous mismanagement.

Which brings me to the next point

The fact that the gold market is already largely managed, to me is so second nature that I don't understand other people's unawareness about the subject. If you understand the tremendous role that governments play in daily foreign exchange markets, you must understand that market to be managed presumably to our benefit. We already know that interest rate policy is manipulated to our benefit, again presumably. Gold is an important monetary asset. At least as important as interest rates and currencies are to confidence and perception. Please, tell me why the market would not be managed. In fact, public denials to acknowledge the fact are simply admission that they are not managed to our benefit. So, the question is not whether, but to what end they are being managed today?

Why would anyone care about such a small industry?

One of the more difficult arguments against gold is the relatively puny size of the industry relative to say, the market capitalization of General Electric, but let us put that aside for one moment to discuss “how” this gold is valued, or priced.

In paper!

In our economic system, as long as paper inflation delivers prosperity, it will always be desired. But can it do so indefinitely? A hasty look through the popular news disseminators will argue yes. A historical perspective, however, will provide many examples of our problems with other "sophisticated" paper based monetary systems. They tend to cause either too much inflation or result in too much deflation. In other words they are unstable. If you can accept that, allow me to argue that they are ever more unstable today. This is not paranoia, at least not to any of my psychiatrist clients (just kidding).

I have been trying to argue that our ability to inflate this paper system to our favor is over extended, dangerously. I, and other much more astute observers, argue that there are visible signs of imbalance/instability, and that there are visible cracks erupting in the infrastructure of our global monetary system, which commands quite a confidence premium. I argue that these cracks will gain in momentum and manifest themselves in a deflation of this paper. Thus, if gold, oil, copper, computer chips, real estate, palladium, or whatever, is priced in paper, then value -- or is it price -- of such "commodity" shall inflate. It's really that simple.

Therefore, the value of the entire gold mining industry today is relative to our inflated paper system, where psychologically at least, price indeed equals value. Judging by the reasonably visible risk of systemic financial failure, I would say that the true value of gold as a monetary asset then, is under priced. Since the sources of the excess supply of gold are usually bankers who argue against gold's value as a monetary asset, then it is clear that they favor the prosperity enhancing paper dollar system.

But what if something goes wrong. Things might happen that they never thought would happen. Suddenly, they find themselves in a big mess and the only way to avoid the day of reckoning is to push this thing as far as it will go!

That is not today, it was four years ago. We are already here - as far as it will go.

What is going on with the dollar?

If the stock market has been discounting a soft landing this past month, why is the dollar up? Shouldn't a soft landing in the United States pressure the interest rate differential between the dollar/euro and the dollar/yen? Perhaps dollar buyers are expecting that the slowdown will engender a hold up in imports, and thus a correction in the trade deficit? Wait, it has already been demonstrated that capital flows, not trade, determine trends in currency markets today. So, why is capital flowing into the dollar? It could be related to some of the recent M&A activity, but you would think many of these companies already own dollars.

Deflationists argue that it is an early warning sign of the deflation to come, however, there is no sign of a scarcity of dollars in the driver's seat behind this rally. In fact, there are an abundance of dollars printed every day:

Again, Doug Noland best discerns the most likely reason for the appreciation in the dollar this summer3. “While broad money supply and bank credit growth were more tempered (M3 expanded $3 billion and bank credit $7 billion), we see that commercial paper outstanding increased $24 billion during the past week. During the last four weeks, total commercial paper has expanded $57 billion, or at an annualized rate of 39%. Year-to-date, total commercial paper has increased $161 billion (more than total M2 growth of about $130 billion!), or at a rate of 20%.”

The commercial paper that he is referring to includes credit card receivables and finance company debt that has been securitized, and is now offered, or sold, to foreign investors - effectively monetizing our consumer debt. Such highly rated debt, which offers above average return potential, is certainly attractive enough to keep the dollar buying cycle going long enough to kick into gear this virtuous cycle where that trend reliquifies US stock markets, which in turn drive the dollar higher, hopefully keeping inflation in check, and perhaps even juicing the bond market, which of course will drive rates lower, make money and credit cheaper, etc. Sorry guys, it cannot happen that way anymore. For one, it would cause further monetary problems abroad to surface (inflation and currency collapse - for the weaker economies). Secondly, there just isn't enough real money in the world to kick this cycle into gear again - as my evidence, just consider the quality of money that is being used to finance the attempt now - not to mention the inflection point that we seem to have passed, and which progressively more, will become reflected in the popular inflation figures.

