Now that US equity indices have erased all of Monday's gains less than 24-hours after the US Treasury's takeover of Fannie Mae and Freddie, we can further better deduce the extent of negative sentiment prevailing in US and overseas markets. We illustrated on Monday how the number of "up" days in US equity indices following the various interventions from the Fed and the Treasury of the past 9 months has declined over time. The Fed-backed takeover of Bear Stearns in mid March produced a rally lasting 2 months. The Treasury's decision to extend credit to GSEs' in mid July produced a rally lasting 1 month. Monday's historical announcement of the implicit nationalization of Fannie and Freddie produced a rally lasting 24 hours. Tuesday's declines of 3.4% and 2.5% in the S&P500 and the Dow are more than just about Lehman Brothers' struggle to raise sufficient capital or the uncertain future with the GSEs and the US mortgage market. The 3.2% decline in US pending home sales in July following a 5.3% increase went unnoticed. The story remains that of persistently weak fundamentals and a deteriorating credit fabric, dogged by a pick up in forced hedge fund redemptions.

The FX implications remain led by rising risk aversion, highlighted by a rallying JPY and falling high yielders (GBP, AUD and NZD). We continue to focus on Sterling as the poster child of a high yielding currencies falling victim to unwinding of long-term carry trades. Yet, unlike AUD and NZD, the Bank of England has yet to cut interest rates in this second half of the year, thereby further limiting prospects for a recovery in GBP and UK.

USDJPY Eyes 105 Until FOMC

USDJPY is the single USD pair failing to ride the USS rally as the yen thrives on severe impairment of risk appetite, courtesy of US financials, credit market and eroding macro fundamentals. We expect further to extend into next week's FOMC meeting, which is likely to focus on the downside risks of the economy. Although the Fed is seen maintaining its tough language on inflation, we expect the statement to push the balance of risks closer to the downside, in which case may spur a relief rally in equities. The September 16 Fed decision will likely shut the door on all remaining rate hike expectations, allowing for probabilities of a Fed easing later in the year to grow. Our persistent forecasts for the Fed to resume easing later this year may well materialize in Q4. But USDJPY selling is likely to subside around Fed decision. 105.80 and 105 are in focus.

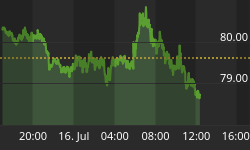

Cable's Path to $1.72

Despite this week's temporary rebound in cable, the bearish outlook for the currency remains intact due to policy paralysis in the UK Treasury and the Bank of England. UK authorities have been the antithesis of their US counterparts as far as policy measures and proposals for shorting up support to the economy and the markets. The head-&-shoulder formation in the 4-hour chart below suggests resistance at $1.77, followed by 1.7790. Downside guided towards $1.7550 and $1.7480.

Thus, at times of emerging selloffs in equities, an alternative play to selling USDJPY and other yen crosses remains shorting GBPUSD and NZDUSD. The latter is an especially atrractive choice ahead of Thursday's (Wednesday 5 pm EST ) widely anticipated 25-bp rate cut by the Reserve Bank of New Zealand to 7.75%.