What Are the Bulls Saying?

“Growth in personal consumption, which accounts for two-thirds of all spending in the U.S. economy, rose at a 3 percent annualized rate - a significant decrease from the 7.6 percent rate posted during the first quarter. This deceleration was helped along by six interest rate increases instituted by the Federal Reserve throughout the past year;” Joe Battipaglia, in providing evidence that we have got our economic slowdown, July 31 2000, CBS Market Watch.

First of all, only a religious bull would take this position on the first (unrevised) GDP report, knowing full well that other personal income and expenditure figures were yet to be included for June. And only a football player wouldn't have noticed the “seasonal” tendency for a slowdown in consumption during the second quarter. Undoubtedly, he is using the statistic to support the bullish “soft landing” tout. While there is absolutely nothing wrong with being optimistic about the future, there is everything wrong with convincing yourself to be so, especially if the data isn't conclusive. For, as it provides the support he apparently needs to make the bullish case, if the revision holds, it provides me with even greater fuel to firm up the bearish case.

Mr. Battipaglia goes on to paint a perfect picture of slowing consumption and accelerating investment spending. With all due respect for the man's bullish bias, what persuades him that the acceleration in investment spending so far, in order to expand productive capacity, is not a typical cycle high overestimation of future demand that will simply resolve in excess capacity, as usual? Perhaps the “remarkable” productivity numbers explain the virtuous circle? I think not4. In fact, a close look at what the average consumer has been doing to his balance sheet, ought to have at least stifled his conclusions, which largely reflect those of nearly every other bull that walks Wall Street today. Furthermore, he makes the fatal mistake of qualifying investment spending as the least inflationary segment of the economy. This flaw is based on a conviction that the investment will expand the nation's productive capacity and therefore contribute to productivity. It ignores the possibility that we have become dependent on capital inflows for this virtuous investment-spending cycle to actually work.

What are the bulls buying?

Certainly not retail stocks, if they are listening to Joe. This week they have been buying the good old-fashioned cyclical stocks, energy stocks, and financial stocks, having just spent most of the summer selling them in favor of another run in leading technology names, which appears further away by the day. Perhaps the NASDAQ is just too broad, and too spent, for them to move it any higher. So what's the plan then? The multiple on the Transports is attractive, but on the Industrials it is in the high twenties. Do investors suddenly believe that any company, regardless of size, can grow at 20 to 30 percent? Do not get sucked into this move, born of confusion. For a new bull market leg to sustain, the bond and the dollar will need to at least stay steady, which means that the dollar buying cycle needs to continue, at least to the tune of around $30 billion per month, net. Yet, perhaps it might become a little difficult to justify new dollar purchases if the growth and interest rate differential with the rest of the world begins to narrow.

Additionally, Japan finally ended its 18-month old moratorium on interest rates Friday, in a bold move that will likely pressure the dollar over the medium term. Britain is concerned about the potentially inflationary weakness in the pound, and the European Central Bank will continue on its more prudent path to not only monitor inflation rates, but also money supply growth.

As I suggested in my last report, 28 July 2000, the Greenspan Fed has been working hard to shut down all the corners that Wall Street has been exploiting. The last liquidity machine that seems to be working is the consumer and his willingness to effectively make a deal with the finance companies; “if you can lend it to me, I'll spend it.”

Sounds like a better deal for foreign exporters than it does for the foreign lender, but of course, that is why the stuff has been securitized and thrown into the money market.

1. The BIS Review

2. The BIS Review

3. The Credit Bubble Bulletin can be accessed at PrudentBear

4. For more on the great productivity debate, see A Nation of Story Tellers